Click here to read important disclaimer & disclosures Click here to see more about Osisko Development Corp.

Shovel-Ready Gold Giant

NYSE: ODV | TSX-V: ODV

Permitted Canadian Developer Unlocking

Tier-1 Gold Asset with Scale

Feasibility-Stage Economics & District Scale Potential:

ODV is Built to Thrive in the 2025 Gold Bull Market

FLAGSHIP CARIBOO GOLD PROJECT READY TO BREAK GROUND IN BRITISH COLUMBIA

Next Major Canadian Producer Targeting 190K oz/Year with 2.07Moz Probable Reserves & District-Scale Upside

Click Here to Read Sponsor Disclosure

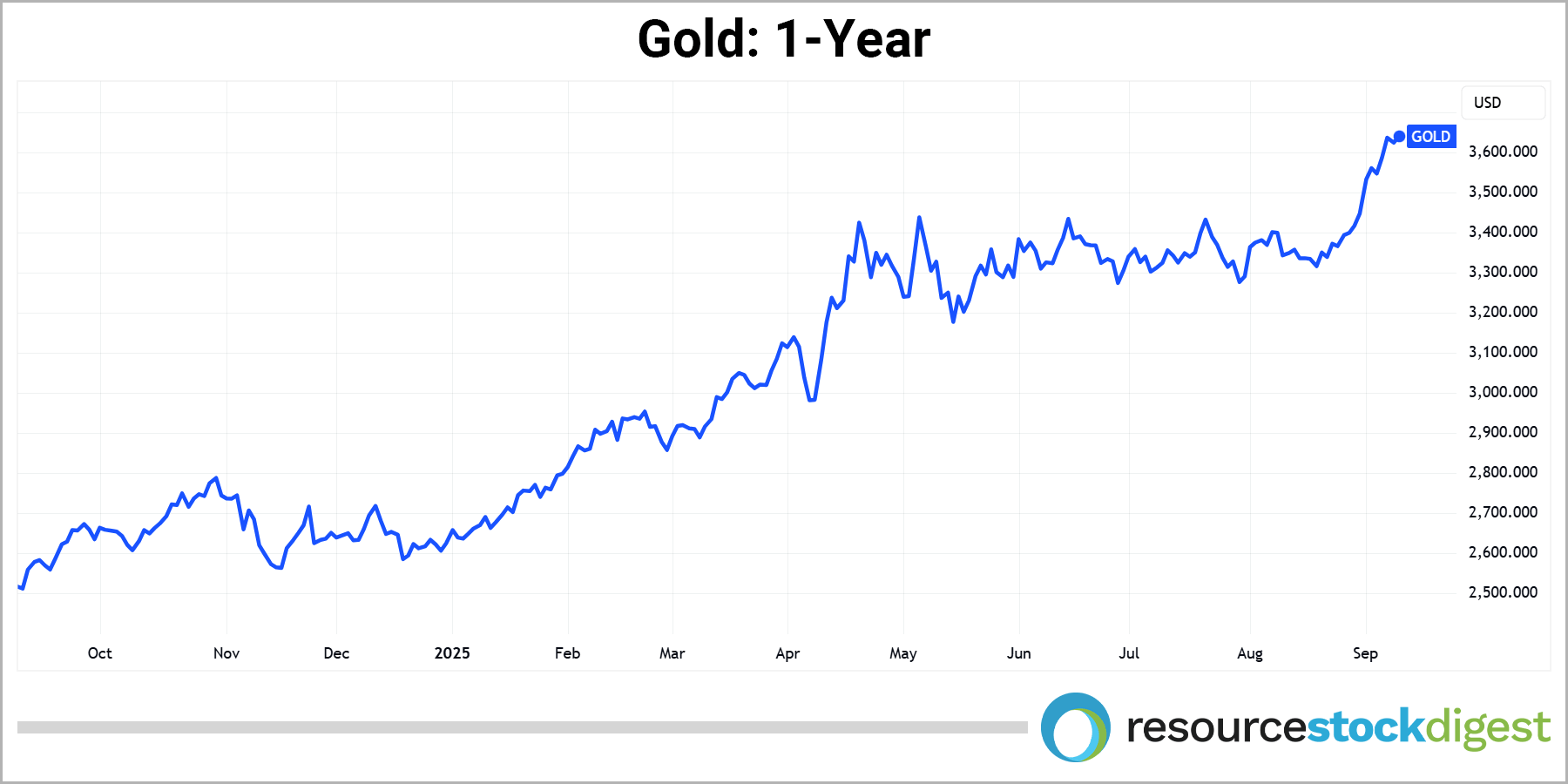

With gold trading at all-time highs above US$3,600 an ounce, Osisko Development Corp. (NYSE: ODV)(TSX-V: ODV) is uniquely positioned with a flagship, permitted, construction-ready gold project in a Tier-1 Canadian jurisdiction backed by a world-class team and a clear path to near-term production.

Armed with feasibility-stage economics and the infrastructure to build, Osisko Development (“ODV”) is moving fast to capitalize on one of the strongest gold markets in decades.

ODV is led by Founder, Chairman and CEO Sean Roosen — the visionary behind Canada’s largest gold mine, Canadian Malartic — and the guest of our exclusive interview coming up next.

Under his stewardship, Osisko has positioned itself as a future mid-tier gold powerhouse with a key project ready to break ground, a robust positive Feasibility Study in hand, and potential multiple district-scale assets lining the runway.

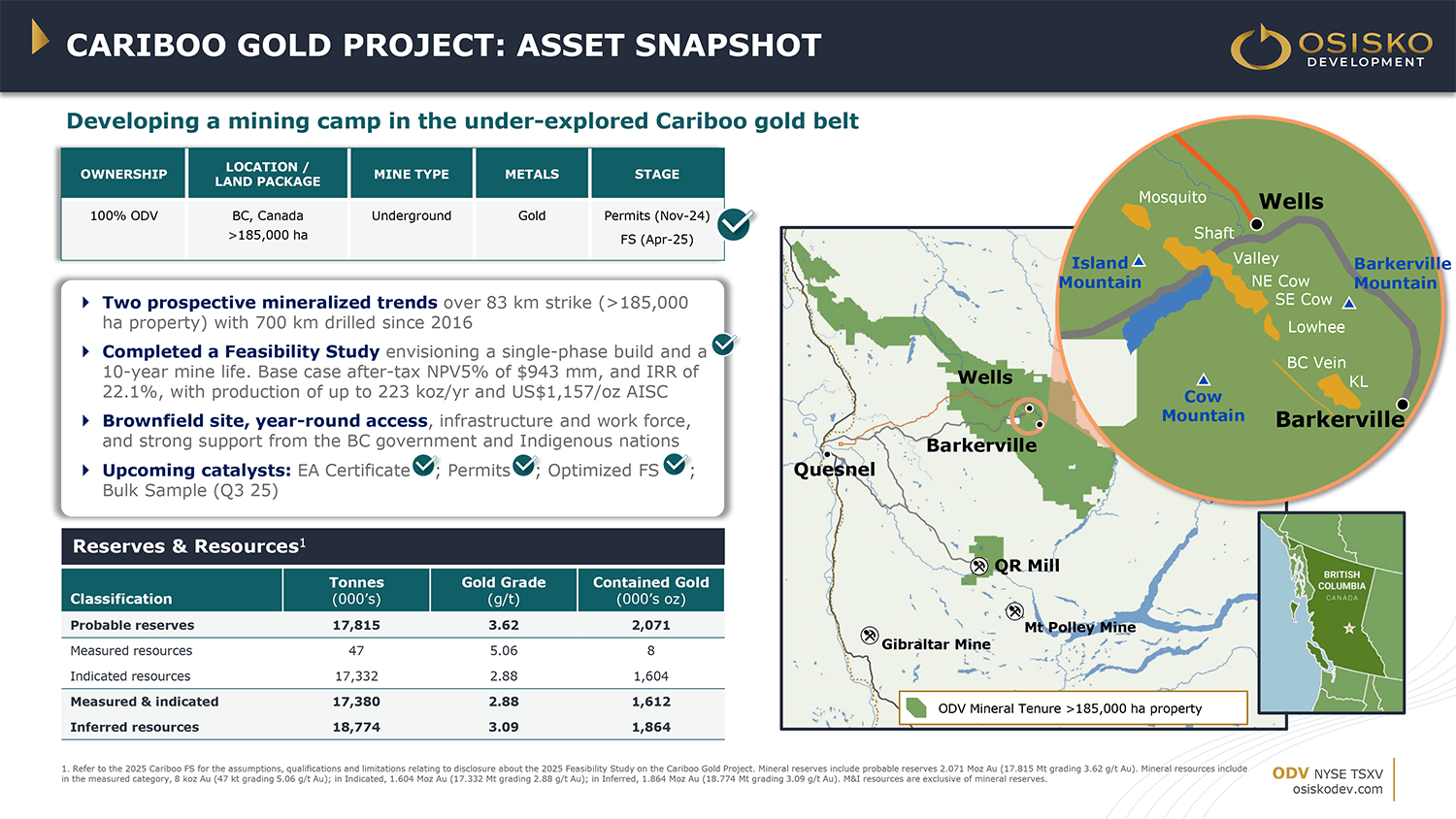

At the center of the story is the flagship Cariboo Gold Project — a 100%-owned, permitted underground project located in British Columbia’s legendary historic Cariboo Gold Belt.

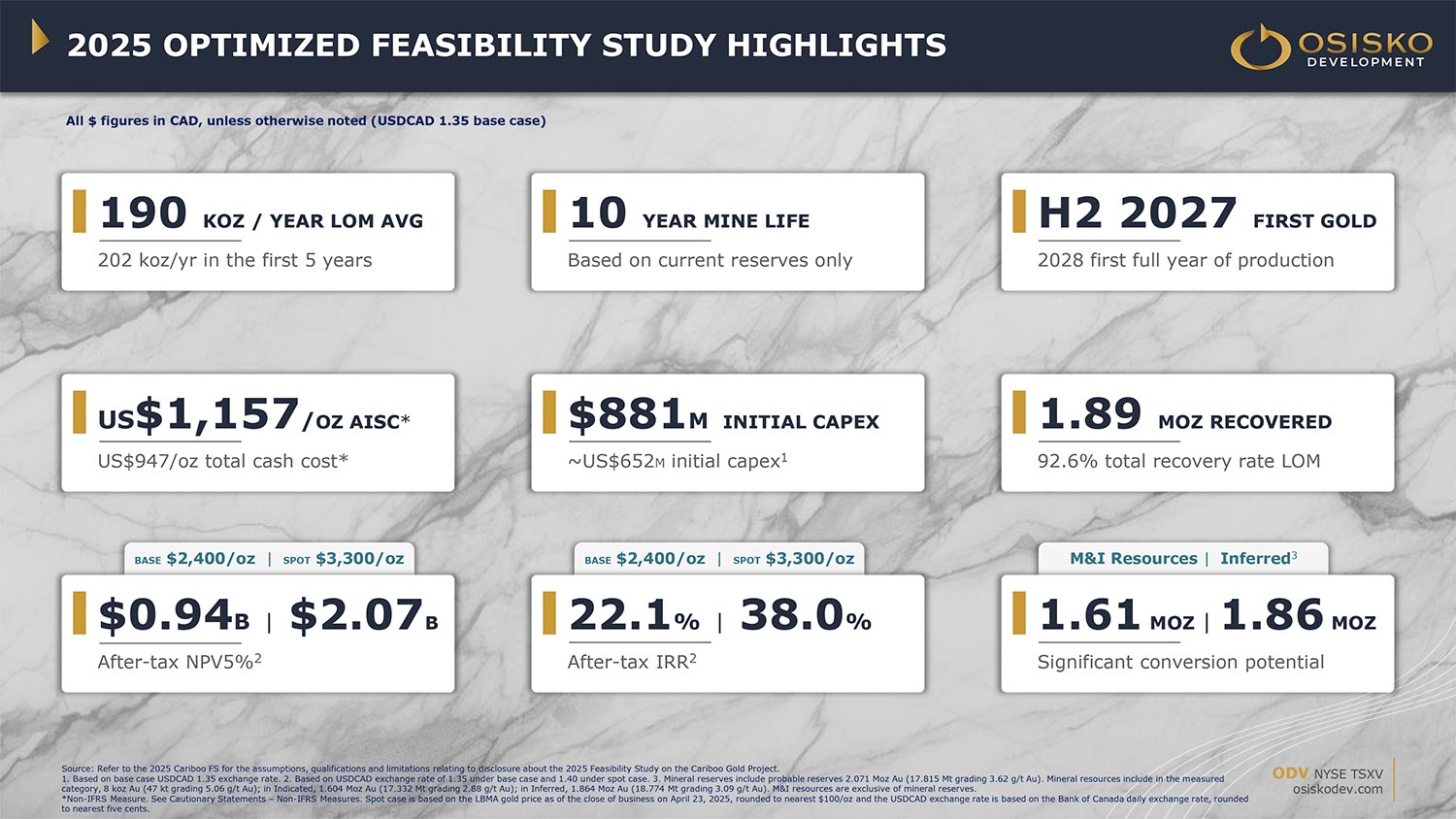

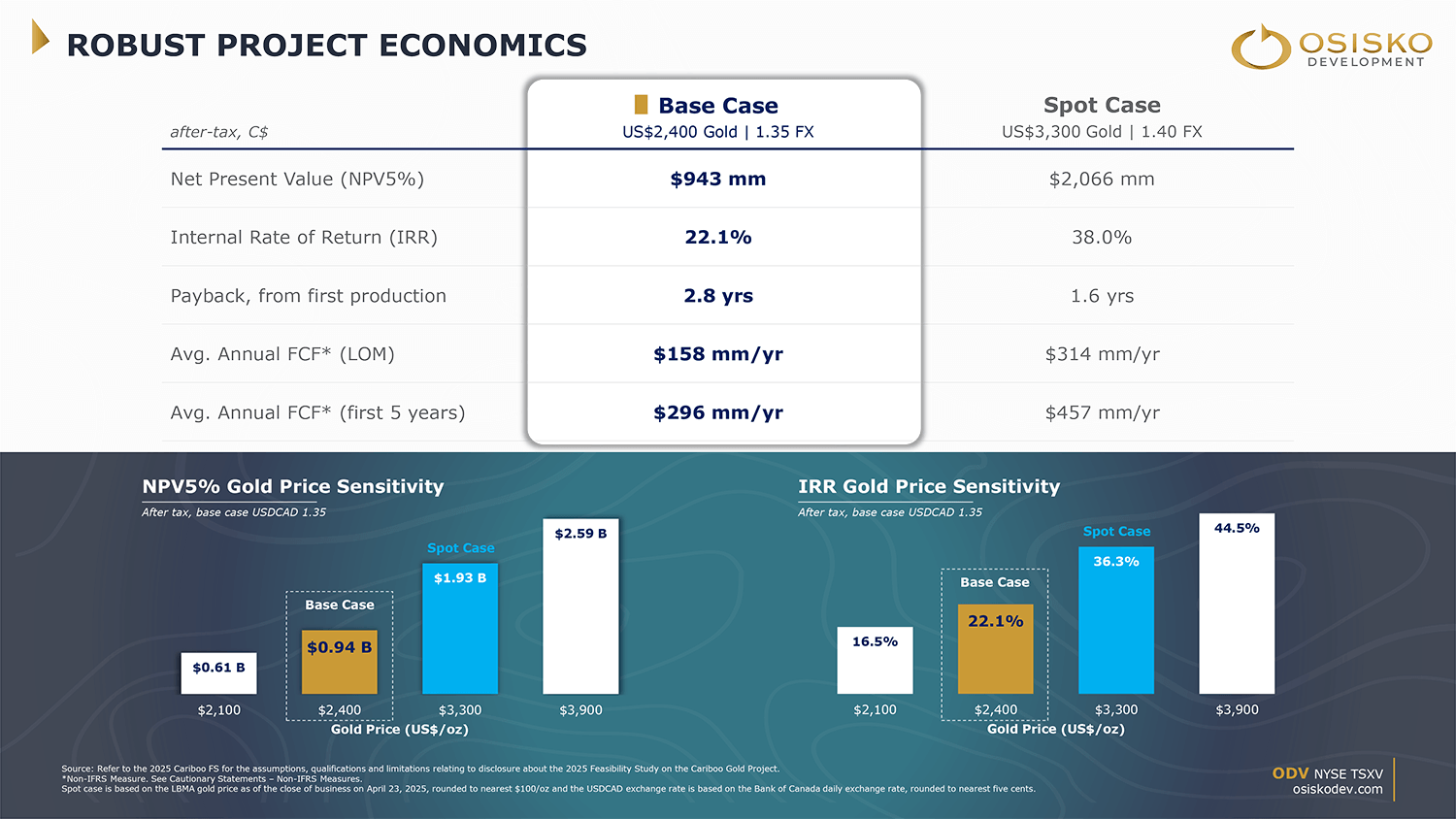

A newly updated Feasibility Study outlines annual production of 190,000 ounces of gold per year over a 10-year life with robust economics that include a post-tax NPV(5%) of C$943M and AISC of just US$1,157/oz (at base case gold price of US$2,400/oz). This improves to NPV(5%) of C$2.1B at gold price of US$3,300/oz.

But that’s just the starting point. The current mine plan only scratches the surface of a much larger system.

With close to 500,000 contiguous acres in the Cariboo District and a seasoned team already advancing exploration and pre-construction, ODV is quietly building what could be Canada’s next multi-million-ounce producer — right as capital floods back into the gold space.

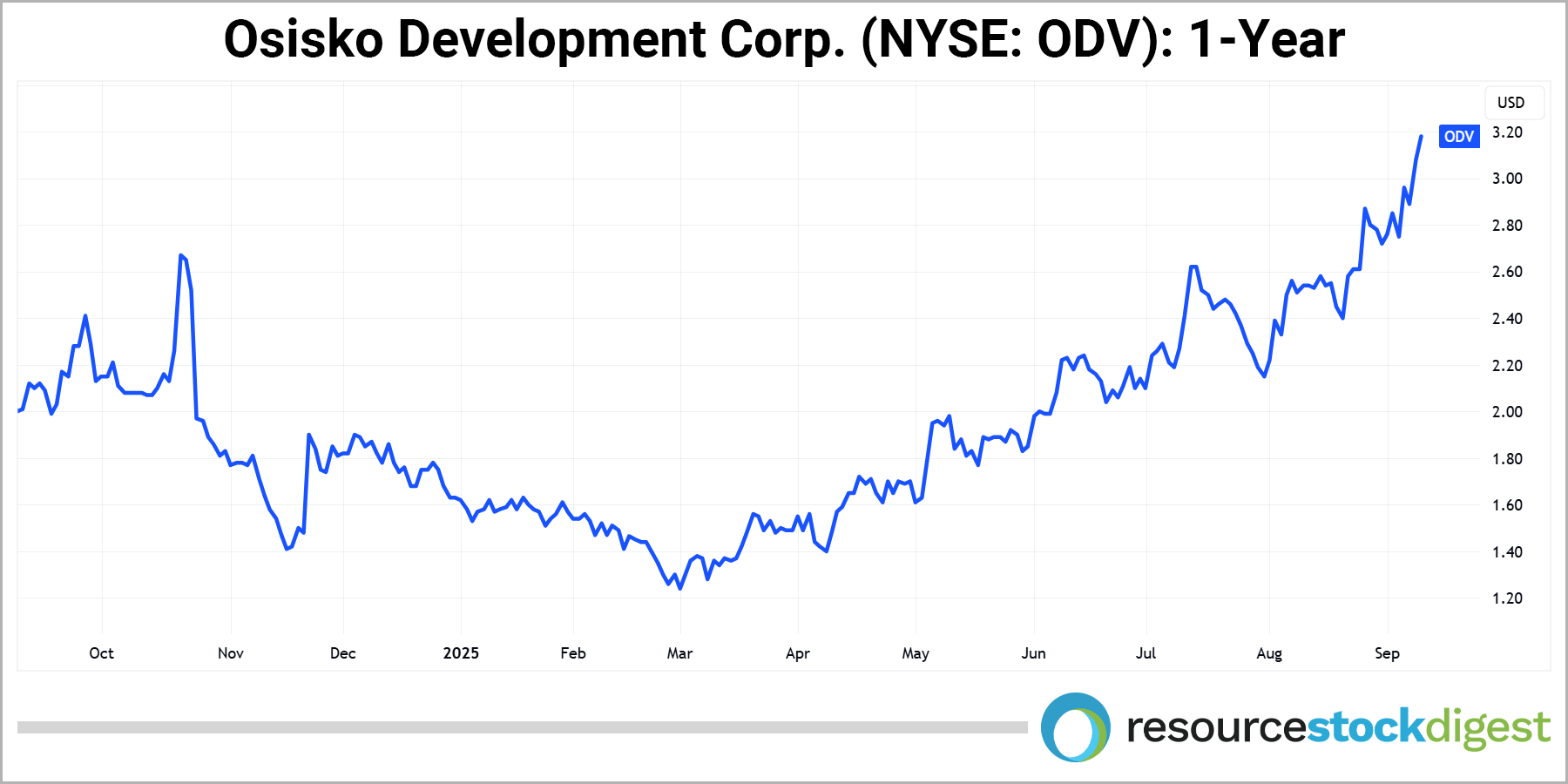

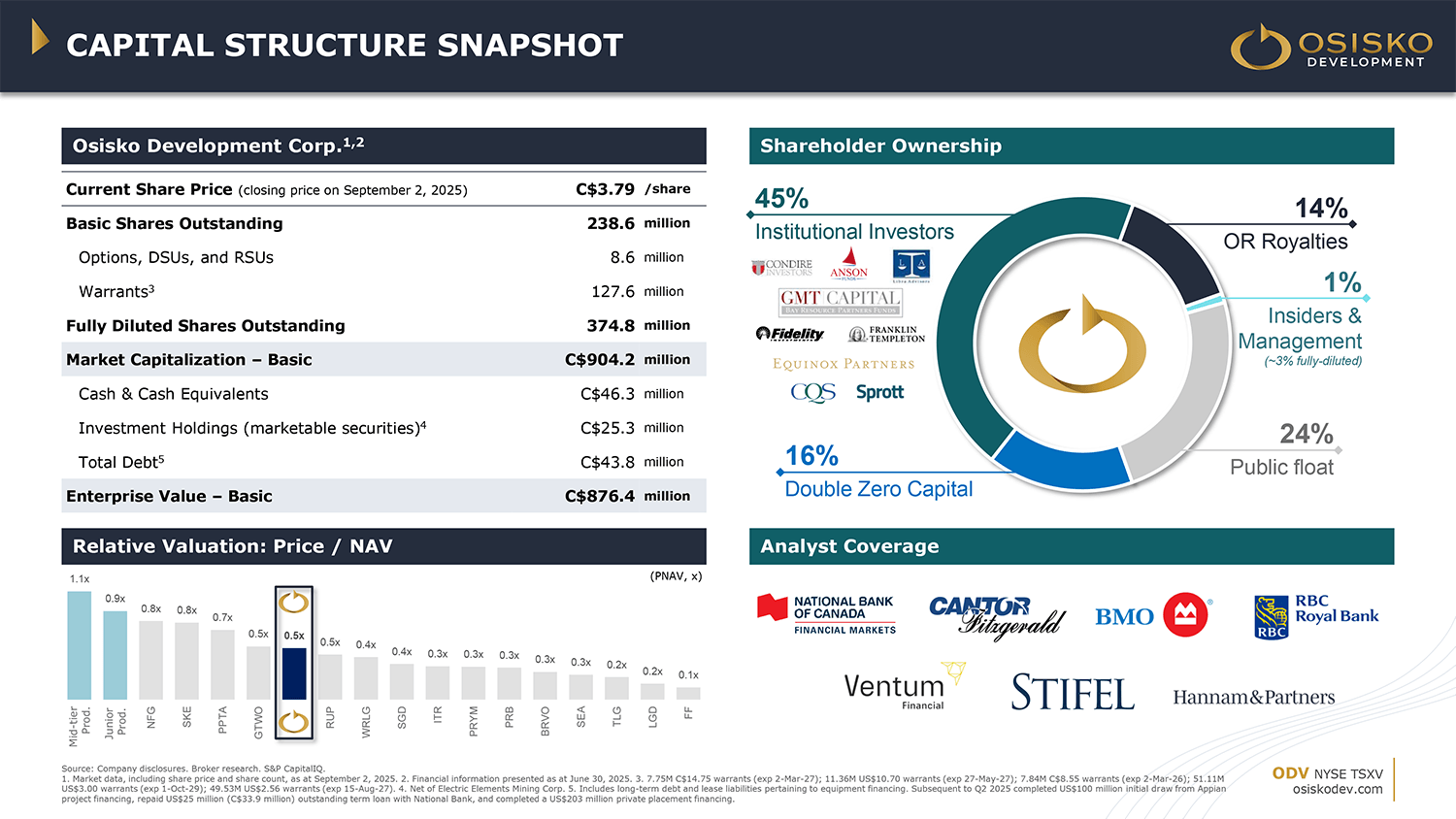

The best part? Shares are still flying under the radar at just ~C$4.50 with a ~C$900M basic market cap — a fraction of the company’s long-term value potential.

Next up, we’ll dive into why Cariboo could be “THE” gold project every major is watching in 2H 2025 — and why the timing couldn’t be better for speculators seeking exposure to near-term production, district-scale upside, and a permitted Tier-1 opportunity.

Leading the Charge: Flagship Cariboo Gold Project

Shovel-Ready, Permitted & With Significant Margin

Potential in BC’s Underexplored Cariboo Gold Belt

At the heart of Osisko Development’s growth strategy is its 100%-owned Cariboo Gold Project — a world-class, shovel-ready gold asset located in central British Columbia’s historic Cariboo Mining District, an area that has produced over 4 million ounces of gold to date.

Today, the Cariboo project is on the verge of a major transformation.

With gold prices trading at all-time highs above US$3,600 per ounce, the project’s strong economics and permitted status make it one of the most de-risked & well advanced, near-term development stories in the sector.

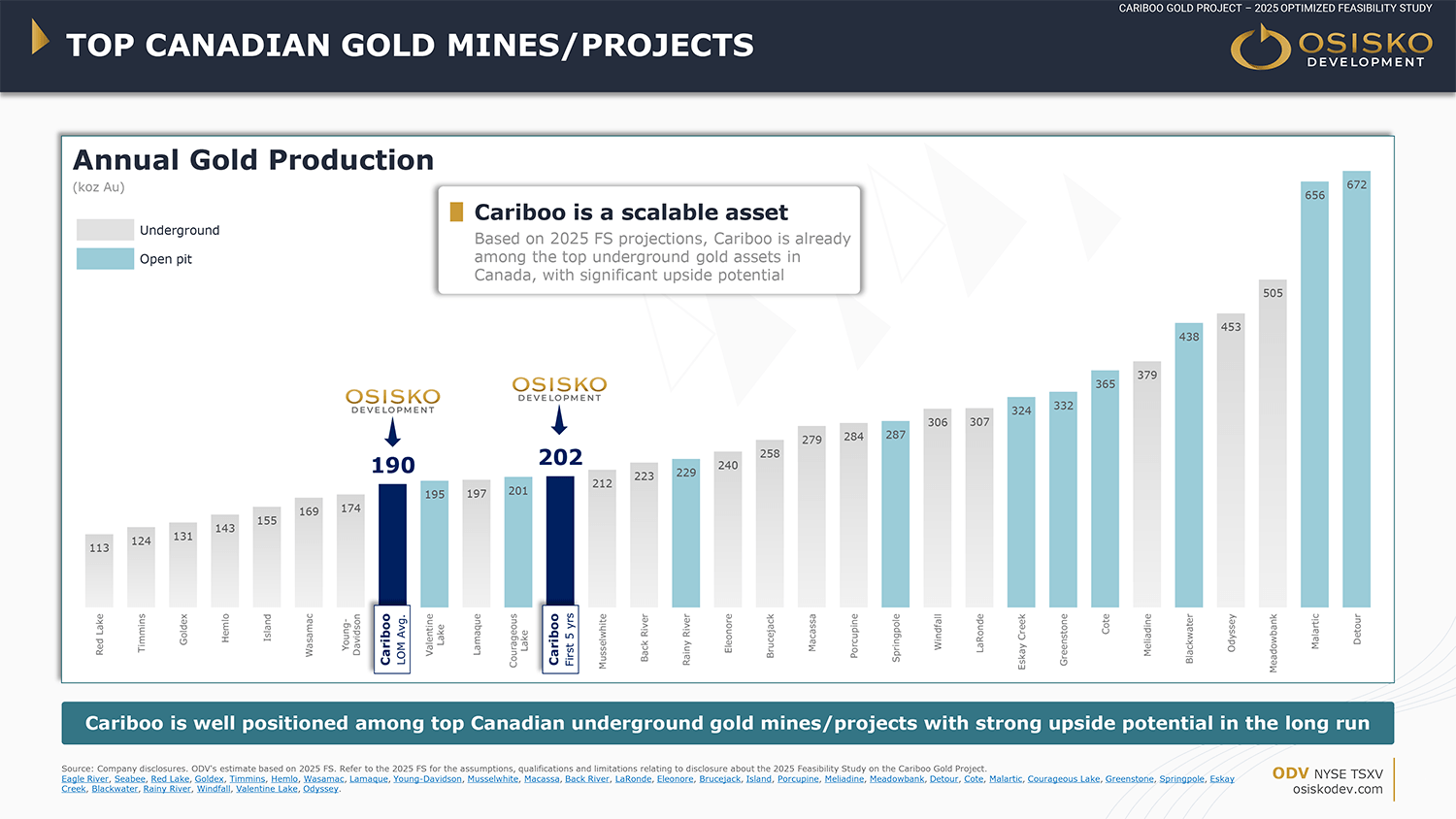

In April 2025, ODV delivered an updated NI 43‑101 compliant Feasibility Study outlining a robust underground operation with expected average annual production of 190,000 ounces Au over a 10-year mine life — totaling 1.89 million payable ounces.

At a US$2,400/oz base-case gold price, the project boasts an after-tax NPV(5%) of C$943 million and a 22.1% IRR. At current spot prices, those numbers jump to C$2.07 billion and a 38.0% IRR, respectively.

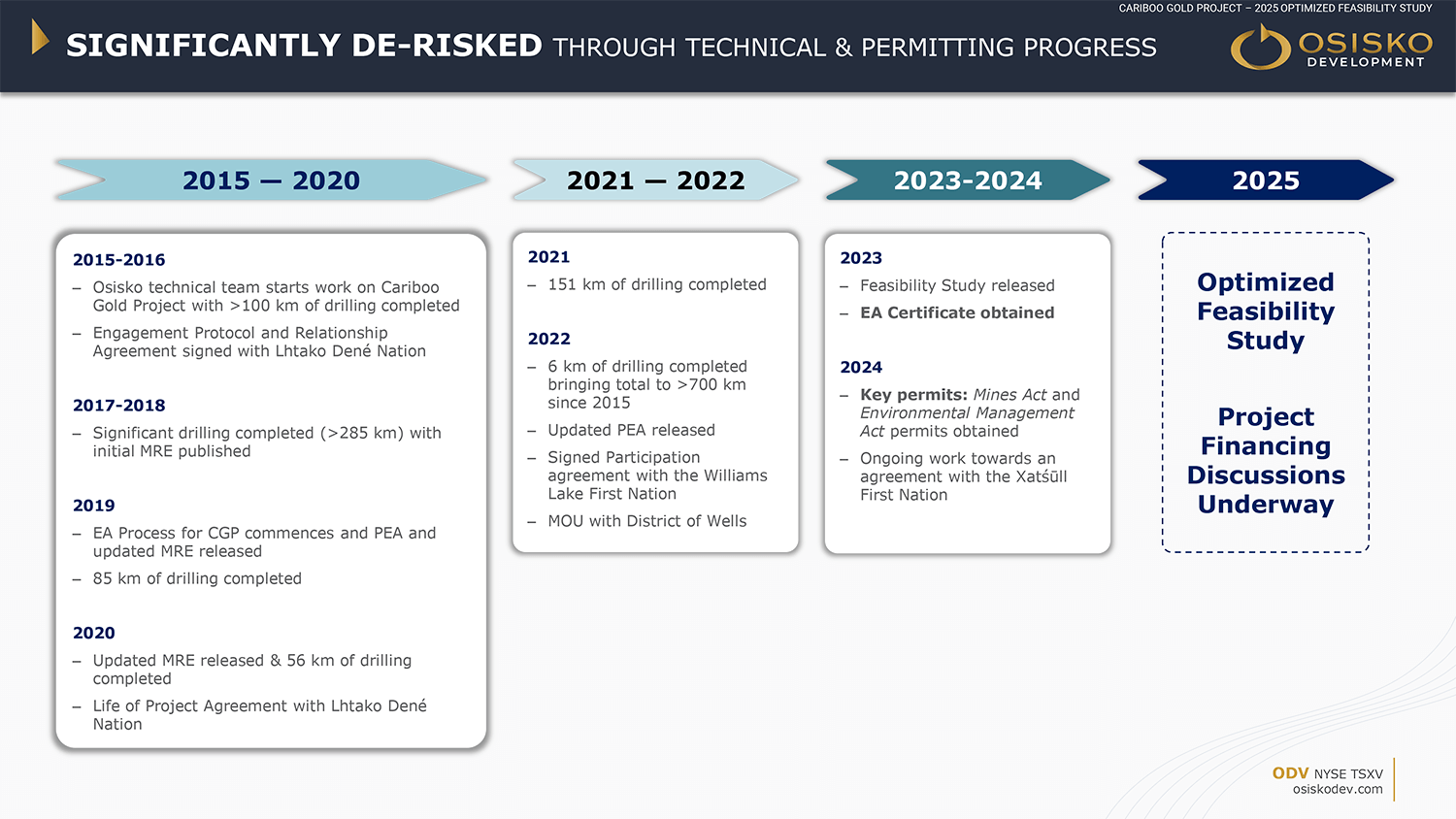

Importantly, Cariboo has already cleared every major regulatory hurdle.

The project was granted its Environmental Assessment Certificate in late 2023 and subsequently received its BC Mines Act and Environmental Management Act permits in Q4 2024 — placing Osisko in a unique position to begin construction in the near term once financing is secured.

Cariboo is designed as a low-impact, mechanized bulk mining operation operating at 4,900 tonne-per-day throughput, and designed to accommodate potential future expansions — offering scalability and strong margin potential from day one.

A recently initiated 13,000-metre infill drill program is underway and expected to generate a steady flow of news in H2 2025 — marking another key near-term milestone that could potentially drive the needle.

CEO Sean Roosen calls Cariboo a “high-quality asset with robust returns and significant upside potential,” emphasizing the scalability of the current mine plan and the vast surrounding land package for future discoveries.

How Cariboo Stacks Up: Big-League Potential, Early-Stage Valuation

With a fully permitted, construction-ready gold project in a Tier-1 Canadian jurisdiction, Osisko Development Corp. (NYSE: ODV)(TSX-V: ODV) is quietly approaching a turning point — and its current valuation suggests a major opportunity for early-stage speculators.

Consider this: Osisko’s flagship, 100%-owned Cariboo Gold Project outlines average annual production of 190,000 ounces over 10 years, totaling 1.89 million payable ounces of gold reserves.

A 2025 NI 43-101 Feasibility Study pegs the post-tax NPV(5%) at C$943 million using US$2,400/oz gold — increasing to C$2.07 billion at US$3,300/oz. Yet, the company trades at a basic market cap of ~C$900 million.

Compare that to two peer companies already in production:

Artemis Gold (TSX: ARTG), valued at ~US$5.2 billion, is ramping up construction at its Blackwater Mine — also in British Columbia. Blackwater hosts 8 million ounces of gold reserves with an initial 6 million tonnes per annum (Mtpa) throughput (Phase 1) expanding to 12 and 20 Mtpa in later phases. Its 2021 Feasibility Study outlines an after-tax NPV(5%) of C$2.15 billion and a 32% IRR, similar to Cariboo’s economics at higher gold prices.

Artemis Gold (TSX: ARTG), valued at ~US$5.2 billion, is ramping up construction at its Blackwater Mine — also in British Columbia. Blackwater hosts 8 million ounces of gold reserves with an initial 6 million tonnes per annum (Mtpa) throughput (Phase 1) expanding to 12 and 20 Mtpa in later phases. Its 2021 Feasibility Study outlines an after-tax NPV(5%) of C$2.15 billion and a 32% IRR, similar to Cariboo’s economics at higher gold prices. G-Mining Ventures (TSX: GMIN), valued at ~US$3.7 billion, declared commercial production in 2024 at its 100%-owned Tocantinzinho Gold Mine in Brazil. The open-pit project contains 2.03 million ounces of reserves and is expected to produce 175,000 ounces annually, slightly below Cariboo’s projected underground output, in a jurisdiction with greater permitting and geopolitical risk than Canada. They also have a second similar-sized asset to Tocantinzinho in Guyana.

G-Mining Ventures (TSX: GMIN), valued at ~US$3.7 billion, declared commercial production in 2024 at its 100%-owned Tocantinzinho Gold Mine in Brazil. The open-pit project contains 2.03 million ounces of reserves and is expected to produce 175,000 ounces annually, slightly below Cariboo’s projected underground output, in a jurisdiction with greater permitting and geopolitical risk than Canada. They also have a second similar-sized asset to Tocantinzinho in Guyana.

The key takeaway is that Cariboo stacks up exceptionally well across the board, including on key parameters such as project fundamentals, mineral reserves, and scalability.

At a basic market cap of ~US$650 million for Osisko — as compared to multiple “$BILLIONS” for Artemis and G-Mining — ODV trades at a fraction of the valuation of those two peer companies.

At present, ODV is advancing Cariboo project financing and expects a formal investment decision in the coming months with construction potentially kicking off in 2H 2025.

ODV secured a US$450 million project financing with Appian Capital Advisory in July 2025 — a well respected and technically driven private equity fund, which serves as another validation of the project’s quality.

In short, the timing couldn’t be more favorable for Osisko Development and ODV stakeholders.

With gold trading above US$3,600, final project financing being advanced, a final construction decision on deck, and all major permits in hand, ODV’s flagship Cariboo project offers a rare combination of scale, margin, and near-term production visibility — all in a Tier-1 jurisdiction.

Strategically located in one of Canada’s most mining-friendly regions — with access to clean hydro power, skilled labor, and established infrastructure — Cariboo is well-positioned to become a foundational mid-tier gold asset.

For speculators looking to position ahead of a potential re-rating, Cariboo stands out as one of the few fully permitted North American gold development stories still trading at an early-stage valuation.

Beyond Cariboo: Two More Shots-on-Goal

ODV’s Tintic and San Antonio Projects Add Scale,

Metals Diversity & District-Scale Growth

Tintic Gold-Copper Project: Utah, USA

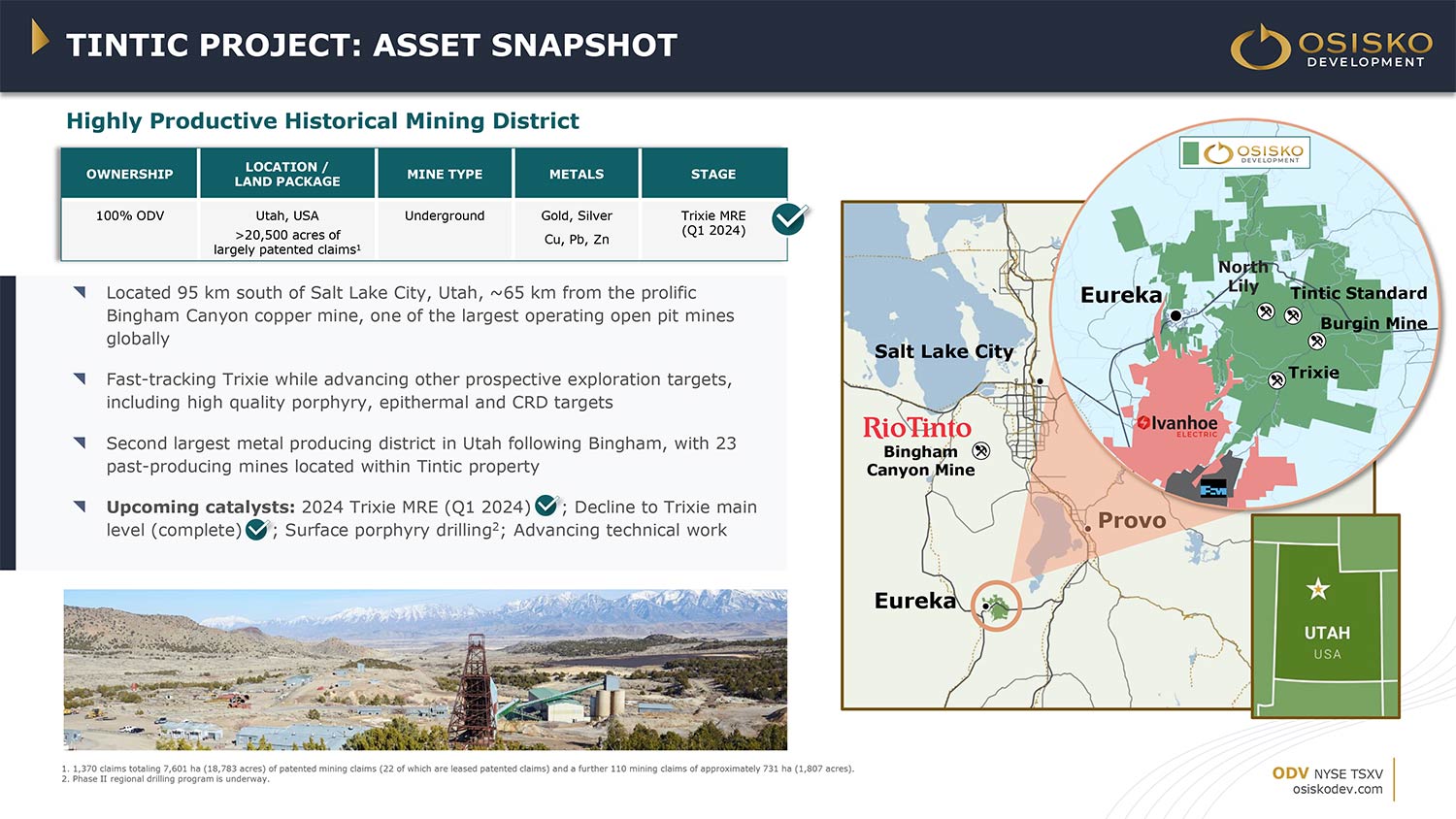

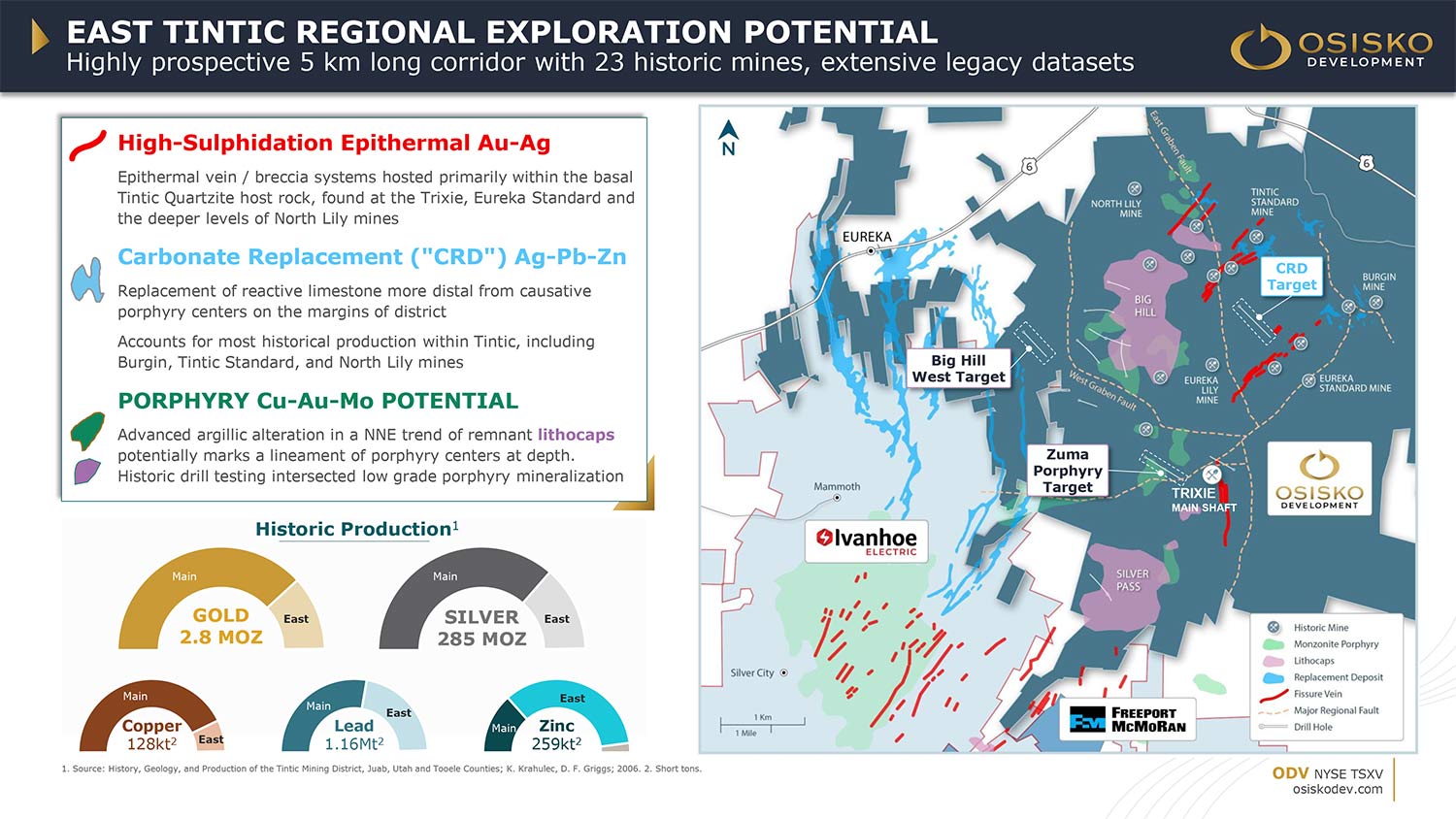

ODV’s 100%-owned Tintic Project is shaping up as a high-potential exploration play in one of the richest historical districts in the western US.

Located 95 km south of Salt Lake City in Utah’s East Tintic Mining District — a past-producing camp with over 2.5 million ounces of gold and 200 million ounces of silver recovered — the Tintic Project offers both gold upside and large-scale copper-gold porphyry potential.

Osisko is currently advancing a small-scale heap leach project retreating stockpiles and tailings material, which produced 1,393 ounces of gold in Q2 2025, and expected to continue until year-end.

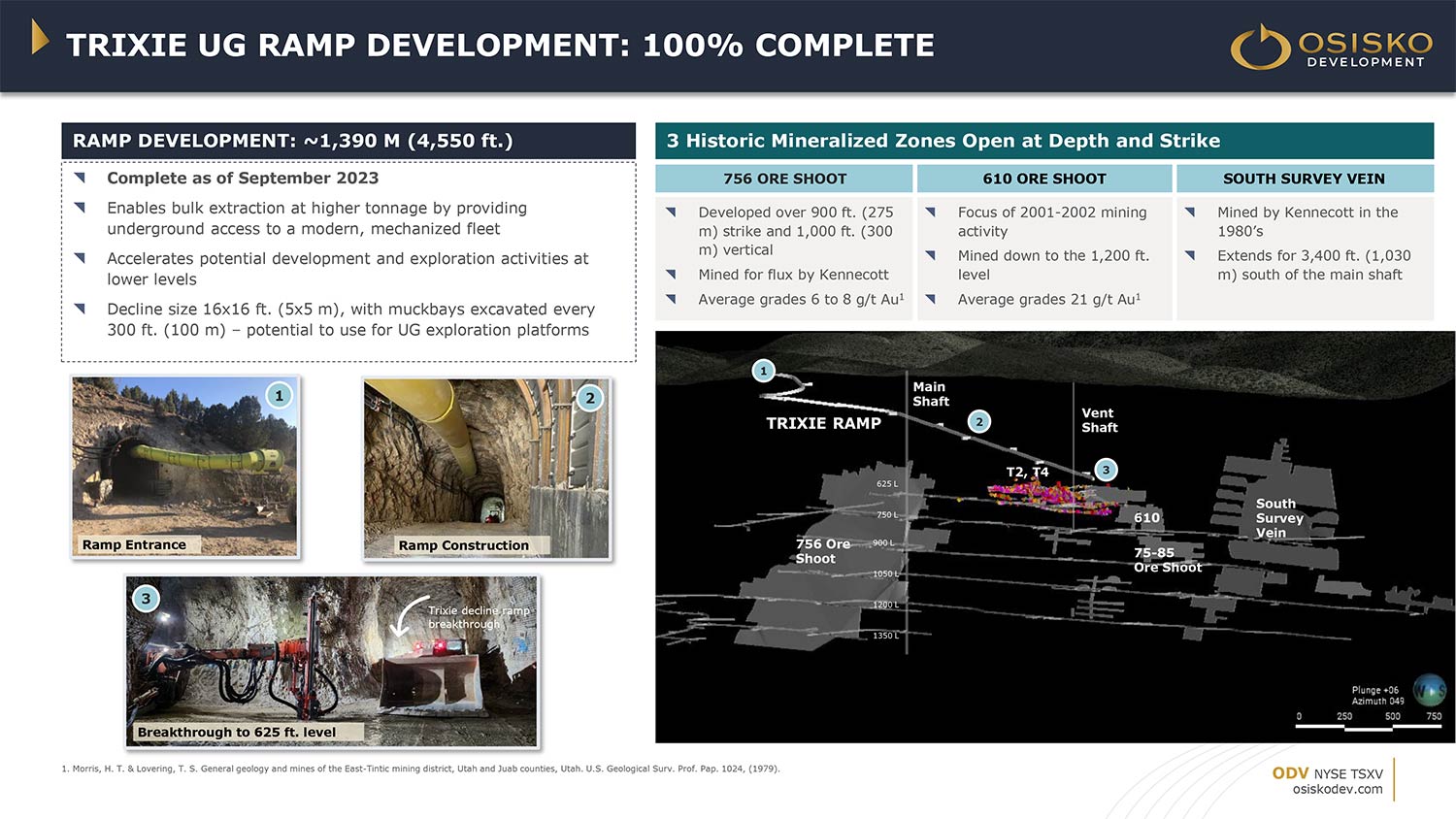

The company has already completed over 6,000 meters of underground drilling across 73 diamond holes at the Trixie deposit, feeding into a 2024 Mineral Resource Estimate outlining 150,000 ounces of gold in the Measured & Indicated category (245 kt @ 19.11 g/t Au) and 51,000 ounces in the Inferred category (202 kt @ 7.80 g/t).

With the Trixie ramp fully developed, Osisko is well-positioned to continue vectoring toward high-grade gold zones while also expanding its search for the district’s potential porphyry source.

Recent Phase II drilling at the Big Hill West and Zuma targets, along with historic mine data, is helping refine exploration vectors across the Tintic Project. This work may lead to new targets for potential mineralized porphyry sources and large, yet undiscovered, polymetallic carbonate replacement deposits.

Meanwhile, Osisko is advancing a small-scale heap leach operation reprocessing historic stockpiles and tailings which produced gold in Q2 2025 and is anticipated continue throughout 2025.

That gives ODV a rare combination of near-term cash flow potential and large-scale blue sky upside in one of the world’s most mining-friendly jurisdictions. In fact, Utah was recently ranked as the top global mining jurisdiction by the Fraser Institute — adding yet another layer of appeal to this under-the-radar US-based asset.

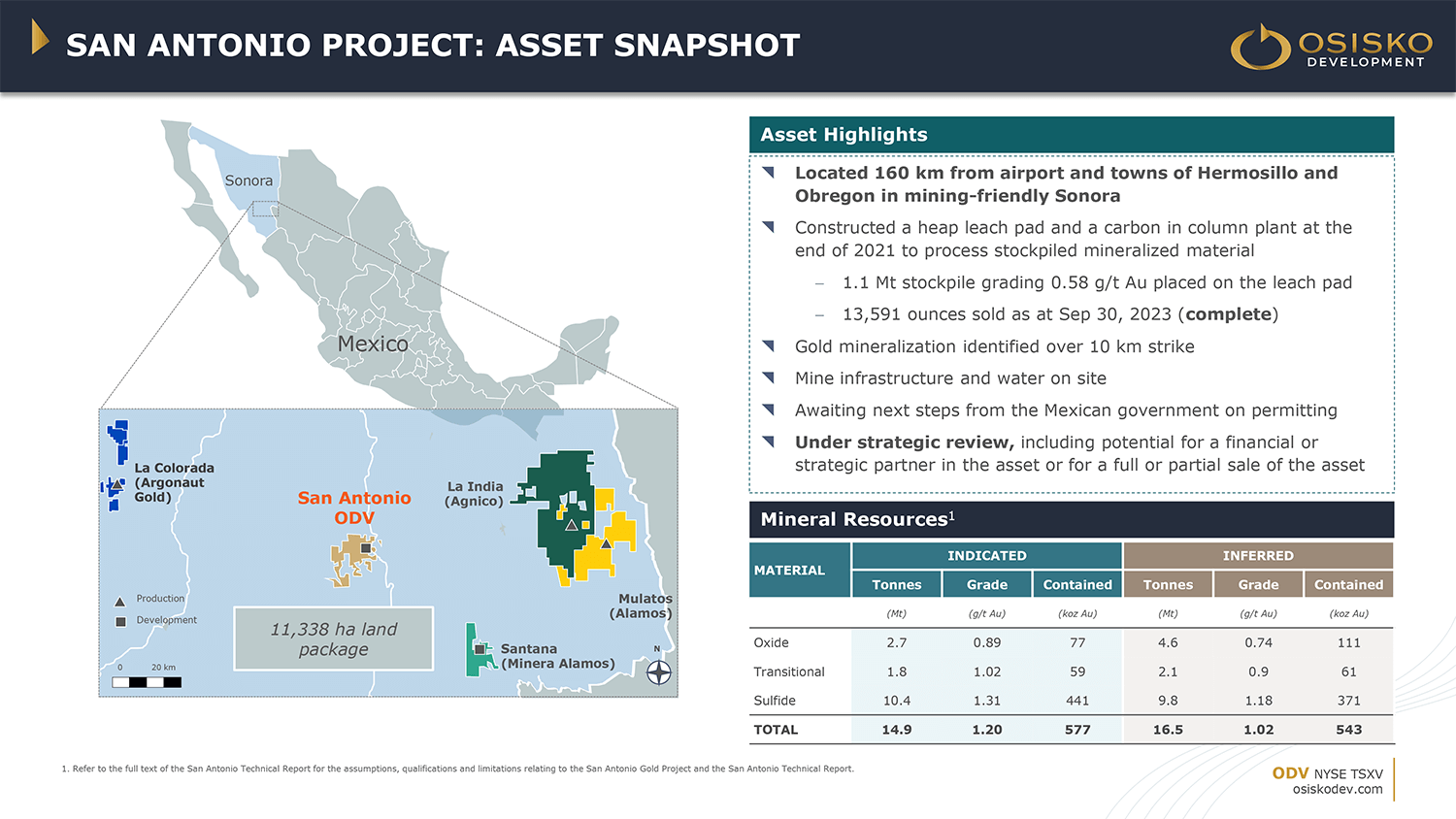

San Antonio Gold-Silver-Copper Project: Sonora, Mexico

Osisko Development’s 100%-owned San Antonio Project is a past-producing gold-copper asset located in Sonora — one of Mexico’s most prominent and mining-friendly states.

The project remains in care and maintenance pending the re-submission of key permit applications, which are expected in the foreseeable future. Recent signs of progress on open-pit permitting in Mexico have sparked renewed optimism for advancing the project toward development.

San Antonio previously generated over 13,000 ounces of gold from stockpile processing via heap leach and carbon-in-column methods between 2022 and 2023. While that initial phase is now complete, the site holds far greater potential.

In June 2022, Osisko announced an initial open-pit Mineral Resource Estimate covering five deposits along a 2.8-km-long strike: Sapuchi, Golfo de Oro, California, Calvario, and High Life. Those zones are hosted within hydrothermal breccia bodies — the primary mineralization control identified to date.

ODV continues to assess strategic options for the asset while preparing for future exploration and drilling to verify historical data and expand the resource.

With favorable geology, supportive infrastructure, and gold-copper upside in a proven district, San Antonio remains a valuable piece of Osisko’s broader growth pipeline.

Exclusive Interview with Osisko Development Corp.

CEO Mr. Sean Roosen

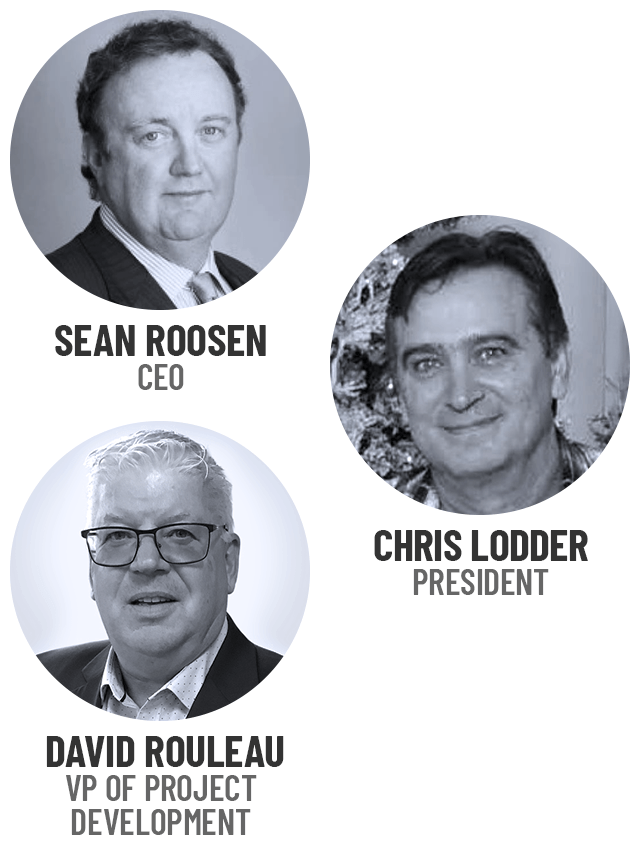

As promised, our own Gerardo Del Real of Resource Stock Digest and Junior Resource Monthly recently sat down with Osisko Development CEO Sean Roosen — a 30-year industry veteran best known for founding Osisko Mining and Osisko Gold Royalties and for leading the discovery and development of the Canadian Malartic Mine, one of Canada’s largest gold producers.

Joining him at the helm is Chris Lodder, president, a seasoned exploration geologist credited with more than 34 million ounces of gold discoveries globally, and David Rouleau, vice president of project development, who brings over three decades of engineering and operations experience across multiple mine builds in North America.

You can learn more about the entire Osisko Development team by clicking here.

Now, without further ado, please enjoy our exclusive interview with Osisko Development CEO Sean Roosen.

Gerardo Del Real: This is Gerardo Del Real. Joining me today is the CEO of Osisko Development Corp. (NYSE: ODV)(TSX-V: ODV) — Mr. Sean Roosen. Sean, it's great to have you on. How are you today?

Sean Roosen: I'm excellent, Gerardo. As we were talking before the show, it's a very good time to be building gold mines.

Gerardo Del Real: Well, let's talk about it. I had the privilege of interviewing Mr. Rick Rule a couple of weeks ago, and he was touting his phenomenal Natural Resources Symposium.

Sean Roosen: Yes.

Gerardo Del Real: And he talked about the phenomenal lineup, and he talked about having people there — presenting and sponsoring — that have been in the belly of the beast.

And look, you’ve built multi-billion-dollar companies in bear markets, in solid markets, in really good markets. But I don't think — well, it's not that I don't think, I know — just because we're at historic highs here, or near them, you haven’t had a market like this to really cook and to really use your skill set.

So when I look at Osisko Development, and I look at the basic market cap of around C$900 million — and how fertile the environment is — and then I look at the background of you and the team, it makes me excited to talk with you and get your thoughts here on the gold space.

Let's start there. How are you feeling about gold? It’s hard not to feel good — but what are your thoughts?

Sean Roosen: Listen, we've all been waiting for gold to sort of break loose out of the trading range around the US$1,500 to $2,200 window that it was stuck in for quite some time. We're here now — we've been well above US$3,000 an ounce for an awfully long time.

That's US$100 a gram or better. It's 31 grams in a troy ounce. So US$100-gram gold makes a one-gram deposit US$100-a-tonne rock. This is 3.62-gram per tonne rock we're trying to do here. So this is US$360 rock that we're dealing with, which is a pleasure for me because I'm used to working with US$50 rock.

Gerardo Del Real: Rick does an amazing job highlighting how we can get excited about where gold is now — and that's great. But if you look at historical ownership of the gold price, we're really near lows relative to the S&P and the major indices.

And then, he talked about how you would have to have a factor of ownership — many multiples of today's percentage — in order to get to a true back-to-the-mean as it relates to the broader indices here in the US.

So how do you feel about the potential runway? Do you need US$4,000 or US$5,000 gold to make 3.6 gram-per-tonne gold rock work?

Sean Roosen: Well, we don't — but we'll sure take it. Our Cariboo project, we just put out an updated Feasibility Study, and our cash costs — the all-in sustaining costs — are about US$1,150 an ounce. In today's market, we'd be making US$2,000 an ounce in gross margin, which is more than 300% our base cost. So there are not many businesses that can say something like that.

And the greater theme of gold — the devaluation of the US dollar — seems like it has to happen. If you want to deal with the US$31 trillion deficit and you want to get the economy in the US rolling again, the strong dollar won't let that happen. So I think we're more in a US dollar devaluation market, as per se, an increasing gold market. But we've seen gold do its job the last 20 years.

I started out as an underground miner in 1981 so I've been at this for a while. I'm a technical guy so I've been running mines and doing that kind of stuff my whole life. This is the best I've seen for gold miners ever. That said, we haven't seen a lot of new, big projects come online. We're seeing the big companies making a huge amount of money.

We built Canadian Malartic, which is Canada's largest gold mine — the ninth largest gold mine in the world — in 2008-09 when the world was ending. We raised C$900 million in February of 2009 to go build that mine because nobody else wanted to finance it.

That mine has been producing ever since, and now Agnico Eagle owns it. We sold it for C$4.1 billion in 2014 and then created a royalty company out of that with a spinco, which is now worth C$6.5 billion or US$5 billion. So to your point, we've been through the hard times and we've thrived in that stress environment when everybody else was sort of throwing their toys out and going home.

And I've been hanging around with Rick Rule for a long time — he may have told you that. And I often sit on his Living Legends panel… which is far better than his Dead Legends panel!

Gerardo Del Real: Listen, we have to talk about the project. It's 100% permitted. You can have your pick of projects, right? Why this project?

It's fully permitted, as I mentioned. It's 100%-owned. You talked about the margin and you talked about the leverage there. Can you speak to what it is about this specific project that made you say, yeah, I'll dedicate my attention and my skill set and my team's focus on this?

Sean Roosen: Well, the reason I'm still in the game is because I've been good at big projects and big companies. Where other people didn't see value, we found Canadian Malartic. We bought that mine for C$88,880. We sold it for C$4.1 billion.

If you broke out Agnico right now, that mine is worth about C$20B to C$22B of their C$100B market cap. So we know what big assets look like, and we know the power of those assets.

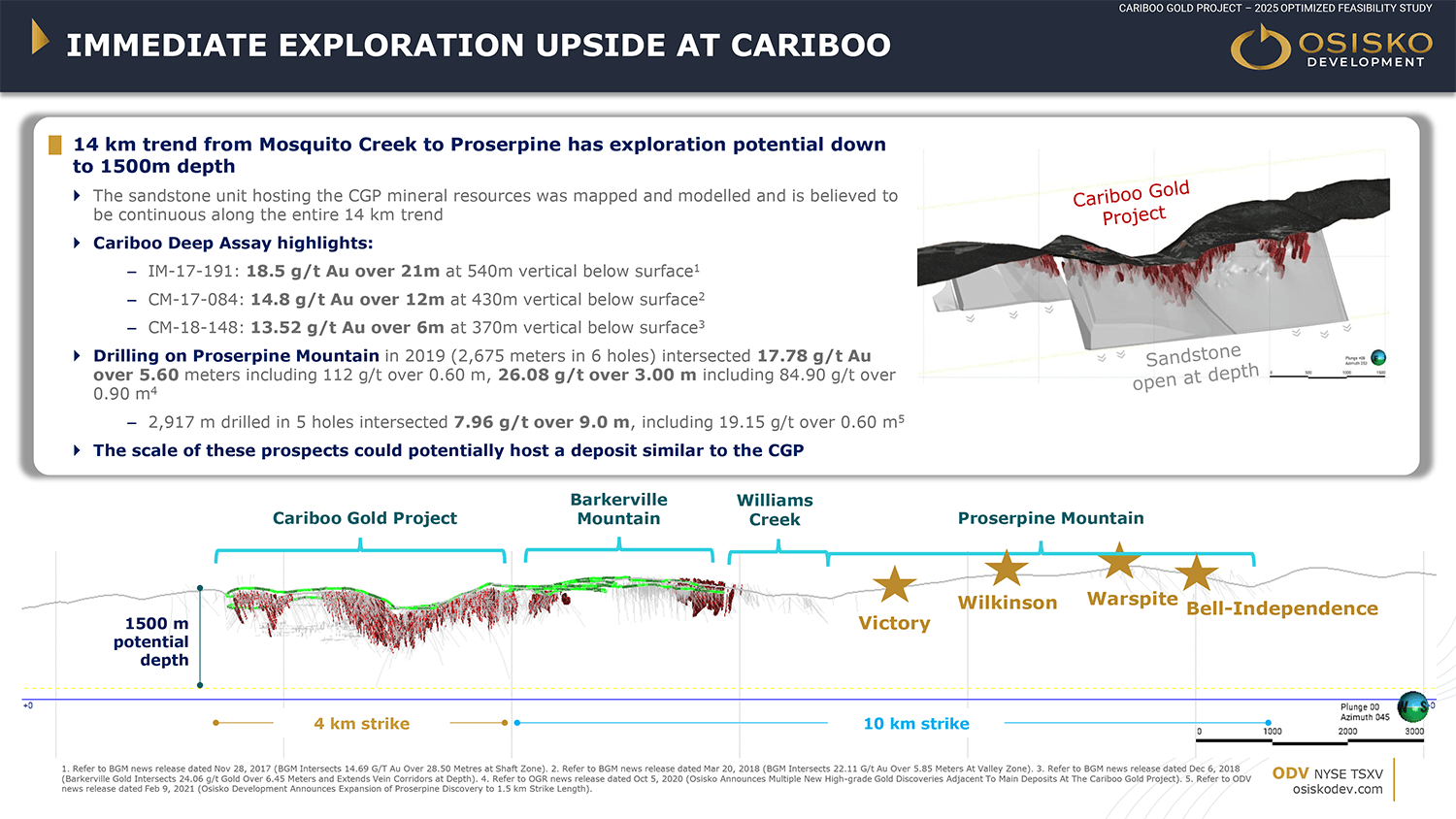

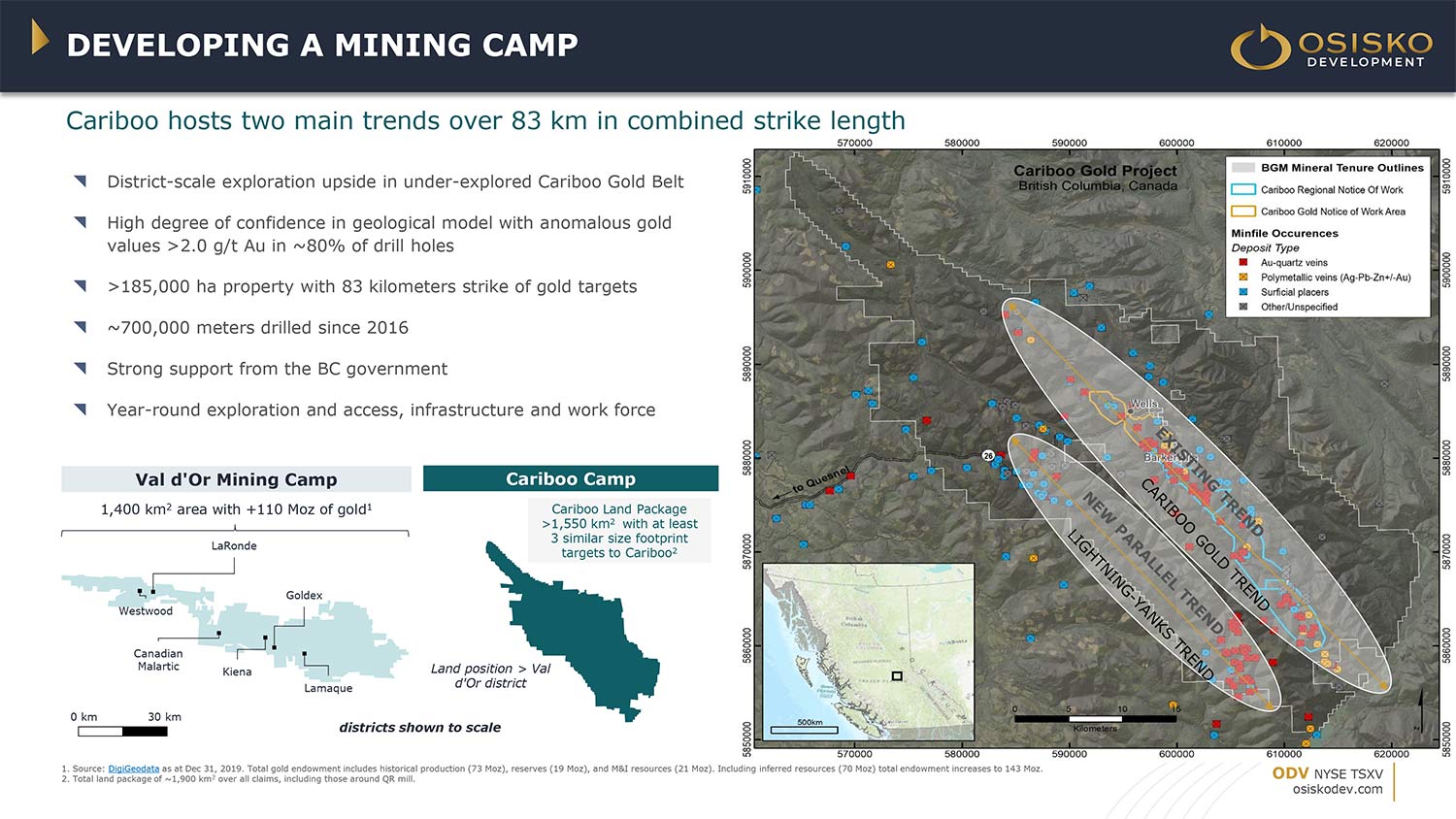

We focus mostly on trying to identify things that we think can be exponentially larger than everything else. Cariboo is one of those things. This is 500,000 acres — about 50 miles of total mineralized trend. The Carlin trend is 50 miles.

Gerardo Del Real: Right.

Sean Roosen: This is two parallel trends. We went in there looking for the next big project that would be Osisko-size. We have a program internally — our strategy is called SUDS, which stands for “shut up and drill, stupid!

Gerardo Del Real: I love it!

Sean Roosen: But for us, we need something big. That's what we're known for, and that's what shareholders will finance with us. This is a big project. The starter project here is 200,000 ounces a year at cash costs under US$1,000 an ounce, all-in sustaining costs of around US$1,157 per ounce.

We have 2 million ounces in the reserve category right now. We have another 1.61 million ounces of Measured & Indicated and yet another 1.8 million ounces of Inferred. So our next extension to grow this thing from 200,000 ounces a year to 400,000 to 500,000 ounces is already within that category of Measured, Indicated, and Inferred. We need to be drilling enough to convert those ounces.

But the good news is with the 2 million ounces and this mine build that we put out, we have about a US$650 million CapEx on this. So for the size of the price for what we're doing here, the ratios are very good. The repay on this thing is about 1.6 years. If we were in production right now, we'd be making about C$450 million of free cash flow a year from this mine — and that's without the expansion capability.

Now, we've sized this thing. Originally, we put out a PEA study in 2022 at 8,000 tonnes per day. But because of the permitting restrictions in Canada, we only permitted for 5,000 tonnes so that we would stay within the boundaries of the provincial permitting process. But we're going to apply for an expansion process as soon as it's practical. But we think as this thing builds, we’ll end up with three to five of these things up and down the belt.

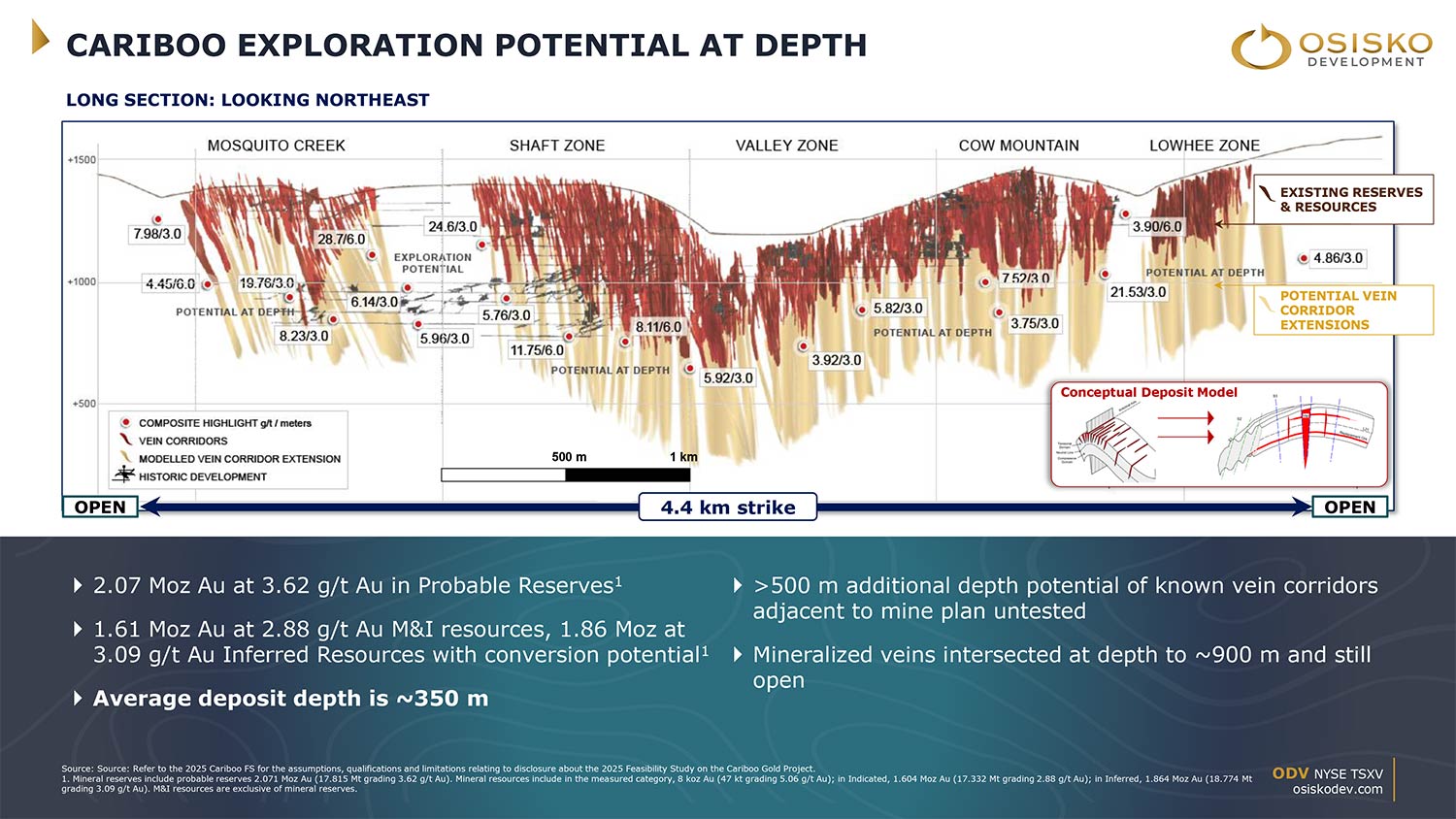

We've drilled this thing down to 1,000 meters but we didn’t do enough drilling down to that depth to put a resource on it. We’ve put the resource down only to a depth of 350 meters. So we’ve been averaging about 15,000 ounces per vertical meter.

This is a rare beast. It’s a sediment-hosted vein system. Some of the things that are like that are Muruntau, which is the largest gold mine in the world. So these aren’t particularly traditional gold deposits that we see in Canada — that are typically the Archaean Greenstone belts that I’m used to. And so this one’s a bit off the charts for what we would do but it only exists in this environment in B.C. in these younger rocks. It’s in Jurassic-age rocks. So this is a pretty exciting play.

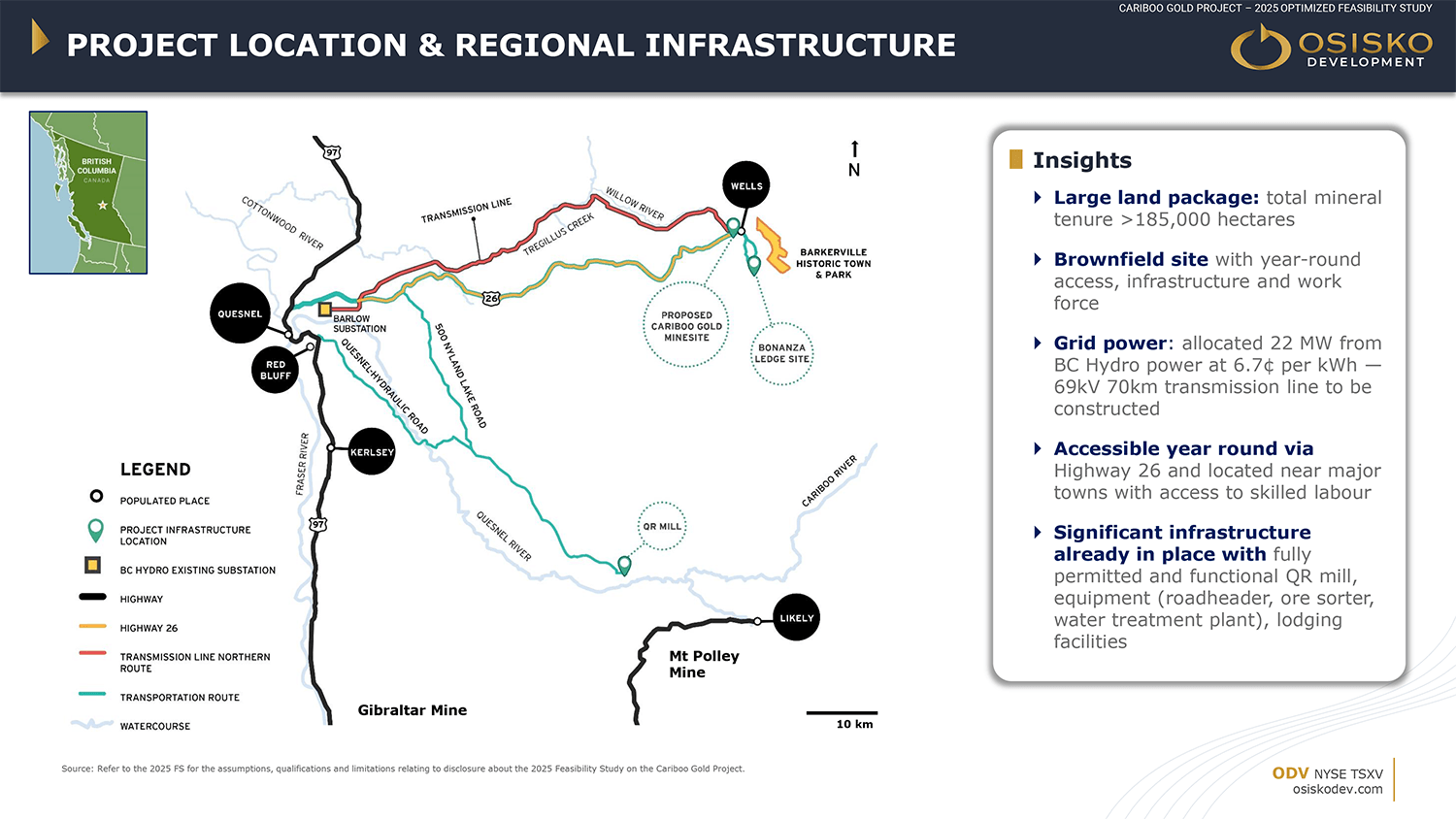

We were the first ones to actually figure out the geology. It’s been mined there since 1858. It’s a brownfields mine site. We can order pizza and McDonald’s to the mine site, and we could be at the Tim Hortons drive-through — which is important for Canadians — in about 45 minutes.

Gerardo Del Real: I love that. Listen, you mentioned your ability to monetize assets to unlock value, and a big part of that is limiting dilution. You have a project financing decision here to make, likely in the second half of this year. How do you approach that, again, given the background, given the network, given your access to capital.

Sean Roosen: We have a couple of analog companies that we'd like you to look at: G-Mining Ventures — they built about a 170,000-ounce-a-year mine in Brazil, and then they have their second project that’s going to be another similar-sized asset in Guyana. And they’re at about a C$5 billion market cap or around US$3.7 billion.

We have the two mines that we need to get similar to where they are within the same site. So we have the reserves in here, and then we have the Measured, Indicated, and the Inferred here. And by converting those, we duplicate basically what they had to do in two different countries — we can do it in one spot.

If you look at just the 200,000-ounce-a-year producer, we would have similar production to something like Wesdome — but again, only one mine site to manage and a significant amount of upside. With the at-depth potential, we have 10 km that we've drilled on to the extension of the strike.

That’s on 4.4 km of strike length — about three miles — and then we have roughly another seven miles on strike that we've drilled on. We know it's there but we didn’t do enough detailed drilling to define it. And we've averaged about 1.2 million ounces of overall resource for every kilometer that we've drilled over that 4.4 km.

The next plan is that we have the main 2 million ounces. The Measured, Indicated, and Inferred that’s in and around that is the next plan. The at-depth target is just to keep extending those vein corridors. At depth, this is a neurogenic system — very predictable, very knowable. And then, we have the on-strike upside.

This is a project that I don't think I'm going to see the close of. I think my grandkids may be working on this one. This is a big project — and this is what we do. We've had the context. I ran the royalty company for 10 years so I pretty much got to look at every project in the world through the royalty business.

And my job — my think tank and my brain trust of Chris Lodder, Ruben Padilla, Terry Harbort, all of the Osisko guys — we've all worked internationally. I was in Africa for 13 years. I've worked around Central Asia for 18 years. We know which one of these projects is better than the other. We have context and we can measure against them.

We've chosen this one as the next big thing for my team. And it’s the reason that I'm not at the dock driving my boat around. You can only do that so much. It gets a little boring after a while.

Gerardo Del Real: I hear you.

Sean Roosen: And if you've seen my golf game, you know why I stick to this…

Gerardo Del Real: No, look, it is hard to argue with the boat — but it's also hard to argue with not taking something like this and running with it.

Sean Roosen: Yeah, this is an exciting project. I mean, most people would be lucky to have one of these in their lifetime. This is kind of like the fourth one for me. We've been very fortunate — and there's often people who will say it's far better to be lucky than to be good.

Gerardo Del Real: Absolutely!

Sean Roosen: My analogy on that is nobody ever scored the winning goal sitting in the stands. You have to be on the pitch.

Gerardo Del Real: Absolutely.

Sean Roosen: So we skate our shift. We work hard. We're 100-hour-a-week kind of guys. The management team — between myself, Bob Wares, and John Burzynski who founded Osisko back in the day — has been together for years.

We sold Windfall Lake, which was under Osisko Mining, to Gold Fields last year for C$2.1 billion. They've got Osisko Metals, which has the big Gaspé Copper deposit on the go. So we're still super active on big deposits. And normally, these things take between 10 to 15 years. We’ve permitted this mine; the other aspect of this mine is that we have the permits.

Gerardo Del Real: Yes.

Sean Roosen: There are only two shovel-ready mine projects in Canada right now that are fully permitted for construction and production. One of them is Seabridge, which is a US$6.5 billion CapEx. We're a US$650 million CapEx. And this is the project that I think is Canada’s next big gold producer.

We're very much on the target list for acquisitions. If you look at a top-ten list for acquisition targets over the last two years, ODV has always been on that list. We also have a project in Utah called Tintic where we are there to look for a Bingham-style lookalike porphyry.

We're drilling at depth there. We're surrounded by my friend Robert Friedland at Ivanhoe Electric who has the ground to the southwest of us and our friends at Freeport to the south of us. And we're 40 miles from the Bingham smelter.

This camp has 23 previous producers on it that were built by Kennecott. We're hunting elephants there, and we're looking for a big Bingham-style copper porphyry at depth.

The difference with Bingham was that it came to surface. This one may not. But in the meantime, we have five historic gold mines. The highest-grade one on the east flank of the graben was 45 grams per tonne. We've accessed the underground there, and we have a small resource we're working on.

But those five mines are connected up. And the only reason they stopped mining them is because they hit water. Subsequently, that water has been pulled down so all five mines stopped at the 1,300-foot level, which is about 300 to 400 meters. And that exploration at depth hasn’t been done.

We have 18 CRD deposits — silver, lead, zinc deposits — that actually had some manganese in them, which is quite strategic these days. And the gold deposit also has some tellurium in it. So there are some critical minerals in that project.

So stay tuned on that one. It’s an exciting piece of the surface of the earth — and Mr. Friedland and his team are working hard to the southwest of us; the Freeport guys are drilling, and we’re underground there now.

So that’s our second project. But the focus for us is to get the financing in, build Cariboo, get the first 200,000 ounces commissioned, and then focus on scaling this asset up.

My last company, when I sold it in 2014, we were producing 670,000 ounces a year. That’s the destination of the GPS — is to try and round off and head for a 700,000-ounce-a-year company.

Gerardo Del Real: Yeah.

Sean Roosen: So we know what that looks like, and we know how to do it — and we have the team to do it. And I think we have the backing of the financial markets, both through traditional debt and private equity, as well as very good equity partners.

Twenty-four percent of our company is owned by OR Royalty Corporation, and 10% is owned by Condire Investors out of Texas. We have some big kids at the table. The stock has had a nice little boost here lately as we get the risk off the table. But again — shovel-ready, fully permitted mine in Canada and on-grid power.

We're using hydroelectric power from site at US$0.05 a kilowatt, and we're on infrastructure. We also own a mill. We have two mills — we have one at QR and then the one that we bought to install on this site for the Cariboo Gold Project. We purchased an all-new kit that didn’t get installed by Hudbay on their Lalor project.

So we have brand-new equipment still in the box — and we bought it for 9 cents on the dollar four years ago. It’s sitting in Prince George. That solves a little bit of engineering because we already own the built comminution circuit, the crushers, the SAG mills, the ball mills, and all the ancillaries that go with that.

We also have 150 beds onsite up and running. And like I said, we’re 45 minutes from Quesnel, which is a 28,000-person town, and we’re an hour and a half from Prince George, which is 180,000 people. And we're near Mount Polley and Taseko's Gibraltar Mine. So we’re in a mining area.

This has always been a mining camp. We have the historic park there called Barkerville Heritage Site, which is still one of the cooler places to visit. It’s an 1860s mining camp set up with period-dressed actors. They’re about 15 km from us so we still have traditional placer miners in the valley.

This area has produced about 4 million ounces in total — but we’ve done what Osisko does. We go to old brownfields mining camps, redo the geology, introduce the science, and then bring in the appropriate technology.

Like at Canadian Malartic, we built a 55,000-tonne-a-day mill, 120 megawatts of power. We went big on it, and we built Canada’s largest gold mine both by ounces per year and by tonnage per day. That’s what we’re looking to do here — bring that thought pattern and that style of entrepreneurialism to this project.

And I think we're just coming out of the Lassonde Curve. We’ve gone through the bottom. We received the permits last fall. We have a beautiful period right now; with the tariffs in Canada, we have a very willing government to get resource projects done because, as Canadians have learned the lesson, it doesn’t matter how many tariffs you put on a mine, you can’t move it. It’s staying where it is, and those jobs are staying where they are.

We have a new refocused government and good regulators behind us. They gave us this permit in 4 years and 10 months. The industry average is 14 years. We have a lot of things lined up.

We have a great partnership with Lhtako Dene, our First Nations host, as well as Williams Lake. We’re still working with our friends from Xatśūll — but the main host is our Lhtako Dene partners. They’ve been just great.

Gerardo Del Real: I mentioned earlier that you had roughly 220 million shares outstanding fully diluted as of the latest reporting period. You’re trading at about three bucks on the Canadian side of things. You’re roughly around a C$900 million basic market cap. I’m pretty sure you’re going to figure out a way to push that valuation up because I doubt you’re selling it for anything close to C$900 million.

Sean Roosen: Right. I’ll tell you one thing — I’ll sleep better north of C$2 billion.

Gerardo Del Real: I believe that. And the track record speaks for itself.

Sean Roosen: Yes.

Gerardo Del Real: Sean, it's been an absolute pleasure. I want to thank you so much. It's an exciting time. I'm looking forward to doing this again. I know it's a busy second half of the year — and again, I think it's going to be a fun second half of the year for you and the team and shareholders.

Sean Roosen: Yes, we're going to start drilling again. There’s another whole exploration program to be run here so we encourage your shareholders to have a look at this one — ODV on the New York Stock Exchange and ODV on the TSX-V.

And good luck to your investors taking advantage of this gold price. We’re one of the developers that’s de-risked right now so I think we should be in the queue to see some valuation. Obviously, the producers have taken off like a rocket.

Gerardo Del Real: Absolutely.

Sean Roosen: Hopefully, some of that money comes back down-market here, and we’ll be ready to host the party.

Gerardo Del Real: I like it! Exciting times, sir. It’s been an absolute pleasure. Thank you so much.

Sean Roosen: Thanks, Gerardo. Best of luck to all your investors.

Gerardo Del Real: Alright, cheers.

The Osisko Development Opportunity

With a fully permitted, construction-ready flagship gold project in British Columbia, a district-scale copper-gold exploration play in Utah, and a gold-copper development asset in Mexico, Osisko Development Corp. (NYSE: ODV)(TSX-V: ODV) stands out as one of the few junior developers offering near-term production potential and long-term discovery upside — all in mining-friendly jurisdictions.

At the center of this story is the Cariboo Gold Project — a high-margin, feasibility-stage underground asset that’s fully permitted and shovel-ready.

With gold currently trading at all-time highs above US$3,600 an ounce, Cariboo’s strong economics are even more compelling with a post-tax NPV(5%) jumping to C$2.07 billion and IRR to 38% at current spot prices.

The timing really couldn’t be any better as investor interest surges across the precious metals space — particularly in companies with high-potential gold projects in safe, Tier-1 jurisdictions.

Additionally, ODV’s Tintic Gold-Copper Project, Utah, delivers upside on multiple fronts — from porphyry-scale copper-gold potential to high-grade fissure zones at the past-producing Trixie deposit.

And in Sonora — one of Mexico’s most mining-friendly states — Osisko’s San Antonio Gold-Silver-Copper Project offers open-pit development optionality in one of the world’s most prolific mining regions.

You heard directly from Osisko Development CEO Sean Roosen. He says of Cariboo:

“This is a rare beast. It’s a sediment-hosted vein system. Some of the things that are like that are Muruntau, which is the largest gold mine in the world. So these aren’t particularly traditional gold deposits that we see in Canada — that are typically the Archaean Greenstone belts that I’m used to. And so this one’s a bit off the charts for what we would do but it only exists in this environment in B.C. in these younger rocks. It’s in Jurassic-age rocks. So this is a pretty exciting play.”

In other words, Osisko Development is on to something potentially BIG that could define its next chapter here in 2H 2025.

Financially, Osisko is exceptionally well-positioned. As of 31 March 2025, the company held approximately C$77.6 million in cash and cash equivalents. ODV is also very well-structured with ~223 million shares outstanding on a fully-diluted basis.

ODV presently trades at a basic market cap of ~C$900 million with a basic enterprise value of ~C$875 million — significantly below the implied value of its core assets and trading at a current market cap that’s a mere fraction of peer companies Artemis Gold and G-Mining Ventures.

Adding further strength, Osisko recently appointed seasoned mining executive David Rouleau as vice president of project development, bringing over 30 years of operational expertise to the team.

With gold in a sustained uptrend, catalysts forming across the company’s three core assets, and a tightly held valuation, Osisko is primed for a potential re-rating as it advances toward gold producer status in 2H 2025 and beyond.

Now is the opportune time to start taking a closer look at Osisko Development Corp. as the company advances toward gold production and unlocks value across its impressive portfolio.

A great place to start is ODV’s corporate website where you can learn more about the properties, the team, and sign up to receive updates directly from the company’s IR department.

View the most recent Corporate Presentation here.

Also, click here for more of our ongoing coverage of Osisko Development Corp., including additional late-breaking interviews with upper management as developments arise.

Osisko Development Corp. trades on the NYSE under the symbol ODV and on the Toronto Venture Exchange under the symbol ODV.

— Resource Stock Digest Research

Click here to see more from Osisko Development Corp.IMPORTANT DISCLAIMER & DISCLOSURES

Resource Stock Digest, as a publisher, is not a broker, investment advisor, or financial advisor in any jurisdiction.

Please do not rely on the information presented by Resource Stock Digest as personal investment advice.

If you need personal investment advice, kindly reach out to a qualified and registered broker, investment advisor, or financial advisor.

The communications from Resource Stock Digest should not form the basis of your investment decisions. Examples we provide regarding share price increases related to specific companies are based on randomly selected time periods and should not be taken as an indicator or predictor of future stock prices for those companies.

Osisko Development Corp. has sponsored this report.

The information in this newsletter does not constitute an offer to sell or a solicitation of an offer to buy any securities of a corporation or entity, including U.S. Traded Securities or U.S. Quoted Securities, in the United States or to U.S. Persons. Securities may not be offered or sold in the United States except in compliance with the registration requirements of the Securities Act and applicable U.S. state securities laws or pursuant to an exemption therefrom.

Any public offering of securities in the United States may only be made by means of a prospectus containing detailed information about the corporation or entity and its management as well as financial statements. No securities regulatory authority in the United States has either approved or disapproved of the contents of any newsletter. Neither Resource Stock Digest nor any employee of Resource Stock Digest is registered with the United States Securities and Exchange Commission (the “SEC”): as a “broker-dealer” under the Exchange Act, as an “investment adviser” under the Investment Advisers Act of 1940, or in any other capacity. Resource Stock Digest, its owners, directors, and employees are also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

HIGHLY BIASED:

In our role, we aim to highlight specific companies for your further investigation; however, these are not stock recommendations, nor do they constitute an offer or sale of the referenced securities. Resource Stock Digest has received cash compensation from Osisko Development Corp. and is thus extremely biased. It is crucial that you conduct your own research prior to investing. This includes reading the companies' SEDAR and SEC filings, press releases, and risk disclosures. The information contained in our profiles is based on data provided by the companies, extracted from SEDAR and SEC filings, company websites, and other publicly available sources.

Resource Stock Digest, and its owners, directors, employees, and members of their households may own shares of Osisko Development Corp.. Therefore, Resource Stock Digest is extremely biased. Measures are in place such that no shares will be sold during the active awareness campaign.

HIGH RISK:

The securities issued by the companies we feature should be seen as high risk; if you choose to invest, despite these warnings, you may lose your entire investment. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures.

NOT PROFESSIONAL ADVICE:

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Resource Stock Digest, and all partners, members, and affiliates harmless in any event or claim. While Resource Stock Digest strives to provide accurate and reliable information sourced from believed-to-be trustworthy sources, we cannot guarantee the accuracy or reliability of the information. The information provided reflects conditions as they are at the moment of writing and not at any future date. Resource Stock Digest is not obligated to update, correct, or revise the information post-publication.

FORWARD-LOOKING STATEMENTS:

Certain information presented may contain or be considered forward-looking statements. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results or events to differ materially from those anticipated in these statements. There can be no assurance that any such statements will prove to be accurate, and readers should not place undue reliance on such information. Resource Stock Digest does not undertake any obligations to update the information presented or to ensure that such information remains current and accurate.

CAUTIONARY STATEMENTS:

This video may contain forward-looking statements within the meaning of applicable Canadian securities laws. Forward-looking statements relate to future events and conditions, and therefore involve inherent risks and uncertainties beyond the control of Osisko Development. Actual results may differ materially from those currently anticipated in such forward-looking statements. Viewers are cautioned that Osisko Development does not undertake to update any forward-looking statements, other than as required by law. For more detail viewers are urged to consult the disclosure provided under the heading "Risk Factors" in the Company's annual information form for the year ended December 31, 2024, as well as the financial statements and MD&A for the year ended December 31, 2024, which have been filed on SEDAR+ (www.sedarplus.ca) under Osisko Development's issuer profile and on the SEC's EDGAR website (www.sec.gov), for further information regarding the risks and other factors. Information relating to mineral reserves and resources is supported by technical reports prepared in accordance with NI 43-101 and available electronically on SEDAR+, EDGAR, and on the Company’s website at www.osiskodev.com.

Information relating to the Cariboo Gold Project and the 2025 Feasibility Study is supported by the technical report titled "NI 43-101 Technical Report, Feasibility Study for the Cariboo Gold Project, District of Wells, British Columbia, Canada" and dated June 11, 2025 (with an effective date of April 25, 2025) (the "Technical Report"). For readers to fully understand the information in the Technical Report, reference should be made to the full text of the Technical Report in their entirety, including all assumptions, parameters, qualifications, limitations and methods therein. The Technical Report is intended to be read as a whole, and sections should not be read or relied upon out of context. The Technical Report was prepared in accordance with NI 43-101 and is available electronically on SEDAR+ (www.sedarplus.ca) and on EDGAR (www.sec.gov) under Osisko Development's issuer profile and on the Company's website at www.osiskodev.com.