Click here to read important disclaimer & disclosures Click here to see more about Skyharbour Resources Ltd.

TSX-V: SYH | OTC: SYHBF

Advancing Multiple High-Grade Uranium Exploration Projects in the 2025 Uranium Bull Market

Click Here to Read Sponsor Disclosure

The new uranium bull market is now underway with U3O8 prices recently surging to decade-plus highs…

…and best of all, it’s still early innings with more potential upside and uranium equities offering additional value relative to the commodity price as we head into 2025.

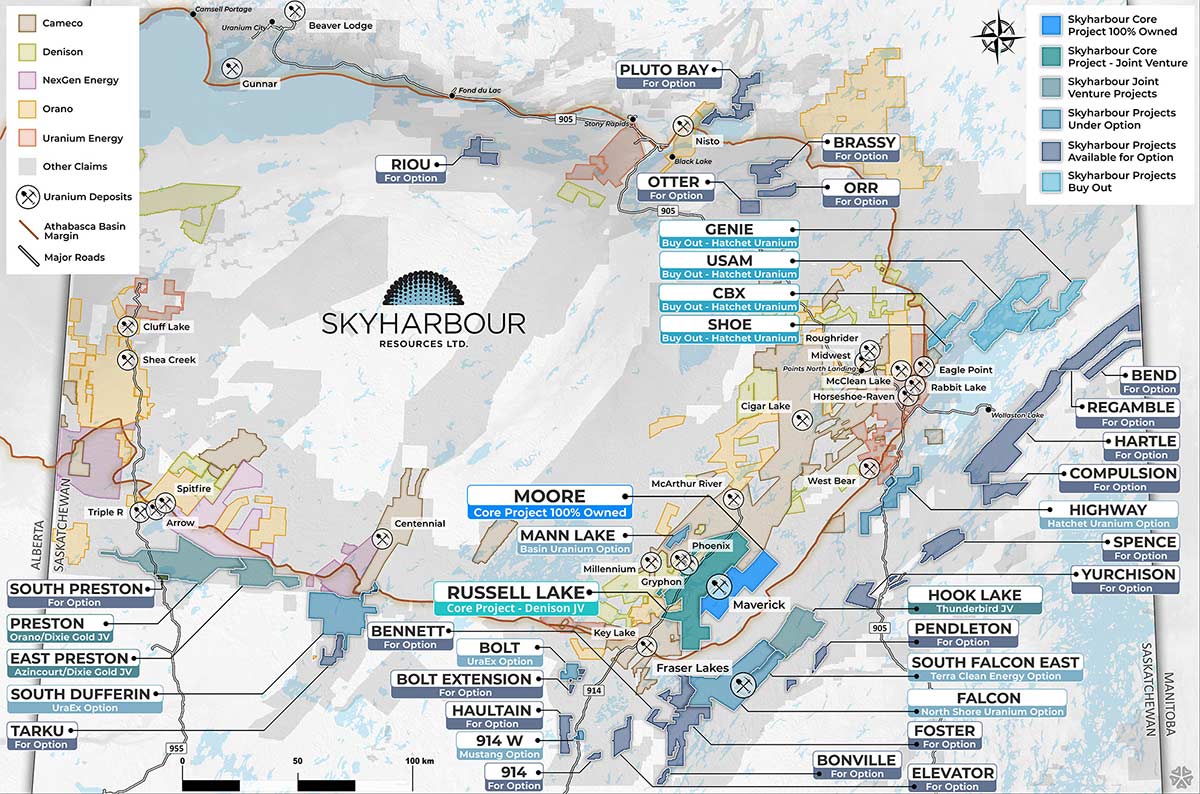

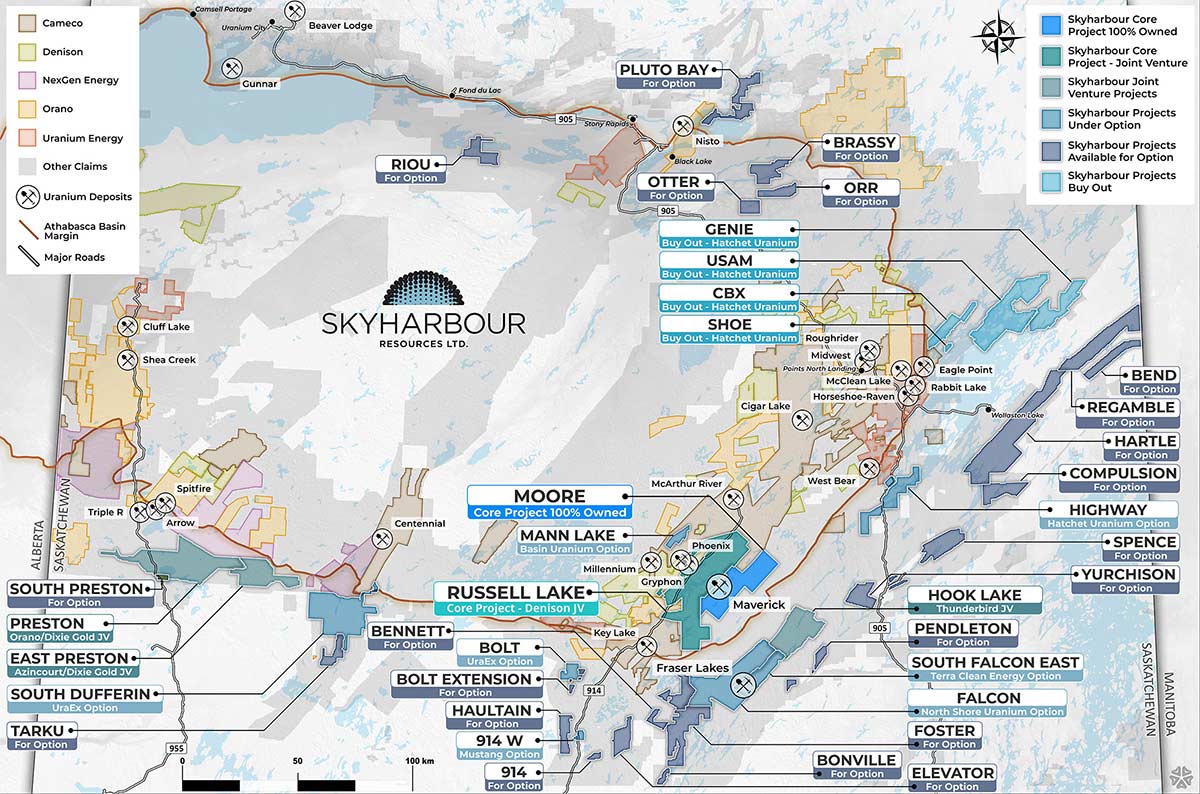

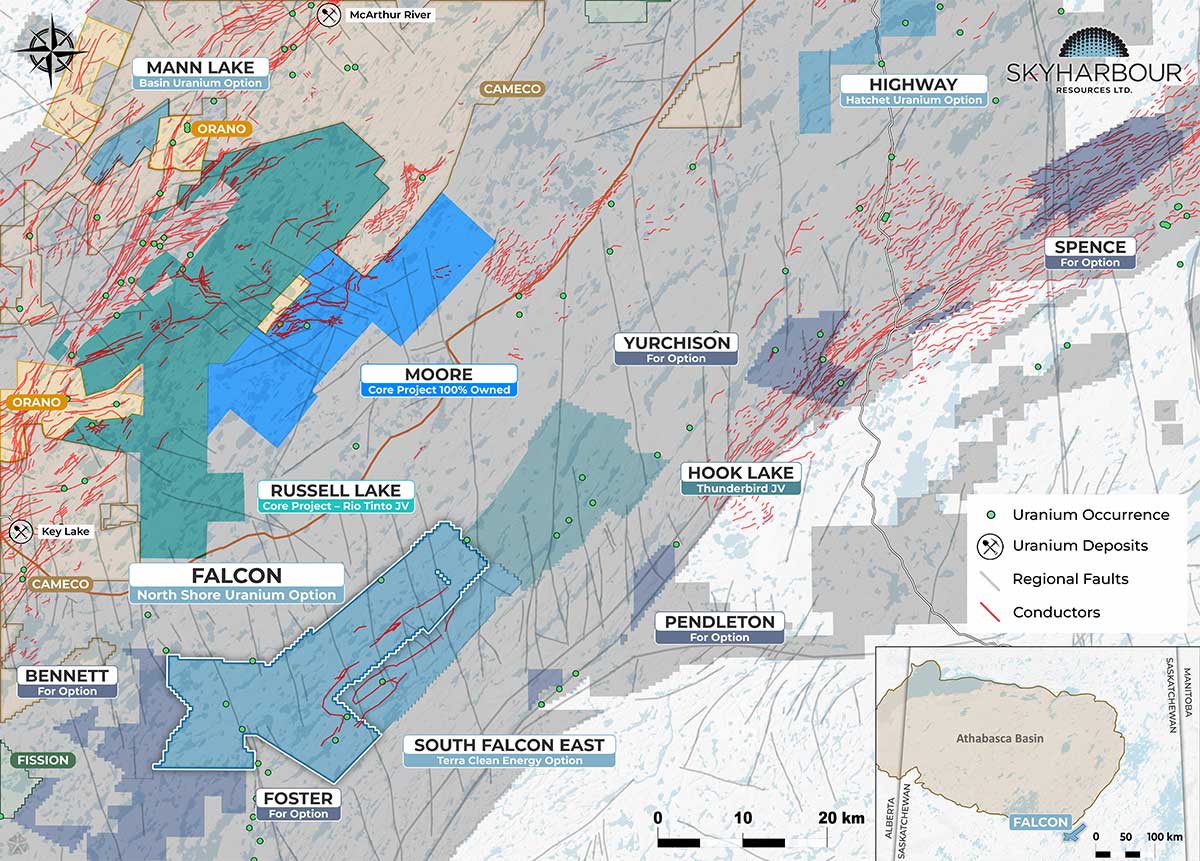

The small-cap uranium company featured in this report — Skyharbour Resources Ltd. — has acquired an extensive portfolio of uranium exploration projects in Canada’s prolific Athabasca Basin and is well-positioned to benefit from improving uranium market fundamentals with 37 projects covering over 616,000 hectares (over 1.5 million acres) of land.

The co-flagship projects are the 100%-owned Moore Lake Uranium Project located 15 km east of Denison’s Wheeler River uranium project and 39 km south of Cameco’s McArthur River uranium mine and the adjacent Russell Lake Project, in which Skyharbour and Denison have entered into a major strategic agreement that restructures the Russell Lake property into four distinct advanced stage exploration projects.

Additionally, SYH has a total of 14 partner-funded uranium projects being actively advanced by a total of 10 partner companies in the Athabasca Basin region as part of their prospect generator strategy.

Uranium Bull Market Accelerating into 2025

There’s a major positive shift happening in the global nuclear energy market.

The world is quickly realizing that lofty climate goals will be impossible to meet without clean-burning, carbon-emissions-free nuclear energy being an integral part of the clean-energy mix.

That fact is adding escalating pressure on an already constrained global uranium supply.

With uranium, what we arrive at is a market that’s consuming close to 200 million pounds of yellowcake annually — yet producing only around 140-150 million pounds.

That equates to a 50-60-million-pound structural deficit this year… which, when compounded over the next six years to the end of the current decade, balloons to a jaw-dropping ~360 million pounds.

That’s a staggeringly large deficit… and it underpins the escalating need for new domestic and friendly uranium sources reaching the supply chain.

And it’s really only the start.

On the demand side, we have Japan looking to restart a further 16 of its reactors. The island nation is also seeking ways to safely extend the plant-life of its existing reactor fleet from 40 to 60 years.

China just approved the construction of six new nuclear reactors across three provinces with plans to build 150 new reactors over the next 15 years as part of their newly-enhanced decarbonization mandate.

South Korea and India have also joined the fray and are now fully onboard with a cleaner energy future that will require vast amounts of uranium, or U3O8.

In Europe, France’s economy minister has doubled down on the need for a top-to-bottom overhaul of the electricity market saying, “there is no energetic transition without nuclear energy.” The nation has announced plans to construct a new generation of nuclear reactors for the first time in decades.

Even Finland’s Green Party — following decades of staunch opposition — voted overwhelmingly last year to categorize nuclear power as a form of sustainable energy. At present, one-third of Finland’s electricity is derived from nuclear power. And in 2023, the country’s OL3 reactor, Europe’s largest, finally went online.

Other European nations are quickly falling in line with Finland’s pro-nuclear stance. Britain and Sweden are each planning new nuclear reactor projects with Belgium and Spain also cementing their support for the clean energy source.

At the COP29 conference in Baku, Azerbaijan in November 2024, 31 nations including some of the largest economies in the world, signed a declaration to triple nuclear capacity by 2050.

Here in the United States, TerraPower is currently constructing a US$4B nuclear power plant in Wyoming that’ll use an all-new blend of enriched uranium.

Once completed, it is expected to generate efficient, low-cost, clean energy while utilizing enhanced safety standards that greatly reduce the risk of accident — even on par with wind power plants.

NuScale recently became the first company to be granted approval by the US government on small modular reactor (SMR) designs with the US Nuclear Regulatory Commission giving it the green light. Privately-owned Standard Power followed up that news with an announced partnership with NuScale on the construction of two SMRs to power its data center company customers.

The emerging industry of artificial intelligence (AI) and its required data centers are another new source of potential demand. Recent announcements from major tech giants highlight a growing commitment to nuclear energy as a long-term, clean power solution. Microsoft is investing $1.6 billion to help revive the Three Mile Island site, paired with a 20-year power purchase agreement (PPA), signaling its intent to secure stable, zero-carbon energy for decades.

Oracle has taken concrete steps toward advanced nuclear adoption, having secured building permits for Small Modular Reactors (SMRs)—a key milestone in next-gen nuclear deployment. Meanwhile, Google has partnered with Kairos Power to advance the deployment of 500 megawatts of advanced nuclear capacity, demonstrating its support for innovation in nuclear technology.

Amazon continues to support the nuclear sector through multiple development agreements, and Meta recently signed a 20-year agreement with Constellation Energy to source 1,121 megawatts of nuclear power from the Clinton Power Station in Illinois—enough to support a massive portion of its data center demand with clean baseload power.

Put plainly, increased uranium demand is coming from all angles. And that includes a new contracting cycle that’s just now getting underway with major utilities entering the market to secure their next long-term U3O8 contracts.

The combination of dwindling secondary supplies, supply cuts from the highest-margin producers, and utilities coming back into the market will create what many experts agree could be the greatest uranium bull market anyone has ever seen.

The Inflation Reduction Act of 2022 also provides funding for US nuclear power projects, including a tax credit for electricity produced at qualified nuclear power facilities.

Next, you have to look at the precariousness of the global uranium supply to really get the full picture.

The West has relied heavily on uranium and nuclear fuel imports from countries like Kazakhstan, Russia, and Niger, which introduces significant geopolitical risk. Western governments and utilities are now recognizing this vulnerability and are starting to prioritize supply from western jurisdictions.

To secure future uranium supply independent of geopolitical risks, the West must ramp up production within uranium producing jurisdictions like the Athabasca Basin, streamline permitting, and invest in conversion/enrichment capacity as well as nuclear fuel cycle infrastructure. Recent executive orders from President Trump aim to cut red tape around uranium mining and new nuclear builds by invoking the Defense Production Act, fast-tracking reactor approvals within 18 months, and opening up federal lands for advanced nuclear deployment. These actions also encourage public-private partnerships and international cooperation to reduce reliance on unreliable suppliers and position the U.S. as a global leader in nuclear energy. The administration has stated they would like to see a quadrupling of US nuclear energy by 2050 including 10 new large reactor builds underway by 2030.

What’s more, the MET (Mineral Extraction Tax) for uranium will further increase starting in 2026 when a two-tier system goes online, which will take into account production output and spot uranium prices. Producers with large uranium assets in Kazakhstan could potentially end up paying an MET as high as 20%.

BMO Capital says the new tax system will limit future supply growth, which, of course, means an even tighter supply of uranium at a time of escalating global demand.

Uranium supply is also being squeezed by aggressive spot market buying, led by the Sprott Physical Uranium Trust (SPUT), which has acquired nearly 50 million lbs in recent years and recently raised $200 million to continue its purchasing spree. Other players like Yellowcake PLC and Uranium Energy Corp have followed suit, further tightening available supply.

As a result, uranium inventories are continuing to shrink, most notably from 3.5 years to around 2 years of supply right here in the United States, well below the historical average.

We also talked about restarts and lifespan extensions on reactors… and it’s not just Japan that’s going down that road.

In California, the Diablo Canyon nuclear plant, originally scheduled to begin shutting down in 2025, is now expected to remain operational through at least 2030 following state and federal support, including a $1.1 billion DOE grant to extend its lifespan.

Similar life-extension efforts are underway in Belgium, which has postponed the closure of two reactors by 10 years (to 2035), and in Finland and Slovakia, where operating licenses have been extended and upgrades are being made to keep existing reactors running longer to meet energy security and climate goals.

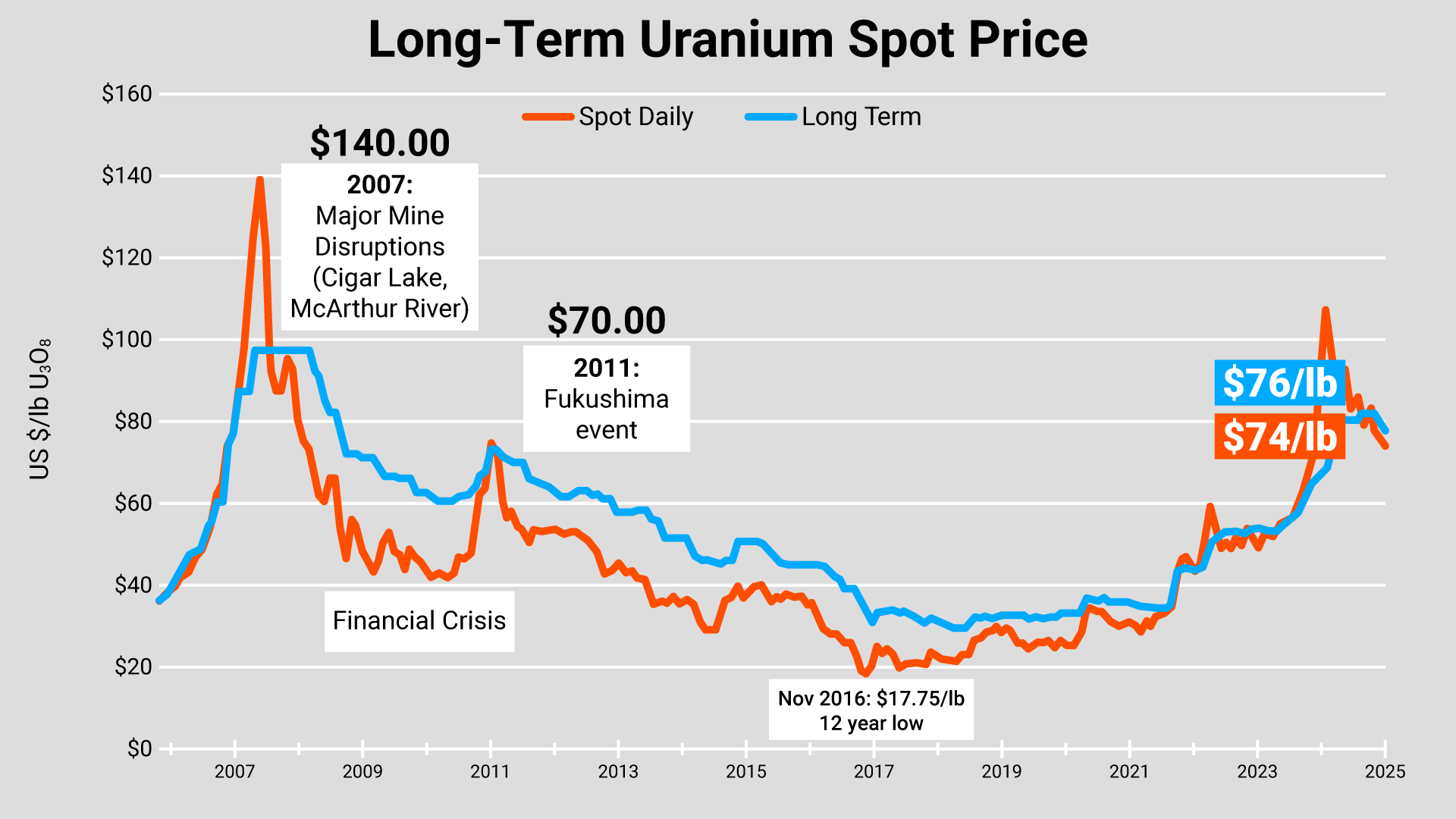

All of that is to say that any further disruptions to the global uranium supply chain could lead to a run on uranium spot prices — possibly like what we saw back in 2006-07 when uranium soared to US$140 per pound upon the flooding of Cameco’s Cigar Lake Mine.

That upsurge caused the share prices of most uranium mining companies to breakout… resulting in substantial gains for well-timed investors.

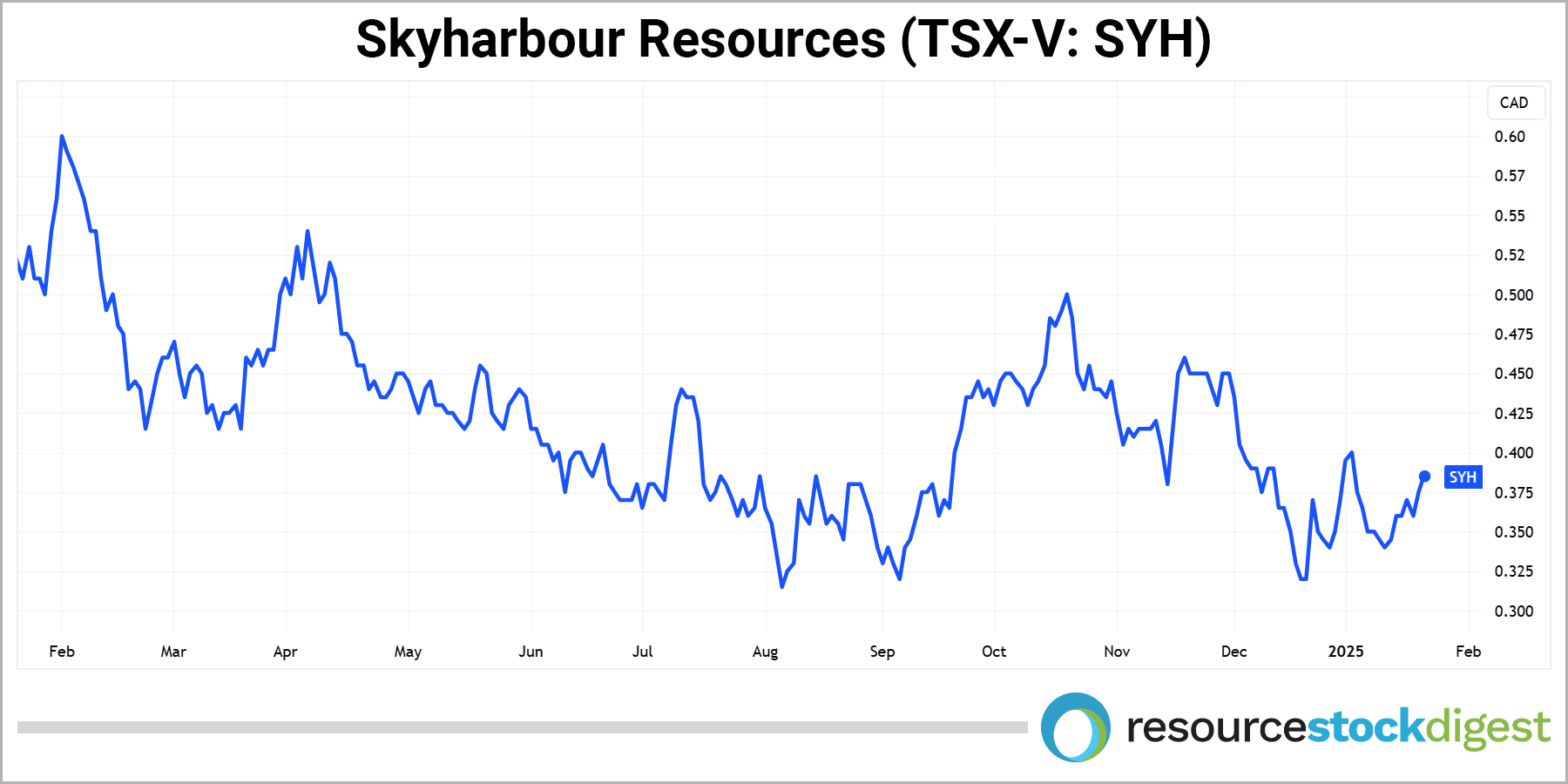

We’re currently north of US$70 per pound U3O8. A few short years ago, uranium prices were languishing at the US$30/lb level. So the uptrend is clearly underway as you can tell by the long-term uranium price chart below.

With geopolitical upheaval at an all-time high in key uranium producing countries, including Russia (which will have its uranium exports sanctioned by the United States in the coming years), the writing’s clearly on the wall for higher uranium prices going forward.

It also underpins the need for increased uranium production from safe jurisdictions such as the Athabasca Basin, located in Northern Saskatchewan, Canada, where Skyharbour is operating.

It’s still early innings in the current uranium uptrend, which means now is an opportune time for resource investors to consider positioning for what could be a material move higher in 2025 and beyond.

Enter Skyharbour Resources Ltd. (TSX-V: SYH)(OTC: SYHBF).

Skyharbour Resources: A Brilliant Growth Model

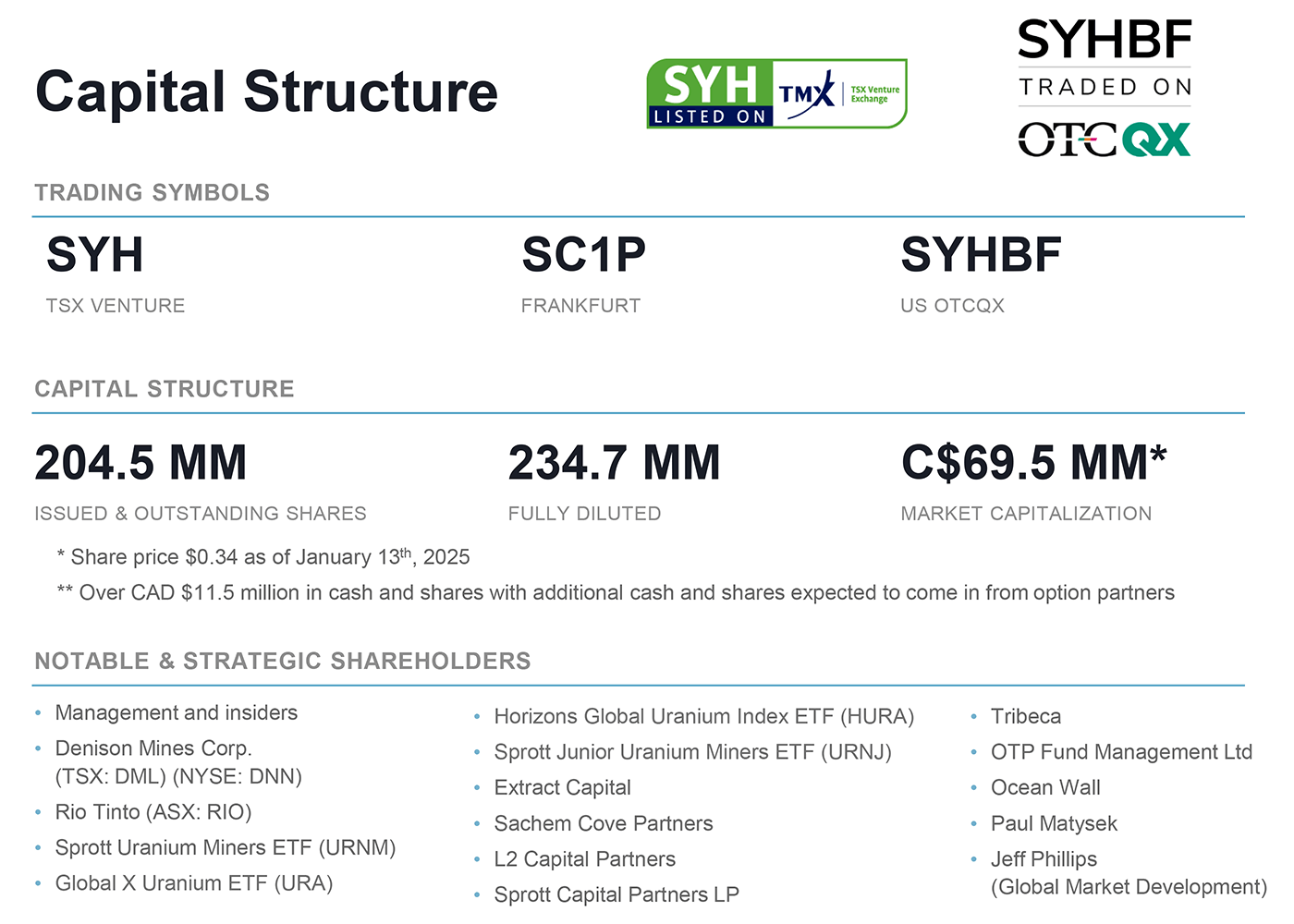

Skyharbour Resources Ltd. (TSX-V: SYH | OTC: SYHBF) is a high-grade uranium exploration and early stage development company with 37 projects, covering over 616,000 hectares (over 1.5 million acres) of land in the prolific Athabasca Basin of Saskatchewan, Canada.

These projects range from more advanced-stage exploration assets that either host small uranium resources and/or have high-grade U3O8 mineralization in previous drilling, to earlier-stage exploration properties ideal for optioning out to partner companies who then fund the exploration.

The Athabasca Basin is truly where the big boys come to play!

Industry leaders like Cameco have their largest uranium mines in the Athabasca. These are some of the biggest and richest uranium mines in the world… including behemoths like McArthur River and Cigar Lake.

Saskatchewan is consistently ranked as one of the best mining jurisdictions in the world, per the Fraser Institute — a benefit that simply cannot be overstated in today’s world where the nationalization or over-taxation of mining assets from foreign operators is commonplace.

With its own core projects plus several additional prospective properties being advanced by partners in the Athabasca Basin region, Skyharbour Resources Ltd. — currently trading around C$0.35 per share — represents an intriguing speculation in the North American uranium exploration space.

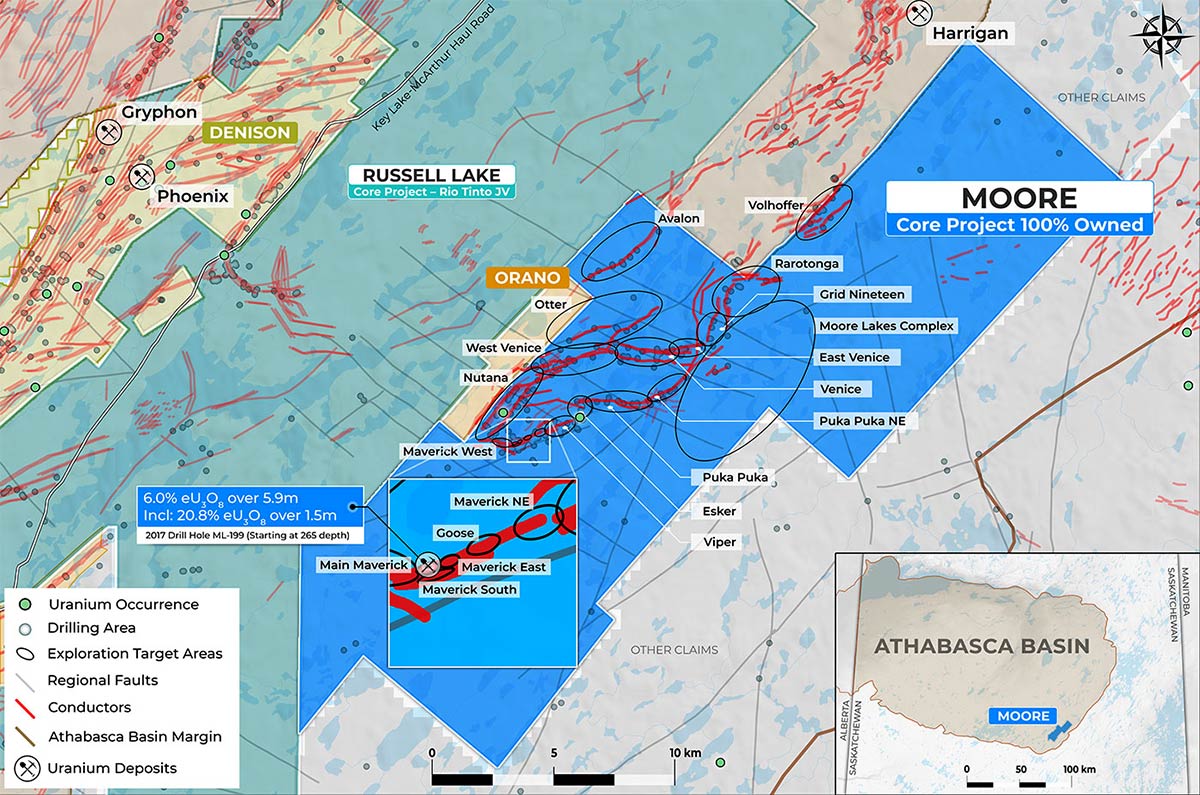

Co-Flagship Property: Moore Uranium Project

Skyharbour owns 100% of the 137 sq mi Moore Uranium Project located 9 miles east of Denison’s Wheeler River uranium project and 24 miles south of Cameco’s McArthur River uranium mine — all situated in Canada’s famed Athabasca Basin.

The Athabasca Basin hosts the world's richest uranium deposits and mines, producing approx. 15-20% of world’s primary uranium supply.

In 2016, Skyharbour acquired the Moore property from Denison Mines, a large strategic shareholder of the company.

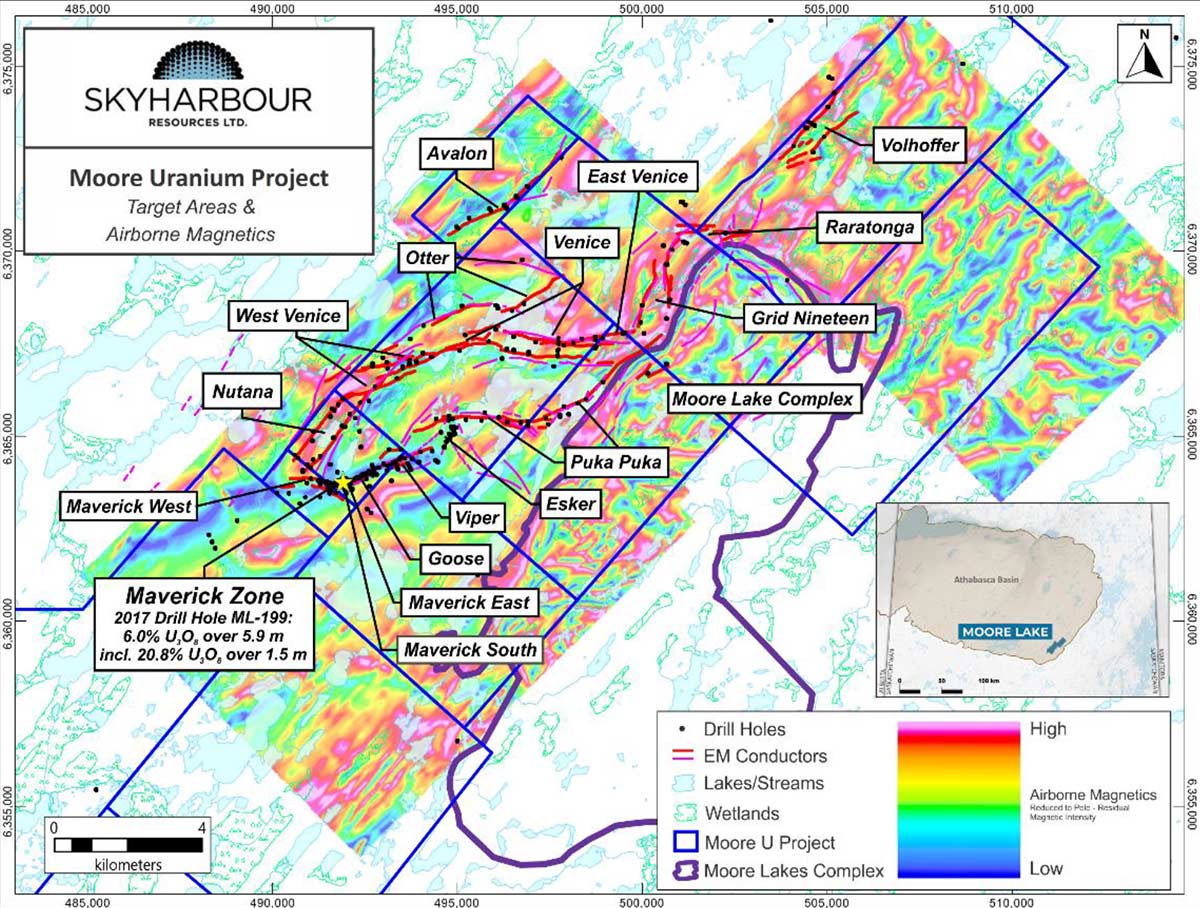

The project is an advanced-stage uranium exploration property with high-grade uranium mineralization at the Maverick Zone that has returned drill results of up to 6.0% U3O8 over 5.9 meters, including 20.8% U3O8 over 1.5 meters at a vertical depth of 265 meters.

In addition to the Maverick Zone, the project hosts other mineralized targets with strong discovery potential, which the Skyharbour team plans to test with future drill programs.

The 2024 winter drill program at Moore Lake totaled 2,864 metres and focused on infill and expansion drilling at the high-grade Main Maverick Zone, as well as testing regional targets such as Grid Nineteen. All holes drilled in the Main Maverick Zone intersected significant uranium mineralization, with highlights including hole ML24-08, which returned 5.0 metres of 4.61% U3O8 from a relatively shallow depth, including a higher-grade interval of 7.30% U3O8 over 3.0 metres.

Skyharbour CEO, Jordan Trimble — whom you’ll be hearing from momentarily in our exclusive interview — commented via press release:

“We continue to discover and delineate new zones of uranium mineralization at our high-grade Moore Project and have plans for future drilling and exploration at the property…”

Keep in mind that the main Maverick corridor is approximately 4.7 km long with just over half having been systematically drill tested to date, which means there’s plenty of expansion potential along strike and at depth.

The remaining assay results from the late 2024 diamond drilling program, which included 2,759 metres over nine holes, were recently released. Notable results include hole ML24-15, which intersected 6.4 metres of 1.50% U3O8, including 4.74% over 1.5 metres, extending the Maverick East Zone by over 40 metres to the northeast. The Company is fully funded for an additional 5,000-metre drill program at Moore in 2025, with a continued focus on the Main Maverick and Maverick East Zones.

Furthermore, Skyharbour plans to test regional targets at Moore that have been further refined with modern geophysics and new geological modelling. This drilling will take place in conjunction with the multi-phased drilling campaign this year at the adjacent Russell Lake Project.

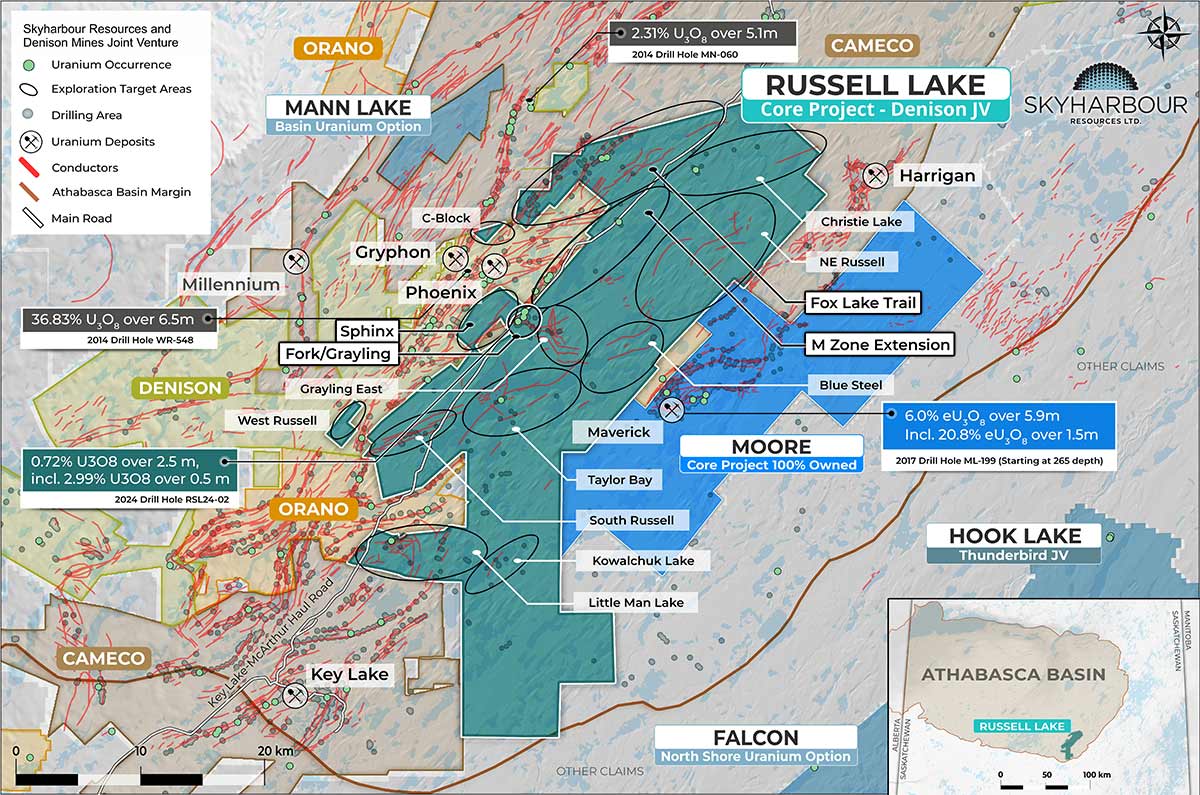

Joint Venture with Denison Mines to bring in Second Flagship Project: Russell Lake Uranium Project

In November 2025 Skyharbour acquired Rio Tinto Exploration Canada’s 42.3% interest in the Russell Lake Uranium Project for $10 million, consolidating 100% ownership of the large, advanced-stage asset. Skyharbour then executed a transformative Strategic Agreement with Denison Mines, dividing Russell Lake into four joint venture areas with total consideration of up to $61.5 million, including cash/share payments and exploration commitments. Skyharbour retains operatorship and an 80% interest at the core RL claims while Denison holds initial minority positions across the project areas.

The property is strategically located between Skyharbour’s other flagship, 100%-owned Moore uranium project and Denison Mines’ Wheeler River uranium project, and gives SYH a dominant land position in the southeastern corner of the basin (see below).

The Russell Lake project — which is considered a co-flagship for Skyharbour — is an advanced-stage exploration property comprising 27 claims and covering more than 73,000 hectares (283 sq mi).

The property is in close proximity to critical regional infrastructure including Cameco’s McArthur River Mine and Key Lake Mill as well as a road, powerline, and exploration camp situated on the property.

Skyharbour’s acquisition of Russell Lake creates a large, nearly contiguous block of highly prospective uranium claims totaling over 100,000 hectares (420 sq mi) when combined with the company’s adjacent Moore project.

Skyharbour entered into a major strategic partnership with Denison Mines, whereby Denison acquired Rio Tinto’s previous interest and joined Skyharbour as an active funding and operating partner at Russell Lake. The transaction, valued at up to C$61.5 million in combined consideration, establishes Denison as a key strategic shareholder and joint venture partner, with earn-in rights of 20% to 70% across the newly restructured Russell Lake property package. Skyharbour remains the operator across the majority of the project area, including the Russell Lake (RL) and Getty East claims, while Denison will lead exploration at Wheeler North and the Wheeler Inlier claims.

The partnership brings significant technical and financial strength to accelerate discovery efforts at Russell Lake, leveraging Denison’s expertise and proximity at Wheeler River. It also provides Skyharbour with substantial near-term funding and long-term exposure to one of the most prospective uranium corridors in the Athabasca Basin.

The Russell Lake property benefits from a significant amount of historical exploration and drilling — 95,000 meters across 230 drill holes — resulting in the identification of numerous prospective target areas along with several high-grade uranium showings and drill hole intercepts.

Skyharbour completed an inaugural three-phased, 9,600-meter drill program in 2023 across 19 holes at the Russell Lake Project.

The winter 2024 drilling at Russell was completed in two phases, totaling 5,152 metres across ten diamond drill holes. Phase One consisted of six holes totaling 3,094 metres and led to a significant discovery at the newly identified Fork Zone. Hole RSL24-02 intersected high-grade, sandstone-hosted uranium mineralization of up to 2.99% U3O8 over 0.5 metres within a broader interval of 0.721% U3O8 over 2.5 metres, just above the unconformity—representing the best drill results to date at the project. This new zone is located within the Fork Target, an area with minimal historical exploration due to limited geophysical coverage and interference from nearby powerlines. The Fork Target lies approximately 1 km southwest of the central Grayling Target and about 4 km southeast of Denison Mines’ Phoenix Deposit.

To support further exploration, the Company recently completed an Ambient Noise Tomography (ANT) survey across both the Fork and Grayling areas, refining drill targets ahead of the fall 2024 follow-up program, which included 4,500 metres of drilling (assays pending). Looking ahead to 2025, the Company is fully funded and has commenced the first phase of its largest-ever annual drill campaign. Plans include 10,000 to 11,000 metres of drilling at Russell, with a total of 16,000 its co-flagship Russell and Moore Lake projects.

Importantly, more than 35 km of largely untested prospective conductors in areas of low magnetic intensity exist property-wide. Plus, never a bad thing having an industry titan like Denison Mines as a large shareholder and JV partner at the co-flagship project.

Partner Funded Projects: Multiple Drill Programs Planned

In addition to the co-flagship Moore Uranium Project and the JV partnership with Rio Tinto Exploration Canada on the other co-flagship Russell Lake project, Skyharbour presently has agreements in place with 10 partner companies who are actively advancing a total of fourteen uranium exploration projects in Saskatchewan’s Athabasca Basin region:

- Preston: JV with Orano Canada Inc.

- Russell Lake: JV with NYSE listed Denison Mines

- East Preston: JV with TSX-V-listed Azincourt Energy

- Hook Lake: JV with ASX-listed Thunderbird Resources (previously Valor)

- Mann Lake: Option partnership with CSE-listed Nexus Uranium Corp. (previously Basin Uranium)

- Falcon: Option partnership with TSX-V-listed North Shore Uranium

- South Falcon East: Option partnership with TSX-V-listed Terra Clean Energy Corp. (previously Tisdale)

- South Dufferin & Bolt: Option partnership with private company UraEx Resources

- 914W: Option partnership with CSE-listed Mustang Energy Corp.

- Highway, Genie, Usam & CBX/Shoe: Option partnership with private company Hatchet Uranium Corp.

For speculators, having a suite of active partner projects means Skyharbour will be delivering news flow not just from its primary projects but also by way of its regional partner-funded projects as developments arise and as milestones are checked off.

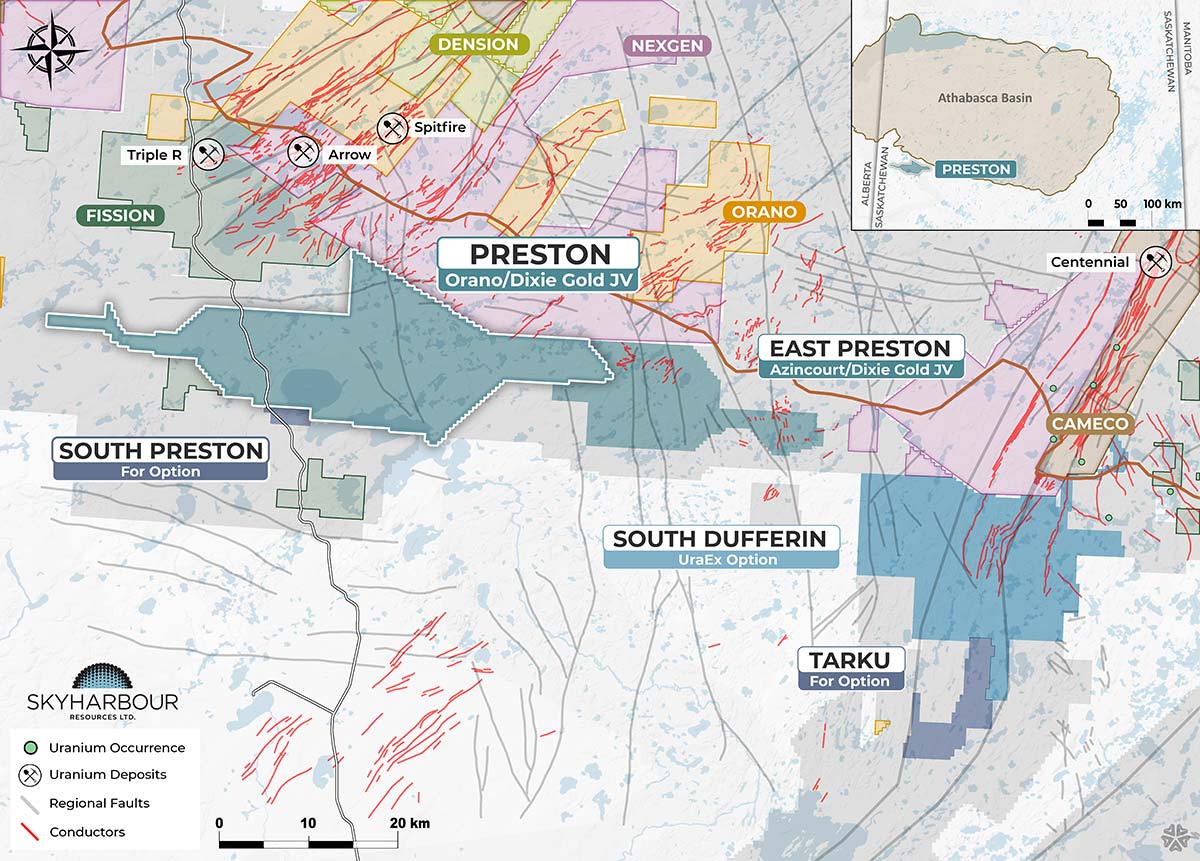

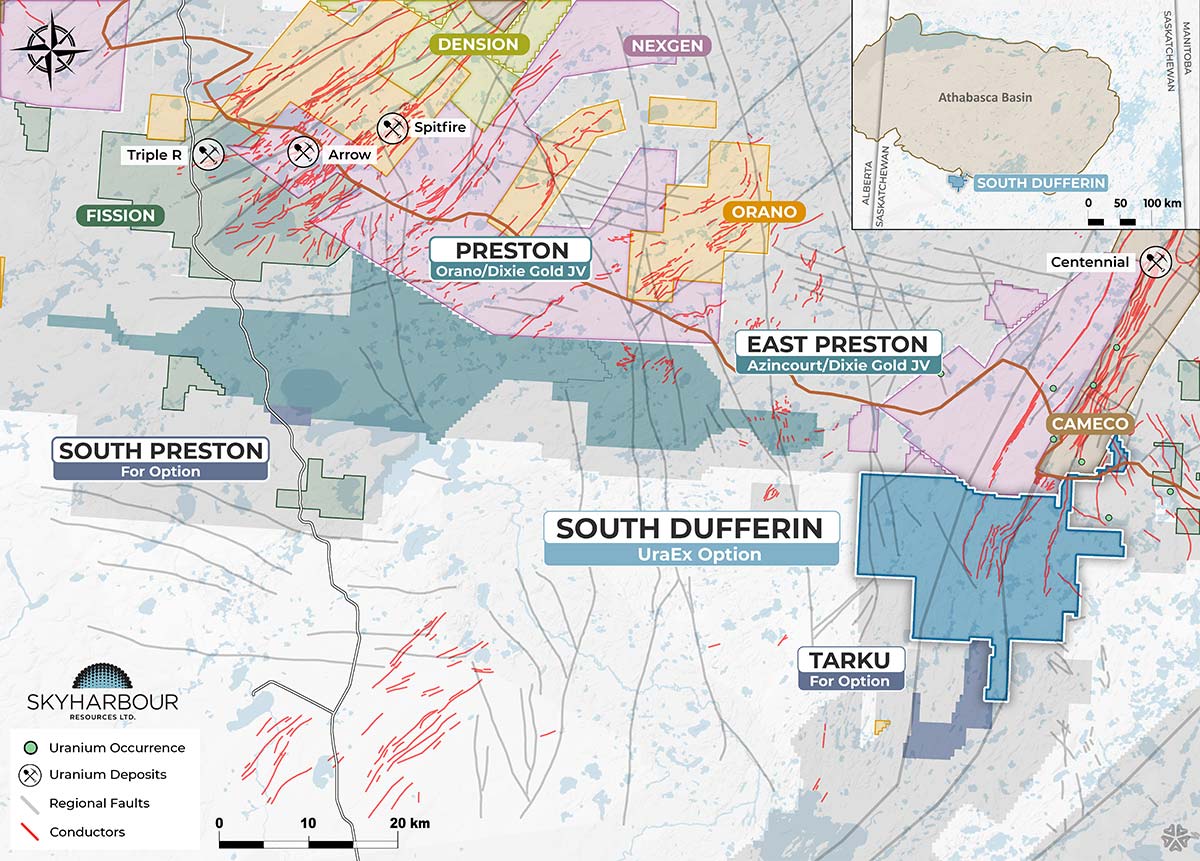

Preston Uranium Project

Skyharbour is joint-ventured with industry-leader Orano Canada Inc. at the Preston Uranium Project whereby Orano — France's largest uranium mining and nuclear fuel cycle company — has earned a 51% interest by way of exploration expenditures and cash payments. Skyharbour currently holds a 25.6% interest in the project.

![]()

The Preston project spans 49,635 hectares and is strategically located proximal to NexGen’s (TSX-V: NXE) high-grade Arrow uranium deposit and Fission Uranium’s (TSX: FCU) Patterson Lake South project, host to the high-grade Triple R deposit.

Orano recently completed a comprehensive 2024 field campaign which included a ground electromagnetic survey (ML-TEM) and a ground gravity survey with the final geophysical data from this field program pending.

An SGH soil sampling program with over 1,100 samples has commenced with additional news forthcoming. The SGH program will cover a large area and is a cost-effective, innovative exploration technique being used in the Athabasca Basin to vector in on uranium showings associated with certain hydrocarbons.

The 2024 field programs mark Orano’s first exploration activity at the project since 2020. Most recently, Orano commenced a renewed exploration program at the Preston Project, which includes a 6,000 to 7,000 metre helicopter-supported diamond drill campaign. The summer 2025 program is underway and will comprise approximately 26 drill holes targeting an average depth of 250 metres.

Primary drill target areas include the previously untested Johnson Lake grid as well as the Canoe Lake grid with the possibility of testing the recently surveyed FSAN-North and the West Preston Grids. Target areas are separated throughout the claim to ensure assessment credits are met across all claims while also testing prospective trends.

Russell Lake Uranium Project

![]()

Skyharbour recently entered into a major Strategic Agreement with Denison Mines to restructure the Russell Lake Uranium Project into four newly defined joint-venture areas, following Skyharbour’s consolidation of 100% ownership of the property. Under the agreement, Denison has acquired initial minority interests across the project while Skyharbour maintains operatorship over the majority of the land package and remains the dominant project owner. The transaction provides up to $61.5 million in total consideration through cash, shares, and exploration funding, marking a major endorsement of Russell’s exploration potential.

At the core RL Project Area, Skyharbour retains an 80% interest and full operatorship over 53,192 hectares—representing more than 70% of the original property. Denison holds a 20% interest and will fund its pro-rata share of expenditures up to a total of $10 million or until the end of 2029. This central claim block hosts several high-priority targets including Christie Lake, Blue Steel, NE Russell, Taylor Bay, and Kowalchuk Lake.

To the west, the Wheeler North JV has been structured with Skyharbour at 51% and Denison at 49% initially, covering 16,409 hectares near the world-class Wheeler River Project. Denison can earn up to a 70% interest through two earn-in phases totaling $25 million in exploration spending and $3.5 million in cash payments. This JV includes the Grayling and Fork Zones and will be operated by Denison.

Further west, the Wheeler River Inlier Claims have been reorganized into a 30% Skyharbour / 70% Denison JV. These 608 hectares sit entirely within Denison’s Wheeler River property and include the West Russell and C-Block targets. Denison will act as operator from the outset.

To the south, the Getty East JV comprises a 70% Skyharbour / 30% Denison split over the 3,105-hectare Little Man Lake area. Denison can increase its interest to 70% through staged exploration expenditures of up to $15 million over seven years, after which it may elect to become operator. Getty East lies along trend from Cameco’s Cree Zimmer and Key Lake operations.

This reorganization positions Skyharbour to continue advancing the largest and most prospective portion of Russell Lake as operator, while leveraging Denison’s technical expertise and financial strength across key areas of the project. The JV framework also provides a clear path for systematic exploration, discovery potential, and staged value creation across one of the most strategically located uranium land packages in the Athabasca Basin.

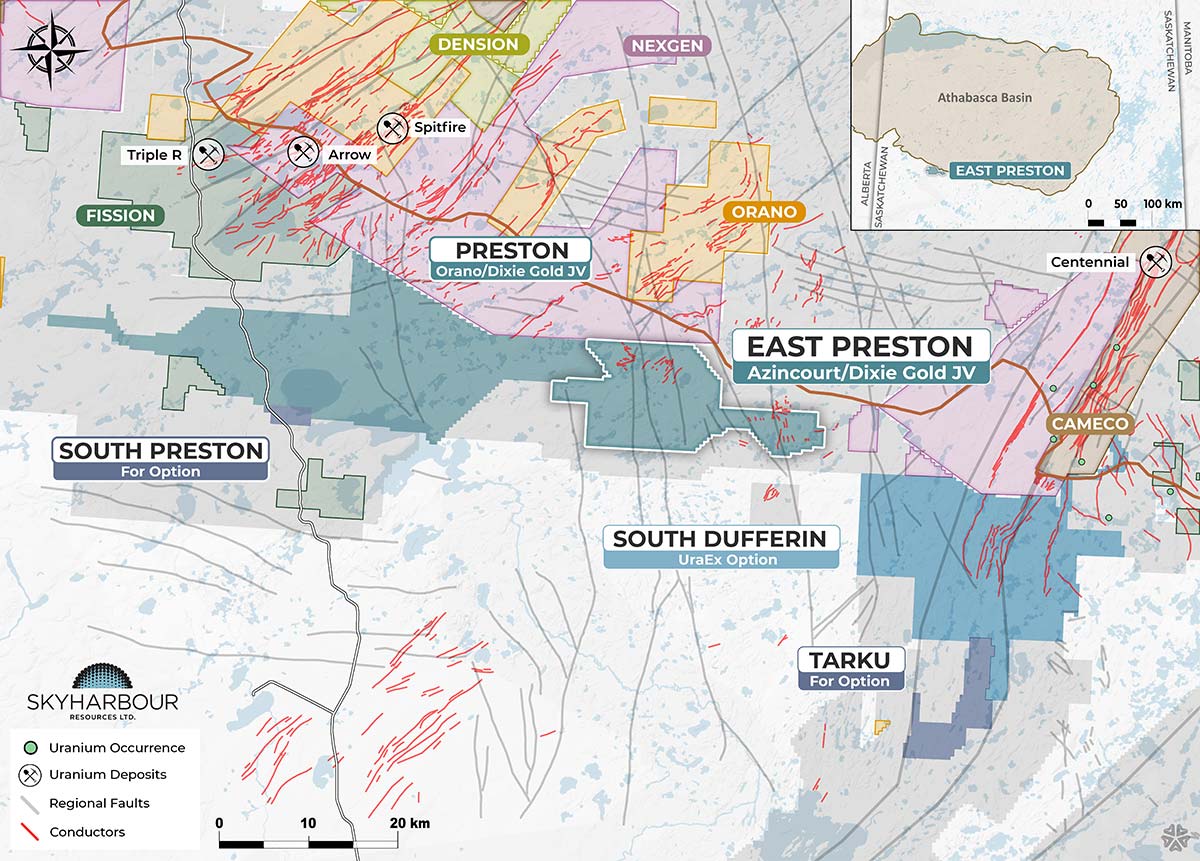

East Preston Uranium Project

Skyharbour is joint-ventured with Azincourt Energy on the neighboring East Preston Uranium Project (see below) whereby Azincourt has earned a majority interest through exploration expenditures, cash payments, and share issuance. Skyharbour maintains a 9.5% interest in the project.

![]()

Azincourt completed a 3,000-meter, 13-hole drill program at East Preston in Q3 2023.

Although not an official discovery as of yet, it’s important to note that numerous Athabasca-based uranium deposits — including Key Lake, Millennium, and McArthur River — have been discovered by mapping out zones of alteration by way of the drill-bit.

To date, Azincourt has identified three distinct corridors at East Preston totaling over 25 km of combined strike length, each with multiple EM conductor trends.

Based on data collection from previous exploration and drilling, Azincourt recently completed a 2024 winter drill program consisting of 1,086 meters of drilling in four diamond drill holes. The priority for the 2024 drill program was to follow up on the clay alteration zone and elevated uranium that was identified in the winter of 2023 with a focus on the area of transition between the K and H Zones.

Analysis of the results shows several intervals with anomalous uranium enrichment within the clay alteration zones along the K and H- target zones. Uranium enrichment is identified as uranium (U) values and a uranium/thorium ratio (U/Th) above what would normally be expected in the given rock type or area. Follow up drilling is being planned for 2025.

Falcon Uranium Project

In Q2 2023, Skyharbour entered into an agreement wherein North Shore Uranium can earn-in up to a 100% interest in the Falcon Property in the Athabasca Basin.

North Shore completed a maiden drill program in 2024 which focused on several targets along a well-defined, dominantly northeast-southwest-trending EM conductor system at the southeastern end of the claim block. Results confirmed near-surface uranium mineralization at two of the first three targets drilled at Falcon during the maiden drill program, emphasizing the uranium exploration potential at this project moving forward.

North Shore recently completed a 2025 prospecting program at the Falcon Project that evaluated several priority target areas and identified multiple zones of elevated radioactivity in outcrop and boulder samples. The work included detailed field mapping and sampling, helping to refine the project’s geological model and highlight areas with strong potential for follow-up exploration. The results provide a solid foundation for advancing the next stages of target definition and planning future field programs.

The property contains 11 mineral claims, comprising approximately 42,908 hectares located approximately 50 km east of the Key Lake mine.

At Falcon, North Shore can earn-in an initial 80% of the project through C$3,550,000 in exploration expenditures, C$525,000 in cash payments as well as C$1,225,000 in share issuances over three years followed by the option to acquire the remaining 20% of the project from Skyharbour through a cash payment of C$5,000,000 plus C$5,000,000 in shares.

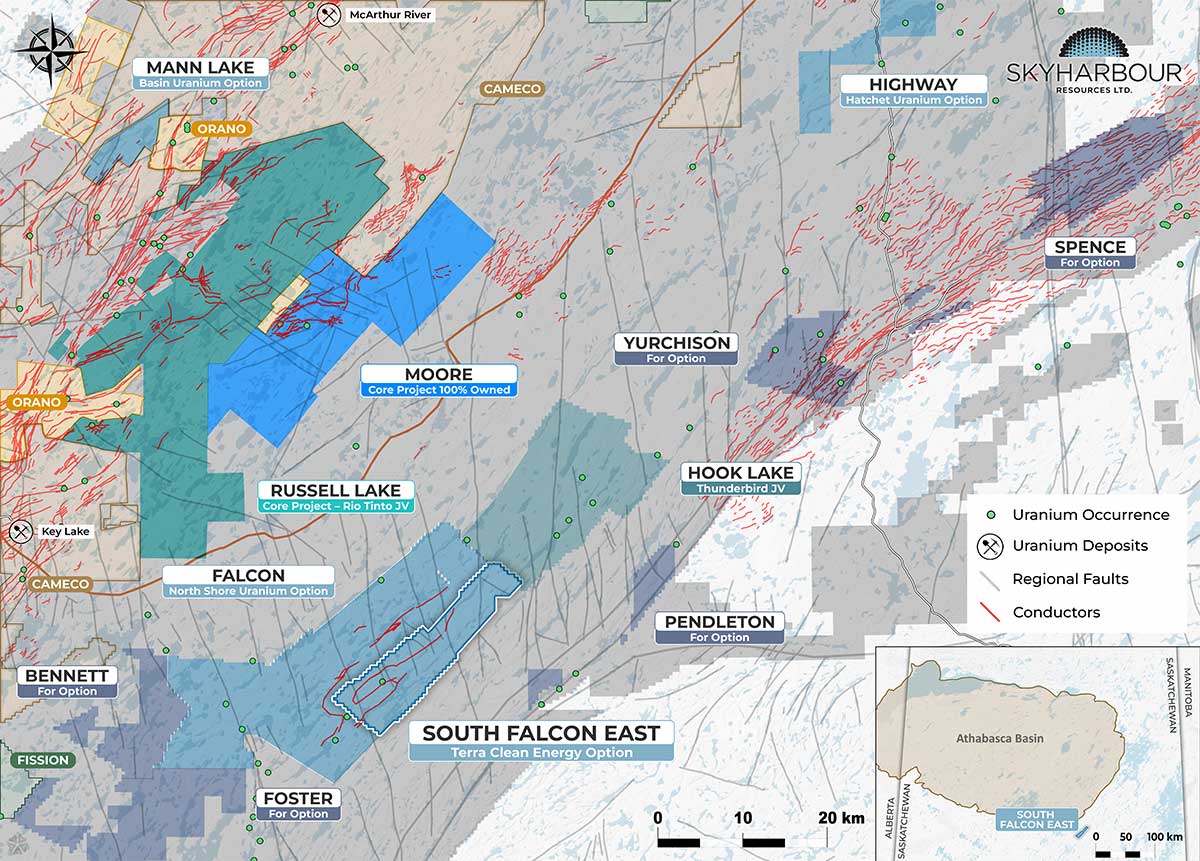

South Falcon East Uranium Project

The South Falcon East project is located in the eastern perimeter of the Athabasca Basin and contains a NI 43-101 inferred resource totalling 7.0 million pounds of U3O8 at 0.03% and 5.3 million pounds of ThO2 at 0.023%.

The project is currently optioned to Terra Clean Energy Corp. (previously Tisdale), whereby Terra can acquire an initial 51% interest and earn up to 75% by issuing 1.1 million Terra shares, spending C$10.5 million on exploration, and making cash payments totaling C$11,100,000 of which C$6,500,000 can be settled for Terra shares over the five-year earn-in period.

In 2025, Terra completed a helicopter-supported winter drill program at the South Falcon East Property, with seven diamond drill holes totaling 1,927 metres at the Fraser Lakes B Uranium Deposit. Results from 682 samples, analyzed by the Saskatchewan Research Council, revealed several broad zones of uranium mineralization. Notably, hole SF0065 intersected 18.1 metres at 0.03% U3O8, including 0.12% over 1.6 metres, while hole SF0067 returned the program’s best sample: 0.17% U3O8 over 0.5 metres. These strong results, particularly from holes SF0065 and SF0067, remain open to the north and east, indicating further potential along the NW-SE fault trend.

Terra is planning an extensive follow-up drill program this summer, consisting of approximately 2,500 metres of drilling.

![]()

Located just outside the Athabasca Basin approximately 50 km east of the Key Lake Mine, South Falcon East — which has seen plenty of historical exploration and has a small inferred resource — consists of a series of 16 mineral claims totaling 12,234 hectares.

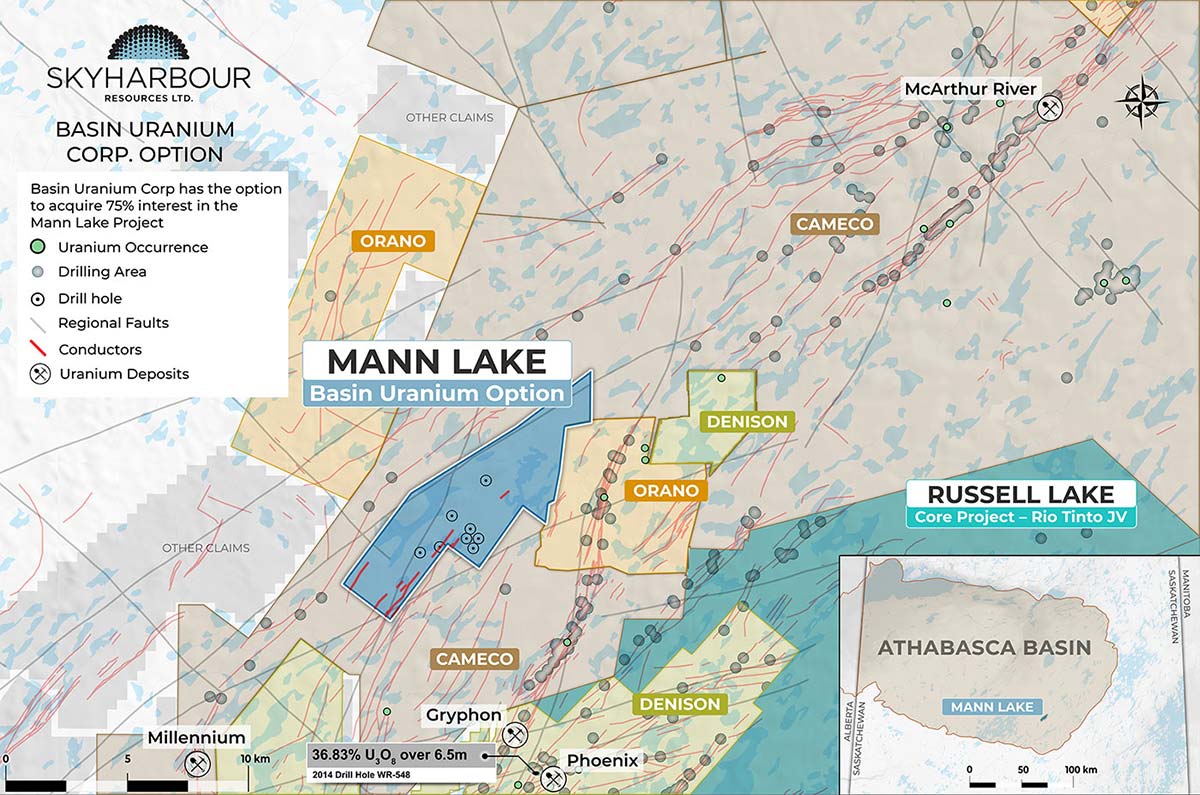

Mann Lake Uranium Project

Nexus Uranium Corp. (previously Basin Uranium Corp.) has an option to acquire a 75% interest in the Mann Lake Uranium Project from Skyharbour.

![]()

The project has seen more than C$5 million in previous exploration expenditures and is situated just 25 km southwest of Cameco’s McArthur River mine — the largest high-grade uranium deposit in the world — and 15 km to the northeast of Cameco’s Millennium uranium deposit.

In Q1 2023, Nexus Uranium received assays from a Phase-2, four-hole drill program across 2,776 meters at Mann Lake with multiple holes intersecting uranium mineralization in the targeted basement rocks.

Previous Basin Uranium CEO Mike Blady commented via press release:

“The completion of our phase two drill program represents the culmination of a very active and successful 2022 exploration program that was comprised of nearly 6,300 meters of diamond drilling and multiple geophysical programs at our Mann Lake project. We were able to advance this project from a grassroots-stage, one that had not seen any modern exploration techniques or benefitted from the last two decades of exploration understanding in the basin, through to a multi-phased diamond drill program that defined the unconformity and intersected uranium mineralization.”

To complete the previously announced 75% earn-in, Nexus Uranium Corp. must pay Skyharbour C$850,000 in cash plus C$1.75 million in shares and spend C$4 million on exploration over a three-year period. Nexus Uranium is planning exploration programs for 2024.

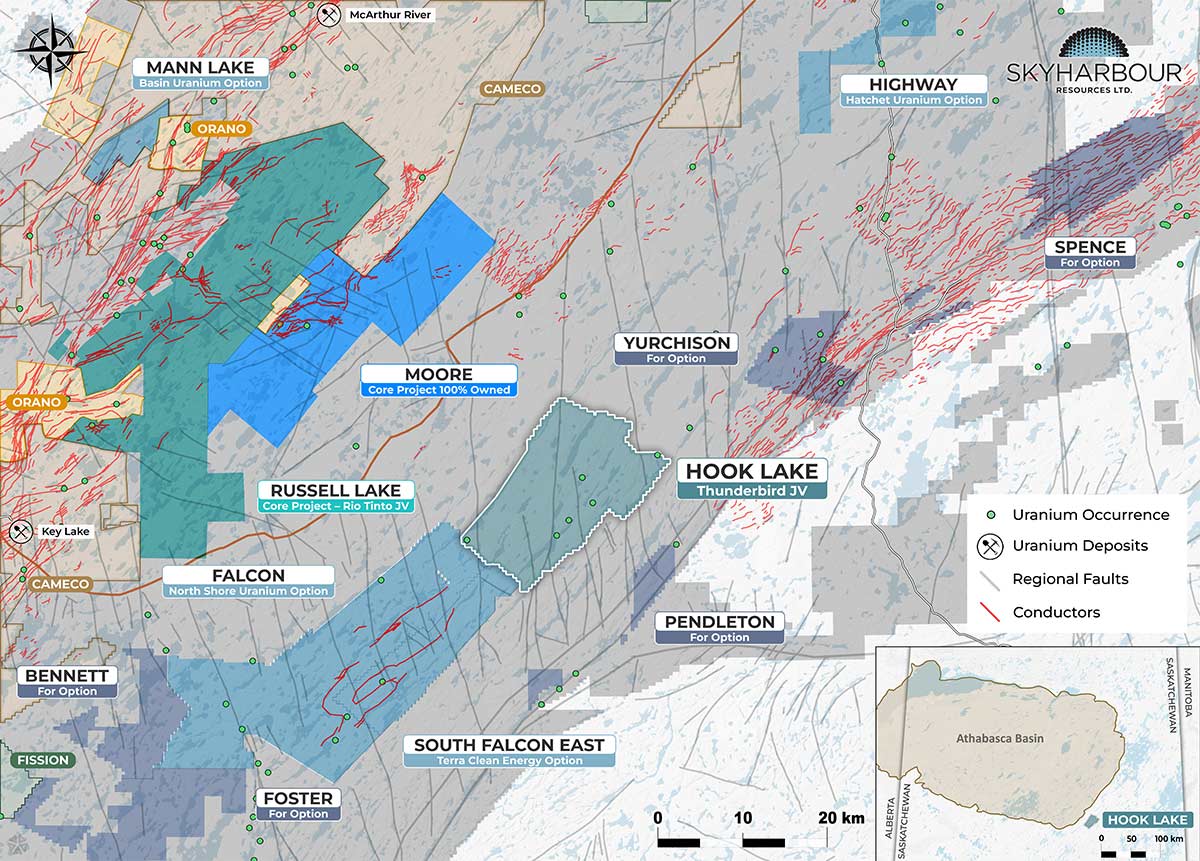

Hook Lake Uranium Project

At Hook Lake, Thunderbird Resources (previously Valor) announced that it had completed the third and final anniversary payment to Skyharbour under its earn-in option agreement, officially forming a JV partnership with Skyharbour. Thunderbird earned-in 80% through C$3,500,000 in exploration expenditures, C$250,000 in cash payments, plus share issuances to Skyharbour.

![]()

Thunderbird Resources completed its maiden drilling program at Hook Lake earlier in 2022.

The drill program comprised eight drill holes for 1,757 meters with six holes at the S-Zone prospect and two at the V-Grid prospect.

A total of 305 samples were collected from the program and submitted for assay with all results having now been received. The assays came in within the boundaries expected and highlight uranium mineralization at depth.

Those results, coupled with 11 new targets from a recently completed airborne survey, should allow for the delineation of new potential drill targets for next-phase drilling at Hook Lake.

South Dufferin Uranium Project

In Q2 2023, Skyharbour acquired 100% of the South Dufferin Uranium Project in the Athabasca Basin region from Denison Mines (TSX: DML)(NYSE-Amer: DNN).

![]()

A Definitive Agreement was recently signed in October of 2024 with UraEx Resources to earn an initial 51% and up to 100% of both the South Dufferin and Bolt Projects, collectively.

For an initial 51%, UraEx will issue common shares having an aggregate value of C$1,150,000, make total cash payments of $450,000, and incur $3,000,000 in exploration expenditures on both the South Dufferin and Bolt properties over a 3-year period.

UraEx has an option to acquire the remaining 49% by issuing common shares having an aggregate value of C$2,500,000, making cash payments of $1,200,000, and incurring $1,500,000 in exploration expenditures over an additional 2-year period.

The South Dufferin project is situated just south of the southern margin of the Athabasca Basin nearby to industry leader Cameco’s Centennial deposit.

UraEx has launched a fully funded summer 2025 diamond drill program at South Dufferin, marking the first drilling at the project in over six years. The program will total approximately 2,600 metres across 8 to 12 holes and is designed to test the southern extension of the Dufferin Lake Fault — part of the same structural corridor that hosts Cameco’s Centennial deposit to the north. The program is supported by a $1.5 million budget and will be helicopter-assisted throughout the summer.

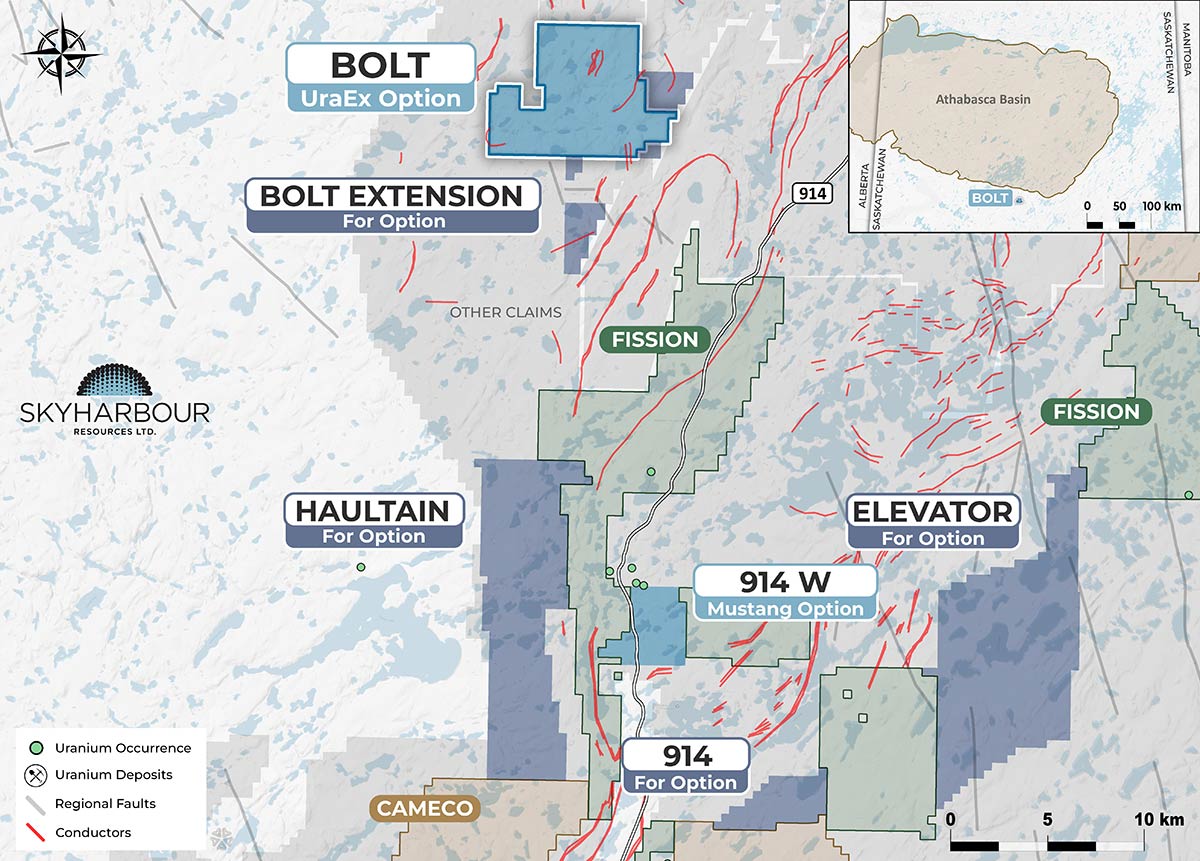

Bolt Uranium Project

The Bolt Project consists of two contiguous claims 100%-owned by Skyharbour totaling 4,726 hectares located approximately 7 km west of Highway 914 and about 32 km southwest of Cameco’s Key Lake Operation (which produced 209.8 million pounds of U3O8 at an average grade of 2.32% U3O8 from two deposits where ore from the McArthur River mine is currently processed).

The project has recently been optioned to UraEx Resources, whereby, for an initial 51% interest, UraEx will issue common shares having an aggregate value of C$1,150,000, make total cash payments of $450,000, and incur $3,000,000 in exploration expenditures on both the South Dufferin and Bolt properties over a 3-year period. UraEx has an option to acquire the remaining 49% by issuing common shares having an aggregate value of C$2,500,000, making cash payments of $1,200,000, and incurring $1,500,000 in exploration expenditures over an additional 2-year period.

Additional news on the advancement of both the South Dufferin and Bolt Projects will be forthcoming.

Newly Acquired Uranium Projects

In 2025, Skyharbour acquired, through staking, a number of additional 100%-owned prospective uranium exploration properties within the Athabasca Basin, significantly adding to Skyharbour’s existing holdings.

With a very active hybrid strategy as an explorer and prospect generator, Skyharbour, in Q4 2024, inked option partnerships on the 914W, Highway, Genie, Usam, and CBX/Shoe projects (see below).

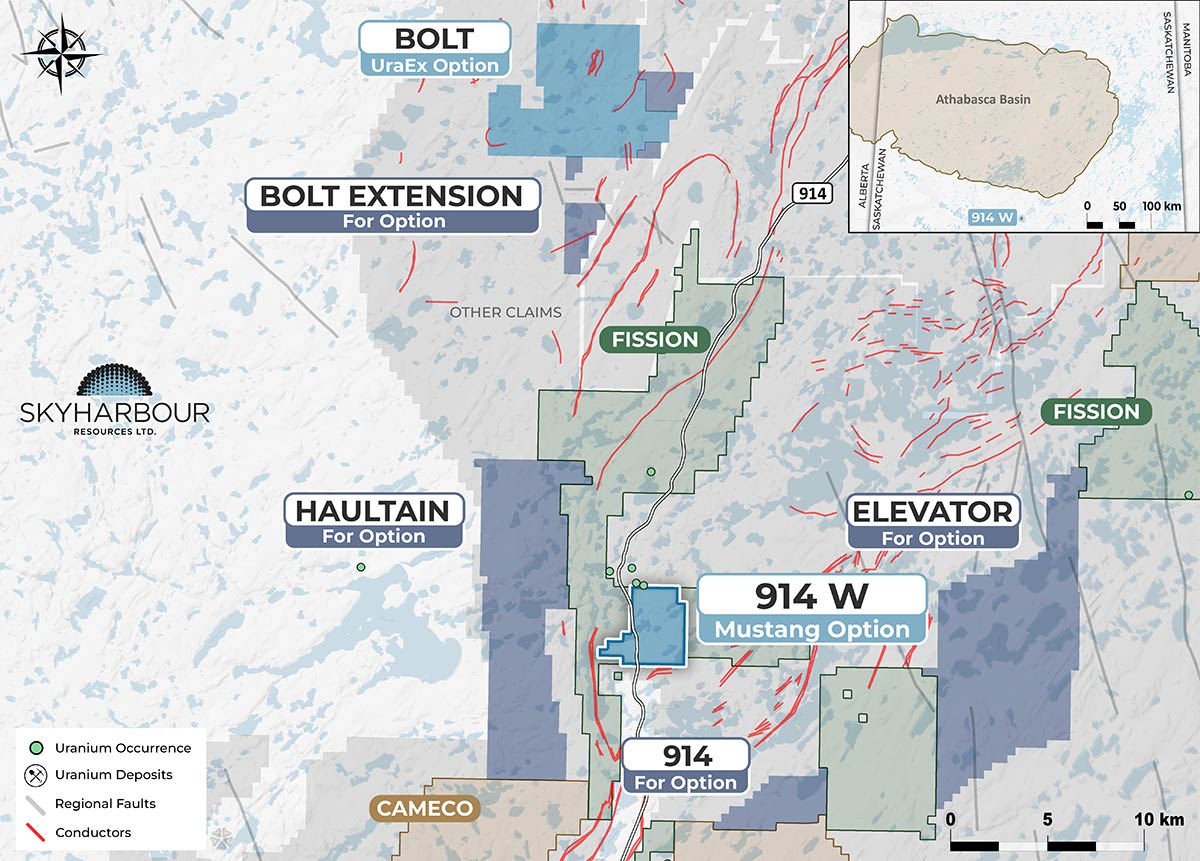

914W Uranium Project

On 14 November 2024, Skyharbour announced an option agreement with CSE-listed Mustang Energy Corp. on SYH’s 1,260-hectare 914W uranium project located ~48 km southwest of Cameco’s Key Lake operation in the Athabasca Basin. More recently, Mustang completed a 2025 program at the 914W Property, which included airborne geophysics and follow-up field sampling, which successfully outlined a broad conductive trend and areas of elevated geochemical response. These results have helped refine the property’s geological model and highlight zones with potential for unconformity-style uranium mineralization. The next steps will focus on additional target refinement through ground-based work and moving the most prospective areas toward future drilling.

Mustang Energy can earn a 75% interest in the 914W property by issuing common shares for an aggregate of C$480,000, making cash payments of C$275,000, and incurring C$800,000 in exploration expenditures over a three-year period.

Skyharbour will retain a 2% NSR royalty on the property whereby Mustang will have the right at any time to purchase one-half of the NSR royalty for a large cash payment.

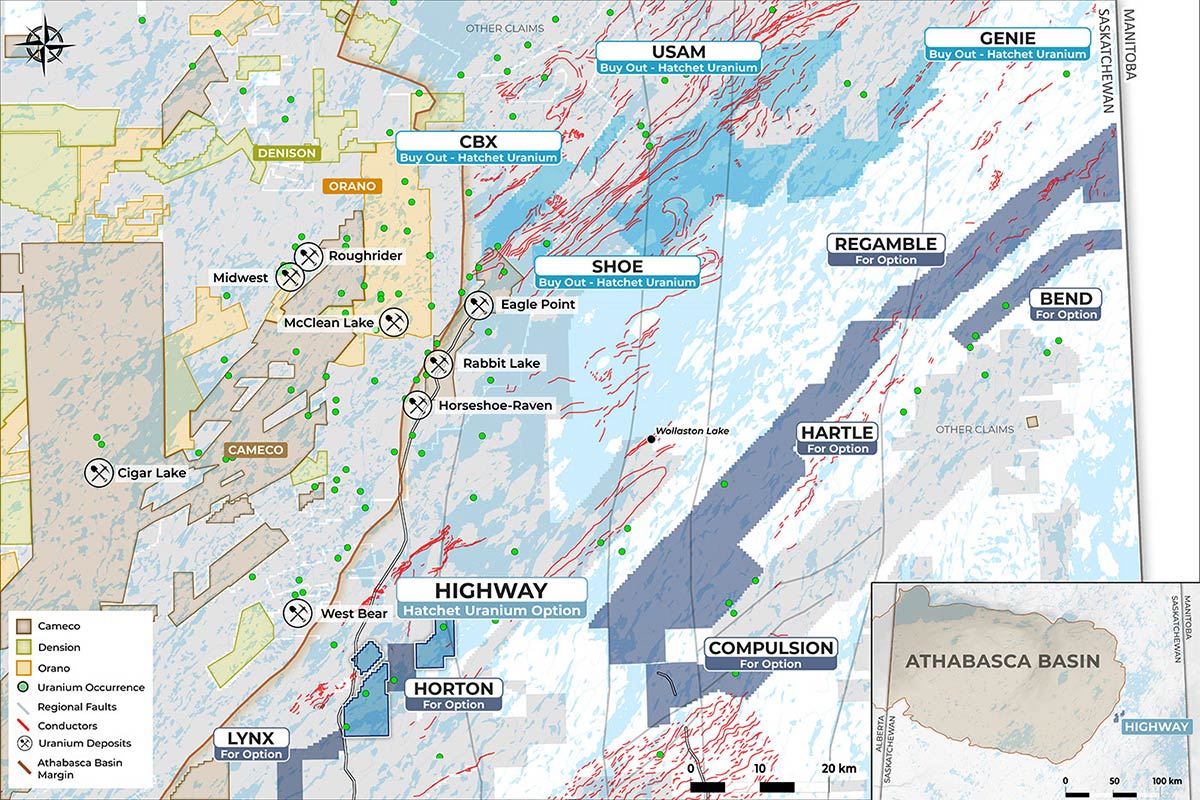

Highway, Genie, Usam & CBX/Shoe Uranium Projects

On 4 November 2024, Skyharbour announced an option agreement with private company Hatchet Uranium Corp. whereby Hatchet can earn an 80% interest in SYH’s Highway uranium property along with a 100% interest in SYH’s Genie, Usam, and CBX/Shoe uranium projects — combining for 66,358 hectares in the Athabasca Basin.

Skyharbour CEO Jordan Trimble commented via press release:

“We are excited to enter into this partnership with Hatchet Uranium Corp. as they advance and fund these exploration properties going forward. We are confident in the capable team behind Hatchet as they have plenty of experience in the Athabasca Basin and we look forward to them unlocking value at these projects. We continue to execute on our strategy by adding value to our uranium project base in the Athabasca Basin through strategic partnerships and prospect generation, as well as focused exploration at our co-flagship Russell and Moore Projects.”

As part of the option agreement, Skyharbour will also receive shares of Hatchet Uranium amounting to 9.9% for the sale of the Genie, Usam and CBX/Shoe projects with SYH retaining a royalty and an ownership clawback provision on the claims.

Prospect Generator Business

Tallying up the numbers, Skyharbour has now signed earn-in agreements with partners that total to potentially over $76 million in partner-funded exploration expenditures and over $42 million in cash and share payments coming into Skyharbour, assuming that these partner companies complete their entire earn-ins at the respective projects.

These partner-funded projects will no doubt provide a steady stream of news flow well into 2025 while complementing Skyharbour’s ongoing drill programs at the co-flagship Russell Lake and Moore projects.

Exclusive Interview: Jordan Trimble, CEO, Skyharbour Resources Ltd.

We’ve done our due diligence on Skyharbour Resources… and we’re impressed with the company’s vast uranium property portfolio in the Athabasca, its partnerships with global uranium mining companies, and its highly-adept management team starting with CEO, Jordan Trimble.

Skyharbour boasts a highly impressive amalgamation of talent — one we firmly believe has what it takes to get the job done for early SYH / SYHBF shareholders.

It’s a team that includes none other than professional geologist and strategic advisor, Paul Matysek, who founded and led Energy Metals as CEO prior to its eventual buyout by Uranium One for US$1.5 billion in 2007. Also on the board is Denison Mines’ CEO David Cates.

These are the types of industry professionals you can have confidence in and that you want to bet on in this highly competitive industry.

Please enjoy our exclusive interview with Skyharbour president & CEO, Jordan Trimble.

Gerardo Del Real: This is Gerardo Del Real with Resource Stock Digest. Joining me today is the president & CEO of Skyharbour Resources — Mr. Jordan Trimble. Jordan, it’s great to have you on. How are you today, sir?

Jordan Trimble: I'm doing great. Thanks for having me on again.

Gerardo Del Real: Well, let's get right into it. I want to talk Skyharbour. You have a lot of catalysts. We talked briefly off-air about the sentiment in the uranium space and how now even the tech companies are starting to realize that the future is nuclear.

I've got to ask you because you are one of the most well-versed voices in the space what the sentiment is like. I know you're on the conference circuit right now. What has the reaction to all of the news recently been on your travels?

Jordan Trimble: Well, it's positive, no question about it. I think the takeaway here is that we've seen some very significant headlines from various big tech companies, hyperscalers, signing notable agreements with nuclear utilities, advanced nuclear SMR developers. You've had just kind of a slew of positive headlines over the last several months.

And we did speak about the one that kind of got things going in September, which was the announcement of the restart of Three Mile Island and the major power purchase agreement signed with Microsoft, a 20-year power contract, buying electricity from the power plant at nearly double the market cost in the area of about $100 per megawatt hour. So Microsoft is getting behind that in a big way, and, again, no one would've thought that Three Mile Island was going to restart.

So there is a $1.6 billion refurbishment that'll take place over the next few years, and then they'll start generating electricity, again, from the Three Mile Island plant. And that'll be used to power, again, Microsoft's data centers, in particular, some of the data centers used for their AI business.

And just in the last couple of weeks, we've seen a few other larger big tech companies falling into line as well, including Amazon. They announced several agreements, actually, including one with a company called Energy Northwest in Washington State that will enable the development of several SMRs that are expected to generate over 300 megawatts of electricity in the first phase. Now, that can increase to almost 1,000 megawatts total, so quite a significant project and agreement there.

They then followed that up with an agreement with utility company Dominion Energy in Virginia that would see them explore the development of an SMR project near an existing nuclear power plant owned and operated by Dominion. So Amazon gets into the mix with those several agreements. And then, we also saw Google.

Google announced an agreement with an advanced nuclear company called Kairos Power. And they've signed a master plant agreement, which basically creates a path to deploy a fleet of advanced nuclear power plants. In this case, up to 500 megawatts over the next, call it, 10 to 11 years. And that would see Kairos develop, construct, and operate these reactors, as well as sell the energy to Google under power purchase agreements.

So a number of the largest tech companies, these hyperscalers, are getting in on the action. Obviously, the underlying takeaway being with the advancement of AI and the data center requirements and just a much larger need and demand for electricity from these big tech companies. Nuclear, being the only source of emissions-free, baseload, reliable, scalable electricity generation, is the perfect fit.

A lot of these companies have net zero carbon goals. And in order for them to efficiently and effectively power the infrastructure that's required for their growing businesses, nuclear energy, and in particular going forward, the advent of small modular reactors is, I think, going to be an integral part of, again, providing the electricity and allowing for the growth within these companies.

Those were all positive headlines. We talk a lot about getting back to the fundamentals. These are flashy headlines; they're great news. They've certainly caught the market's attention. But really, what it's doing is unearthing to the average investor, the generalist investor out there, what we've already known about nuclear and the prospects for nuclear energy.

As a result, uranium as a commodity is showing the benefits of this technology, of this electricity source, and we're now seeing more capital, more generalist money, coming into the sector.

I still think it's early days. In terms of those flashy headlines and those flashy announcements, we’ve yet to really see that work its way into the market in terms of the supply-demand fundamentals and, particularly, the growing demand profile.

As we see these agreements and these plans come to fruition, I believe you're going to see that move the uranium price much higher as the demand profile continues to expand and grow, especially in the West. We haven't yet seen that take place… but over the next few years, we will see that happen.

We’ve talked about this at length but you've got a very tenuous situation right now on the other side of that equation with supply. So the markets continue to bifurcate East versus West.

And one of the other big announcements out in the last few weeks was a major agreement signed between Kazatomprom and China's CNNC, the China National Nuclear Corporation, and actually two of the wholly-owned subsidiaries of CNNC.

They announced a major agreement with Kazatomprom to buy uranium, to buy nuclear fuel, from the Kazakhs. The value of the transaction, together with previously concluded transactions, exceeds 50% of the total book value of Kazatomprom's assets.

What this is showing the market is that the largest producer, globally, which is Kazatomprom in the country of Kazakhstan, represents over 40% of global primary mine supply. But more and more of that primary mine supply is being earmarked for China, and for Russia, and for other Eastern countries.

That, again, I think, is going to put upward pressure on prices going forward. As the market continues to bifurcate, Western producers are going to have to really ramp up production to meet the Western demand as we've just talked about. Whether that be demand from big tech and data centers, or the hyperscalers, or just the existing fleet.

We've seen announcements, not just with restarts as we've just talked about with Three Mile Island, but also there have been a number of reactors that have had their lives extended as well. The Western demand profile is quite robust and is growing much quicker than we thought it would even a few years ago.

Yet, Western supply has been relatively stagnant. And now, that Eastern supply, again, is being earmarked for Eastern consumption; a perfect example, as I just highlighted, with the Kazatomprom agreement with CNNC. Again, this is going to, I think, create a market that will be conducive to much, much higher uranium prices going forward.

Gerardo Del Real: I couldn't agree with you more. Let's talk Skyharbour specifically. You've had lots of news so let's get right into it. What's going on with Skyharbour? How are you positioned to close out 2024? And what can we look forward to in 2025?

Jordan Trimble: Yes, it’s going to be a mad dash to the finish line here this year. As we've spoken about in previous interviews, this is going to be our largest drill campaign we've ever carried out as a company in a single year.

We completed our initial winter and spring program earlier in the year, which totaled about 8,000 meters: about 1/3 of that at our Moore Lake project and the other 2/3 at our Russell Lake project. We announced a new high-grade discovery at the Russell Lake project at a new target called the Fork Zone.

The plan at Russell is to, obviously, go right back into that new Fork target and try to expand on that high-grade discovery where we had up to 3% U3O8 over half a meter, relatively shallow, and sandstone hosted.

It's a target that has not been well-understood historically and very much was not tested by previous operators. One of the reasons being is that it is located under the powerlines that actually run up and power the McArthur River Mine just to the north. So the historical geophysics were somewhat inconclusive as a result of that due to the powerline interference.

One of the things we're doing that we've just completed and announced here is an ANT survey, which stands for Ambient Noise Tomography. Basically, it allows us to go in there and back out, if you will, that powerline interference. It's a relatively new geophysical technique that's been used quite effectively by some other companies in the Athabasca Basin.

So it's kind of a cutting-edge new tool that we have. In terms of the requirements for this target to further refine it, it's kind of a new perfect survey for us to get a better handle on what's happening there. We've just completed that. We'll get the data here, and then that'll help further refine the target when we get back to drilling it here shortly.

We are planning to commence drilling very soon at Russell; we'll be following up on the success that we had earlier in the year with another 4,000 to 5,000 meters of drilling. We've also been wrapping up a few thousand meters of drilling at our Moore Lake project. Again, this being a follow-up to the program earlier in the year, which delivered some notable shallow high-grade drill intercepts.

That phase of drilling will be wrapping up, and we're very, very pleased with what we've seen and what we've found in that program, including several step-out holes from multiple high-grade zones of mineralization. So we'll wrap that up and we'll wait for our phase on that. And then, like I said, we'll finish the last phase of drilling at Russell, which will take us right through to the end of the year.

When all is said and done, there will have been well over 15,000 meters of combined drilling across both projects completed with lots of news flow right through to the end of the year and into the new year. Then, we'll gear up for a busy 2025 with our main focus being on the Russell and Moore Lake projects.

We also just announced that we've officially formed the 51%-49% JV partnership with Rio Tinto. We've locked in that joint venture with them. Not a bad name to have as a JV partner, one of the world's largest diversified mining companies. We're a majority owner of the project and operator, and we'll work with Rio on the project going forward to advance the project.

And then, we have a number of partner companies, as we've spoken about, again, previously. Just in the last few weeks, we've had several announcements out from North Shore at the Falcon project announcing plans for a drill program early in the new year. Terra Energy, which was previously Tisdale, has announced plans for a drill program early in the new year as well at the South Falcon East project.

And at our Yurchison project, Madero Mining is currently earning in under an option agreement where they've announced plans for a couple phases of exploration over the next several months.

Of the eight current partner companies, three of those being JVs, five of those still actively earning in, we are expecting programs and news flow from at least half a dozen of them over the next six months. So we're well-positioned to take advantage of this rising tide, and, hopefully, we’ll continue to see positive headlines coming that the market's responding well to.

But like I said earlier, I think the next 6 to 12 months, given all of the positive news flow, once that really works its way into the market, you’ll see, obviously, the uranium price respond to it. And as a result of that, you'll see, I think, a very, very strong next 6 to 12 months for the uranium equities.

Gerardo Del Real: I couldn't agree with you more. I couldn't be more excited. For those of us who saw the writing on the wall years ago for uranium, it's really, really neat seeing it actually play out. I said it off-air when we chatted briefly but I think it's going to be a fun couple of years. Jordan, anything else to add to that?

Jordan Trimble: No, I think we've covered everything. Lots of news to come, and we'll touch base in the coming weeks.

Gerardo Del Real: Look forward to having you back on. Thanks again, Jordan.

Jordan Trimble: Thank you.

The Skyharbour Resources Opportunity

The new uranium bull market has arrived…

“Uranium has likely reached a pivotal inflection point that could force the price higher by as much as three to four-fold over the next several years. For the first time in history, uranium has slipped into a persistent and widening deficit. We believe the results will be dramatic.”

That’s how Goehring & Rozencwajg Associates, LLC describes the state of the uranium market — and we couldn’t agree more!

After an extended consolidation in the space, the uranium spot price is now trading with strong support above US$78/lb with plenty of runway ahead.

Why? Several reasons.

The ongoing coups in Africa, coupled with other geopolitical factors — including Russia's invasion of Ukraine — are underscoring the need for clean energy sources that can contribute to a coordinated push for increased energy efficiency and energy security worldwide as a means of meeting net zero climate initiatives.

Nuclear energy is the answer… and uranium is the fuel source.

Earlier, we talked about ongoing uranium supply constraints with Cameco adding further fuel to the proverbial fire by announcing a 2.7 million pound uranium shortfall from its Cigar Lake and McArthur River mines.

It’s a sign of the times: As old, existing mines deteriorate, exhaust their resources, and ultimately shutter, the global uranium supply will become increasingly dependent on new discoveries, such those being sought and made in Canada’s prolific Athabasca Basin.

With a ~360 million pound shortfall expected by the end of the current decade, select small-cap uranium stocks — including Skyharbour Resources — are well positioned to benefit from what we expect will be a rising uranium price environment.

Led by President & CEO Jordan Trimble, Skyharbour Resources has amassed an impressive portfolio of 29 projects covering over 1.4 million acres in and around the prolific Athabasca Basin region — oftentimes referred to as The Saudi Arabia of Uranium.

The combination of 100%-owned and partner-funded projects (currently, eleven partner-funded projects being actively advanced by ten partner companies) makes Skyharbour one to watch in the newly-resurgent uranium bull market.

You heard directly from CEO Jordan Trimble. He says,

“... it’s going to be a mad dash to the finish line here this year… this is going to be our largest drill campaign we've ever carried out as a company in a single year… We are planning to commence drilling very soon at Russell… We've also been wrapping up a few thousand meters of drilling at our Moore Lake project… When all is said and done, there will have been well over 15,000 meters of combined drilling across both projects completed with lots of news flow right through to the end of the year and into the new year. Then, we'll gear up for a busy 2025 with our main focus being on the Russell and Moore Lake projects.”

As we discussed in detail, the next major leg up in the uranium price will be driven by utilities coming into the market to secure long-term U3O8 contracts. That’s happening now.

And it means we could be setting up for a potentially higher uranium price environment for years to come, particularly in this new era of AI-driven demand for carbon-emission-free electricity.

To meet that growing demand, the Skyharbour team is presently focused on advancing its co-flagship Moore and Russell Lake uranium projects located in the southeastern portion of the Athabasca Basin in close proximity to Denison's Wheeler River uranium project and Cameco’s McArthur River uranium mine.

The option agreement with Rio Tinto Exploration Canada (RTEC) at Russell Lake — which has an initial earn-in of 51% — provides Skyharbour, as operator, a key advanced-stage exploration project with strong backing from a powerful partner.

Additionally, Skyharbour has partners funding some of its other projects in the Athabasca Basin region. Most of these partner companies are planning exploration activities and/or drill programs that they'll be funding the lion's share of over the next 12-18 months.

It’s a brilliant model of advancing certain 100%-owned projects on their own — such as the flagship Moore and Russell projects — while joint venturing or optioning out other properties with the vast majority of exploration expenditures being on other companies’ dimes.

Skyharbour typically retains a minority interest in the property that’s being optioned out while also securing an equity holding in the partner company.

Collectively, Skyharbour has inked earn-in option agreements with partners that total to over C$38 million in partner-funded exploration expenditures, over C$29 million worth of shares being issued, and over C$21 million in cash payments coming into Skyharbour, assuming the partner companies complete their entire earn-ins at the respective projects.

With a robust portfolio of 29 Athabasca-based uranium exploration projects, ten of which are drill-ready, being advanced in a bullish uranium market — Skyharbour’s ~C$75 million market cap is considered small compared to some of its peers.

Plus, you really cannot overstate the significance of having three very well-established strategic partners in Denison Mines, Orano, and Rio Tinto Exploration Canada, as discussed throughout.

Skyharbour is also well-funded with over C$6 million in cash and equity holdings with more money and stock coming in from partner companies earning-in at the company’s secondary projects.

Now is an excellent time to begin conducting your own due diligence on Skyharbour Resources Ltd. — symbol SYH on the Toronto Venture Exchange and symbol SYHBF on the US-OTCQX Exchange.

A great place to start is Skyharbour’s corporate website. Sign up for updates directly from the company here. View the 2024 Corporate Presentation here.

And be sure to follow our exclusive interviews with upper management and much more.

— Resource Stock Digest Research

Click here to see more from Skyharbour Resources Ltd.IMPORTANT DISCLAIMER & DISCLOSURES

Resource Stock Digest, as a publisher, is not a broker, investment advisor, or financial advisor in any jurisdiction.

Please do not rely on the information presented by Resource Stock Digest as personal investment advice.

If you need personal investment advice, kindly reach out to a qualified and registered broker, investment advisor, or financial advisor.

The communications from Resource Stock Digest should not form the basis of your investment decisions. Examples we provide regarding share price increases related to specific companies are based on randomly selected time periods and should not be taken as an indicator or predictor of future stock prices for those companies.

Skyharbour Resources Ltd. has sponsored this report.

The information in this newsletter does not constitute an offer to sell or a solicitation of an offer to buy any securities of a corporation or entity, including U.S. Traded Securities or U.S. Quoted Securities, in the United States or to U.S. Persons. Securities may not be offered or sold in the United States except in compliance with the registration requirements of the Securities Act and applicable U.S. state securities laws or pursuant to an exemption therefrom.

Any public offering of securities in the United States may only be made by means of a prospectus containing detailed information about the corporation or entity and its management as well as financial statements. No securities regulatory authority in the United States has either approved or disapproved of the contents of any newsletter. Neither Resource Stock Digest nor any employee of Resource Stock Digest is registered with the United States Securities and Exchange Commission (the “SEC”): as a “broker-dealer” under the Exchange Act, as an “investment adviser” under the Investment Advisers Act of 1940, or in any other capacity. Resource Stock Digest, its owners, directors, and employees are also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

HIGHLY BIASED:

In our role, we aim to highlight specific companies for your further investigation; however, these are not stock recommendations, nor do they constitute an offer or sale of the referenced securities. Resource Stock Digest has received cash compensation from Skyharbour Resources Ltd. and is thus extremely biased. It is crucial that you conduct your own research prior to investing. This includes reading the companies' SEDAR and SEC filings, press releases, and risk disclosures. The information contained in our profiles is based on data provided by the companies, extracted from SEDAR and SEC filings, company websites, and other publicly available sources.

Resource Stock Digest, and its owners, directors, employees, and members of their households may own shares of Skyharbour Resources Ltd.. Therefore, Resource Stock Digest is extremely biased. Measures are in place such that no shares will be sold during the active awareness campaign.

HIGH RISK:

The securities issued by the companies we feature should be seen as high risk; if you choose to invest, despite these warnings, you may lose your entire investment. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures.

NOT PROFESSIONAL ADVICE:

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Resource Stock Digest, and all partners, members, and affiliates harmless in any event or claim. While Resource Stock Digest strives to provide accurate and reliable information sourced from believed-to-be trustworthy sources, we cannot guarantee the accuracy or reliability of the information. The information provided reflects conditions as they are at the moment of writing and not at any future date. Resource Stock Digest is not obligated to update, correct, or revise the information post-publication.

FORWARD-LOOKING STATEMENTS:

Certain information presented may contain or be considered forward-looking statements. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results or events to differ materially from those anticipated in these statements. There can be no assurance that any such statements will prove to be accurate, and readers should not place undue reliance on such information. Resource Stock Digest does not undertake any obligations to update the information presented or to ensure that such information remains current and accurate.