Click here to read important disclaimer & disclosures Click here to see more about PMET Resources

Critical Mineral Powerhouse

TSX: PMET | OTCQX: PMETF | ASX: PMT

North America's New

Critical Mineral Powerhouse

With LITHIUM climbing and CESIUM now confirmed as a globally strategic asset, this Tier-1 Canadian developer is advancing the largest hard rock lithium-cesium system in the Western world

— Shares still around US$3 —

WORLD-CLASS LITHIUM-CESIUM ASSET IN A TIER-1 CANADIAN JURISDICTION

Feasibility Due Q4 2025 — Trading Near US$3 with Major Rerate Potential

Click Here to Read Sponsor Disclosure

Emerging Lithium Leader

with a Strategic Cesium Kicker

PMET Resources Inc. (TSX: PMET)(OTCQX: PMETF)(ASX: PMT) is rapidly emerging as one of North America’s most important next-generation lithium developers and a serious contender in the global race to secure scalable, multi-critical mineral supply.

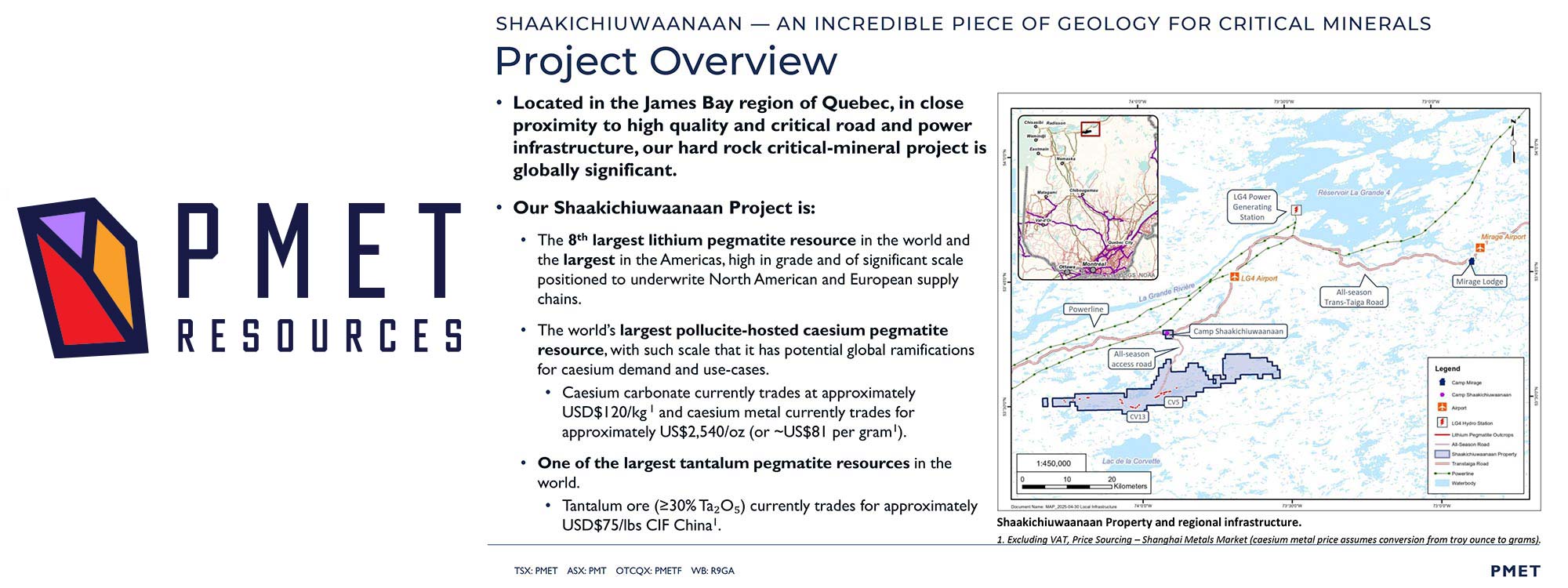

At the center of it all is the company’s flagship Shaakichiuwaanaan Project (formerly “Corvette”) in Quebec’s James Bay region — an ultra-safe Tier-1 mining jurisdiction now attracting billions in mining-sector investment tied to the battery-metals boom.

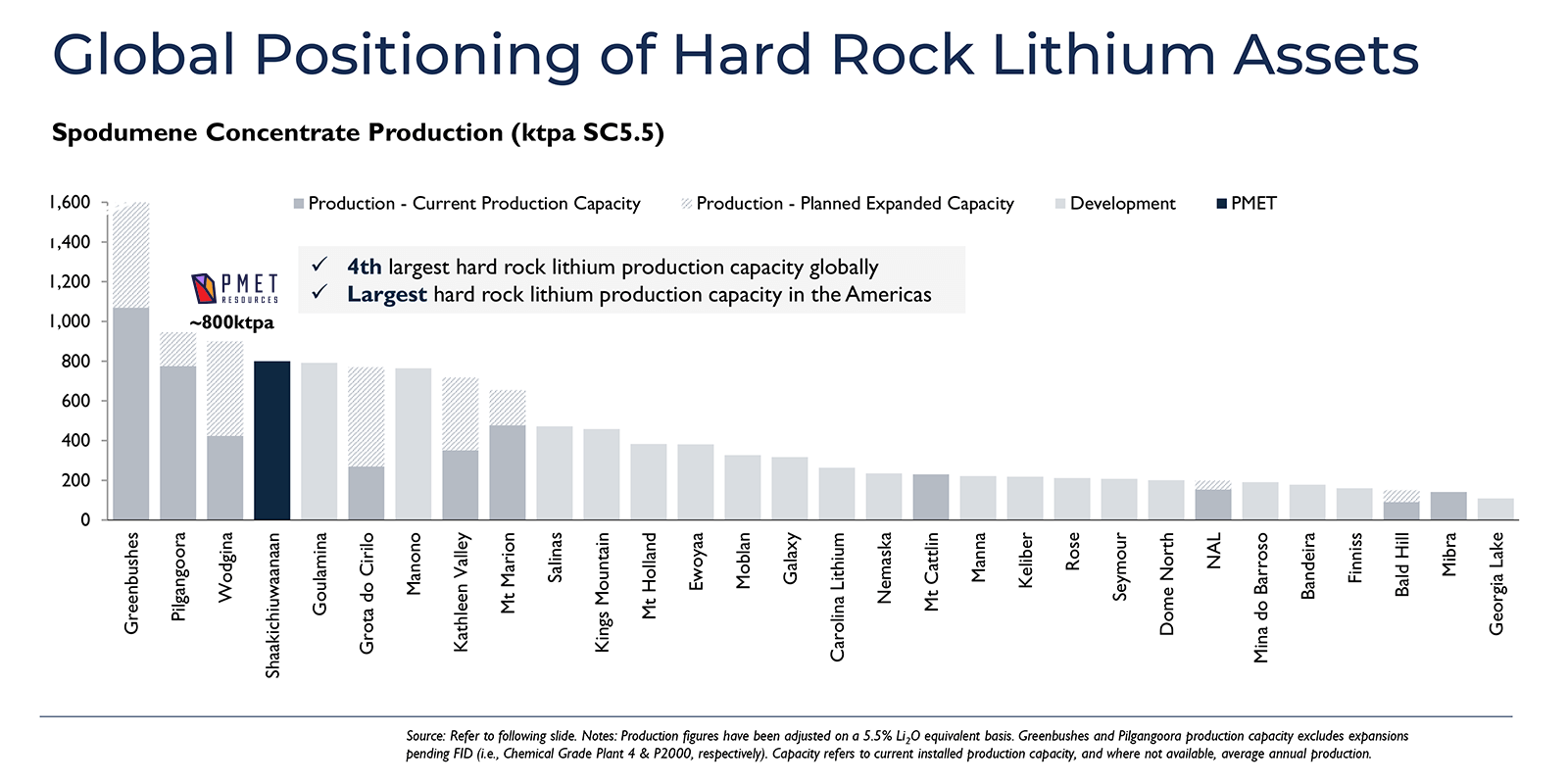

The project has already been confirmed to host the largest lithium pegmatite Indicated Mineral Resource in the Americas and one of the largest globally at an incredible:

108 million tonnes (Mt) at 1.4% lithium oxide (Li2O) Indicated and 33.3 Mt at 1.33% Li2O Inferred.

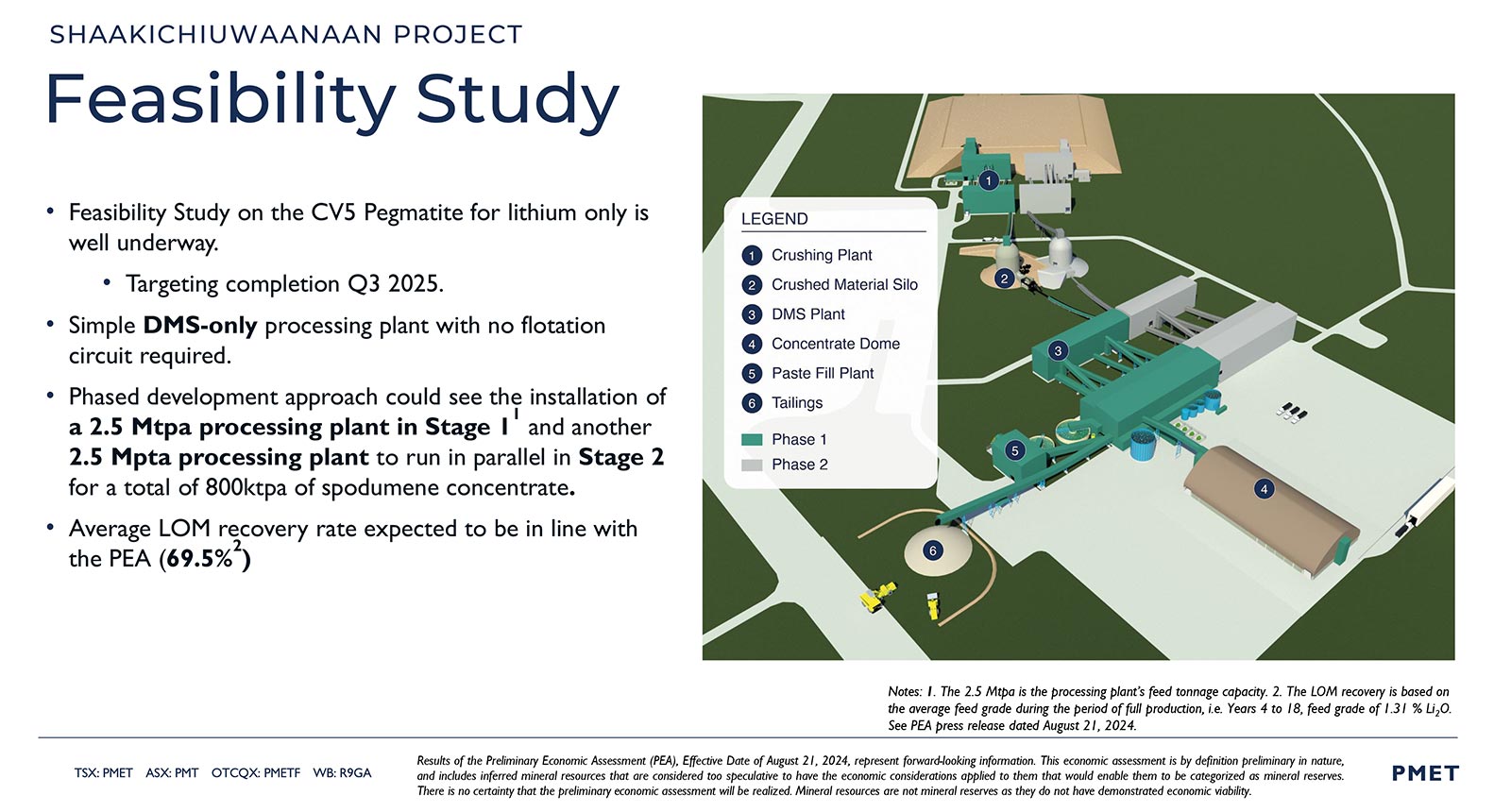

A lithium-only Feasibility Study for the CV5 pegmatite is due in Q3 2025 — a high-impact milestone that’s expected to significantly de-risk the project and mark the transition toward final permitting and construction.

While lithium remains the focus, Shaakichiuwaanaan is far from a one-metal story.

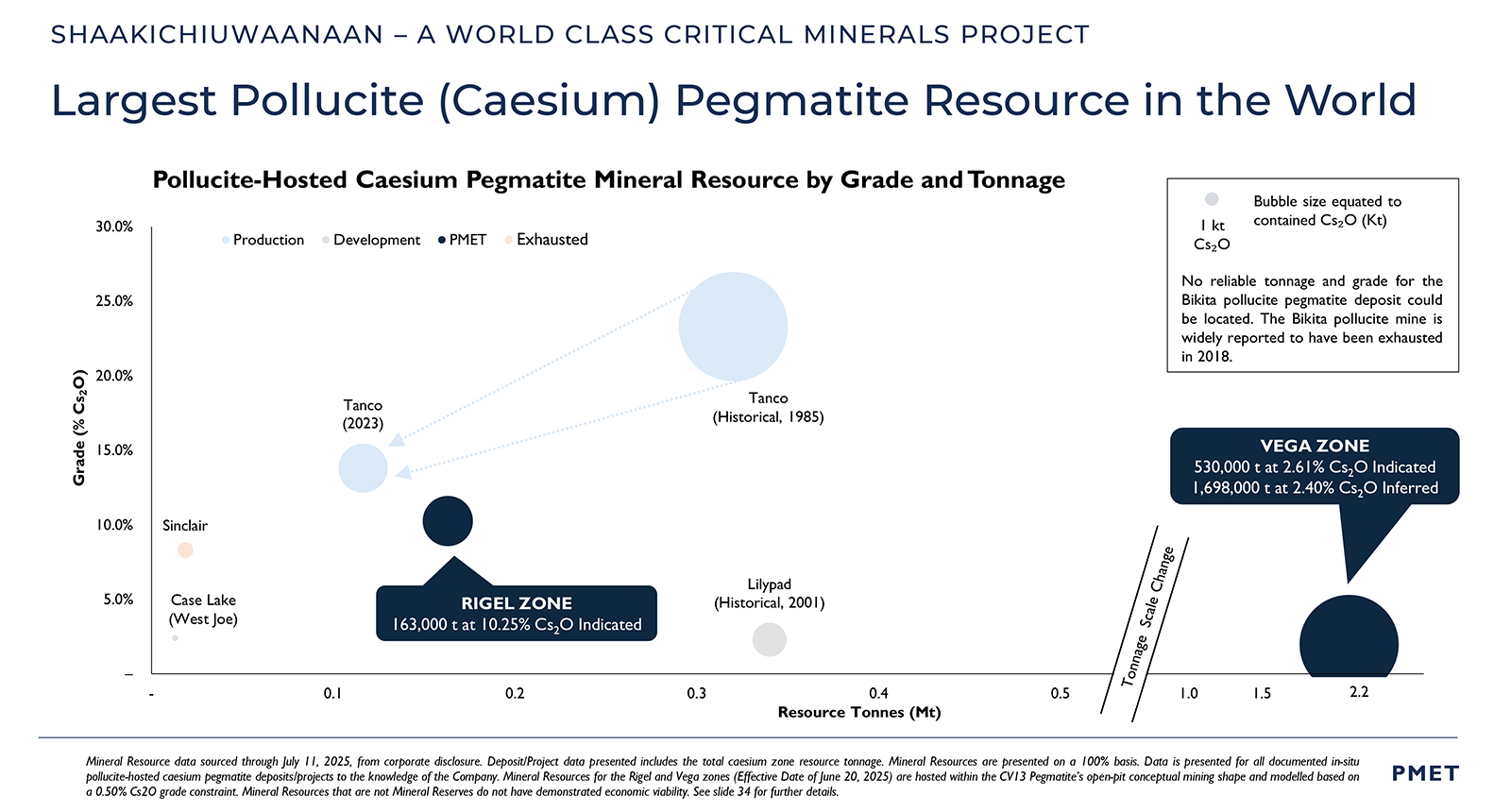

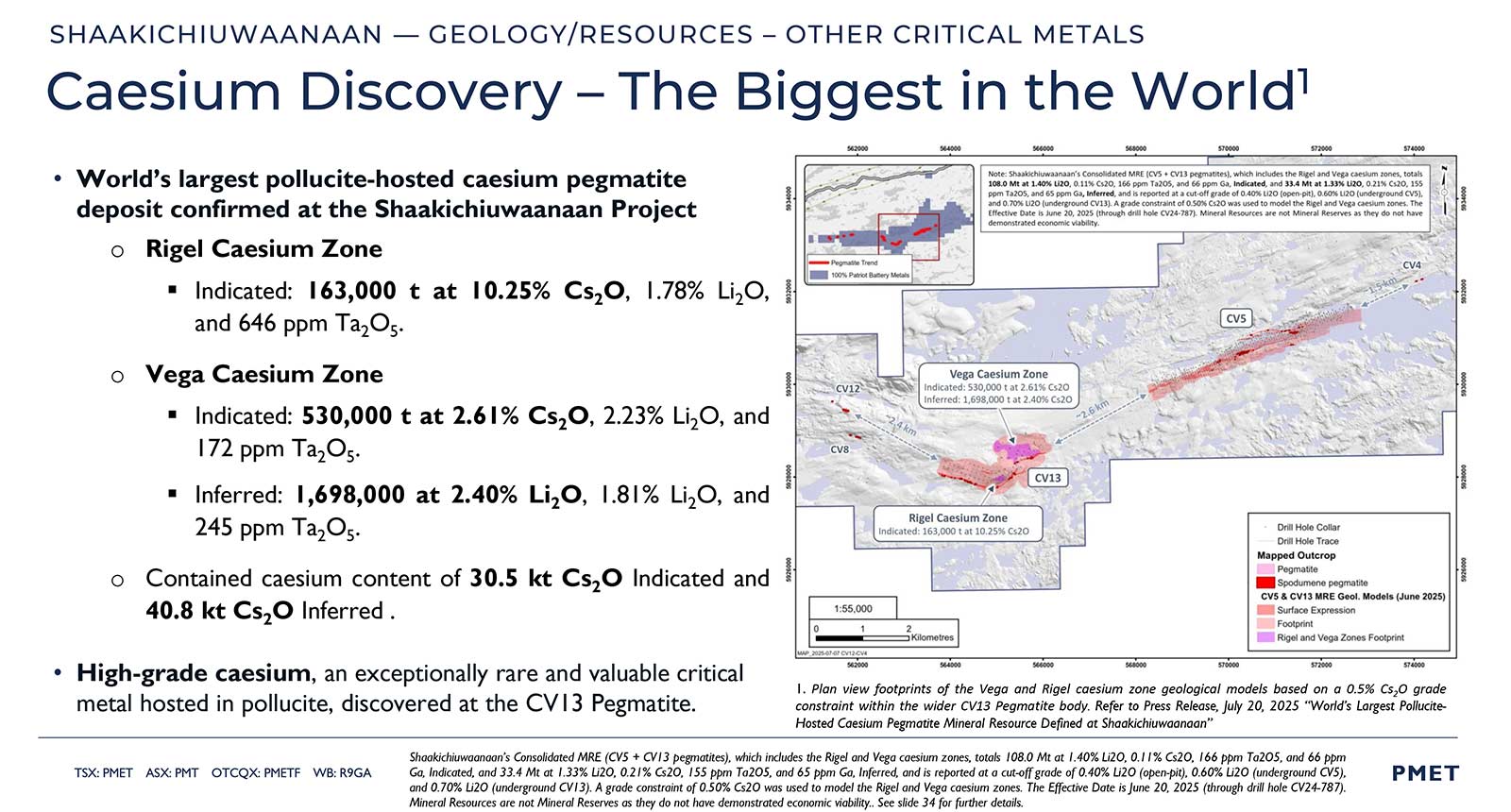

In a major new development, PMET Resources has now confirmed the world’s largest pollucite-hosted cesium resource, both in size and grade, following a newly announced maiden Mineral Resource Estimate (MRE).

The cesium component — a rare, high-value critical mineral used in solar, medical imaging, and defense — is hosted in the Rigel and Vega zones at the CV13 pegmatite and comes in at a staggering:

693,000 tonnes at 4.4% cesium oxide (Cs2O) Indicated and 1,698,000 tonnes at 2.4% Cs2O Inferred.

With cesium carbonate priced around US$120/kg and pure cesium metal fetching over US$2,500/oz, the value-add potential of this critical secondary commodity is just beginning to be understood.

In a market starved for secure supply — and with historic deposits like Tanco, Sinclair, and Bikita depleted or nearing end-of-life — PMET’s newly announced cesium discovery lands at a time of soaring global demand.

Importantly, the cesium is fully embedded within broader lithium and tantalum zones, positioning Shaakichiuwaanaan as a uniquely strategic, multi-metal asset with long-term upside.

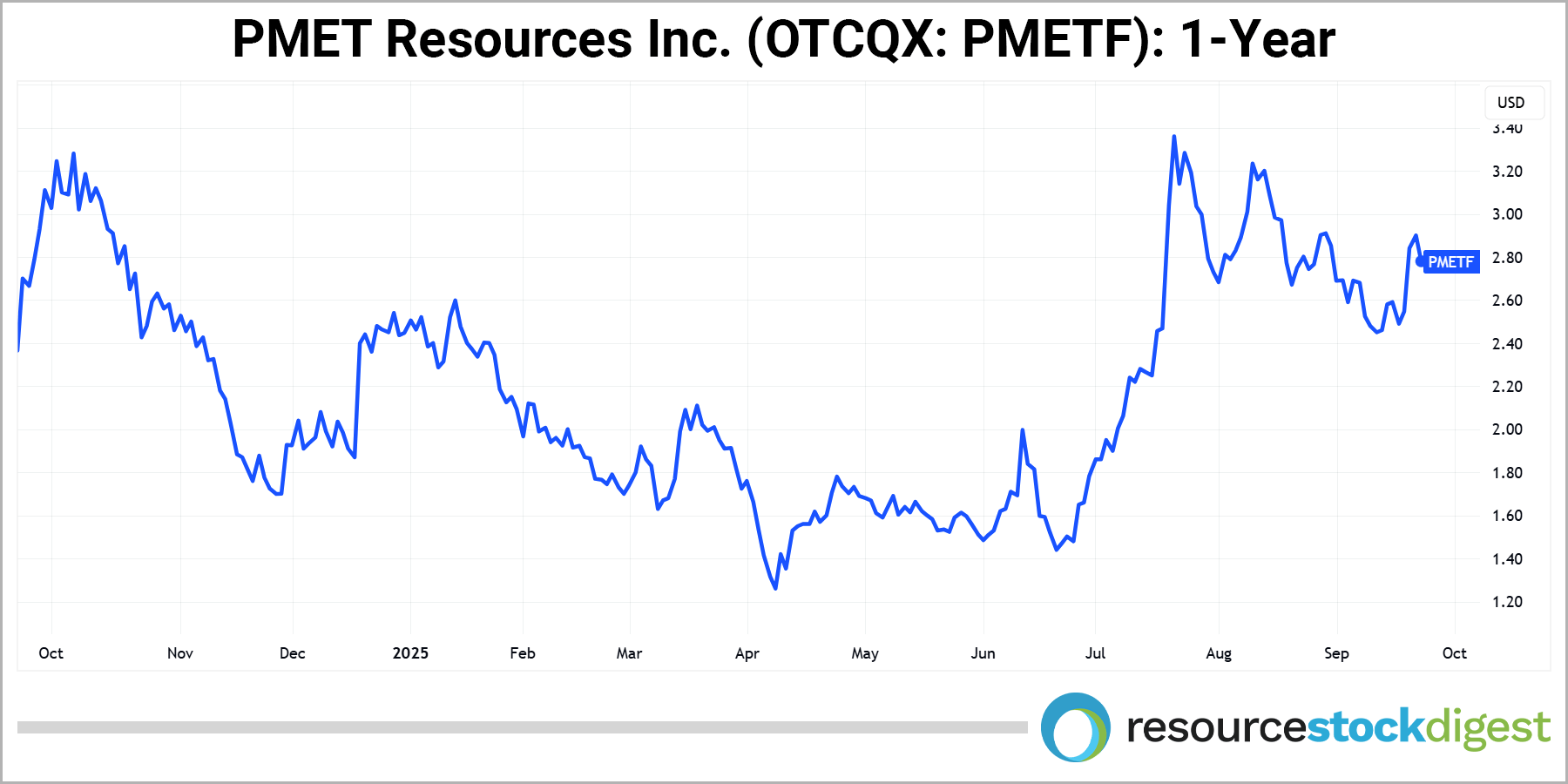

Even with all those advantages, PMET’s shares are still trading relatively undiscovered around US$3 — giving well-timed speculators a compelling entry point ahead of multiple high-impact catalysts over the next 6 to 12 months.

For speculators seeking exposure to critical minerals, North American supply, and electrification trends, the real PMET Resources story is only just beginning to unfold.

Lithium Foundation

Feasibility at CV5 Sets Stage for Rapid Buildout

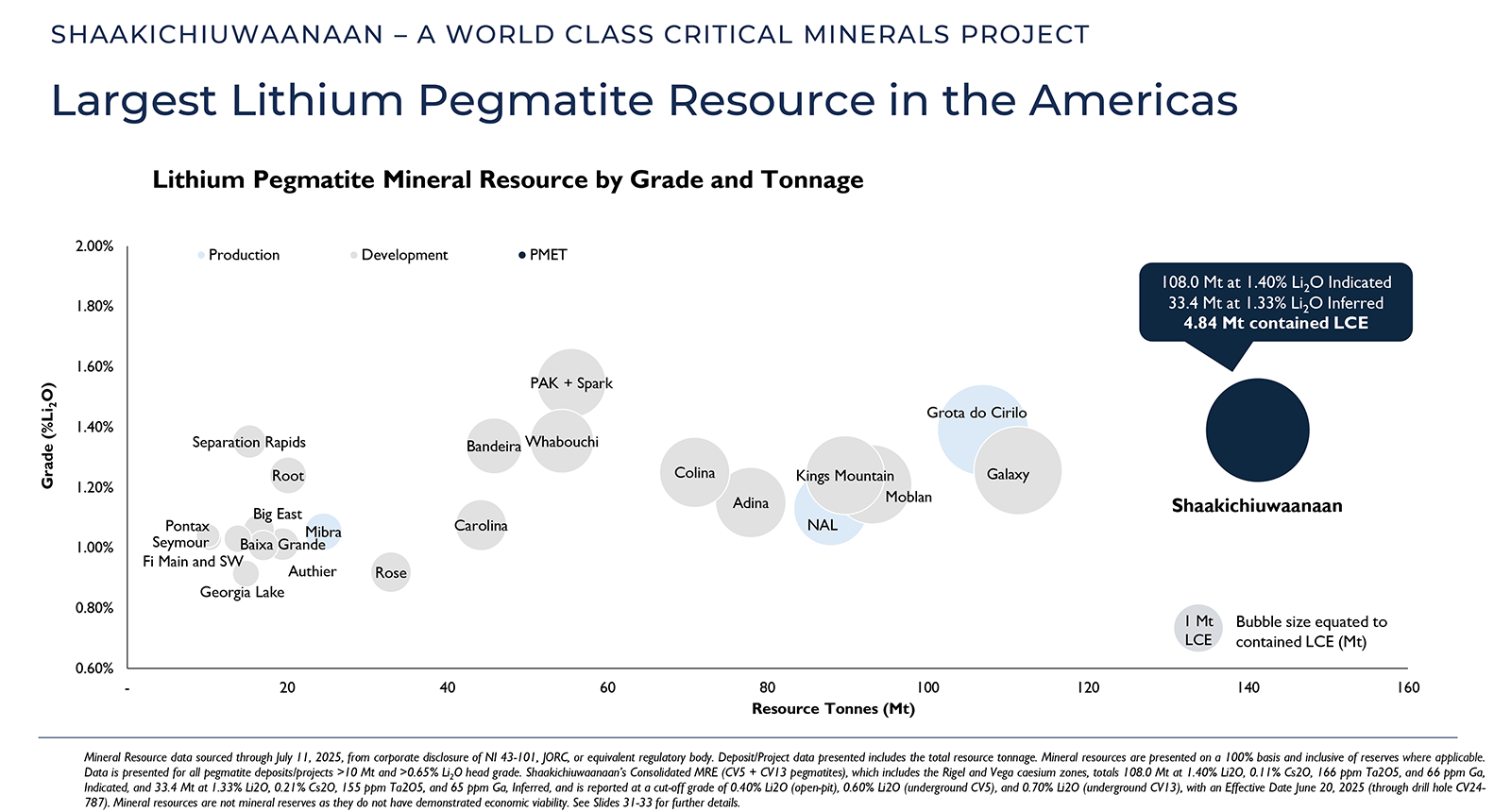

At the core of PMET Resources’ story is CV5 — a long, continuous spodumene-rich pegmatite that now ranks as the largest lithium pegmatite Indicated resource in the Americas.

The most recent Mineral Resource Estimate (Q2 2025) confirms:

- 108 Mt @ 1.4% Li2O Indicated

- 33.3 Mt @ 1.33% Li2O Inferred

- Combined total of 141.3 Mt across the CV5 and CV13 deposits

The Q2 2025 update reflects a substantial 30% increase in Indicated resources at CV5 along with a remarkable 306% increase at nearby CV13 — underscoring strong growth and long-term scalability across the broader Shaakichiuwaanaan system.

The MRE also includes valuable critical metal credits: 166 parts per million (ppm) tantalum oxide (Ta2O5) and 66 ppm gallium (Ga) in the Indicated category.

That combination of scale, grade, continuity, and critical metal content places CV5 among the top-ten polymetallic pegmatite resources globally — firmly establishing Shaakichiuwaanaan as one of the most strategically important critical mineral development assets in the world.

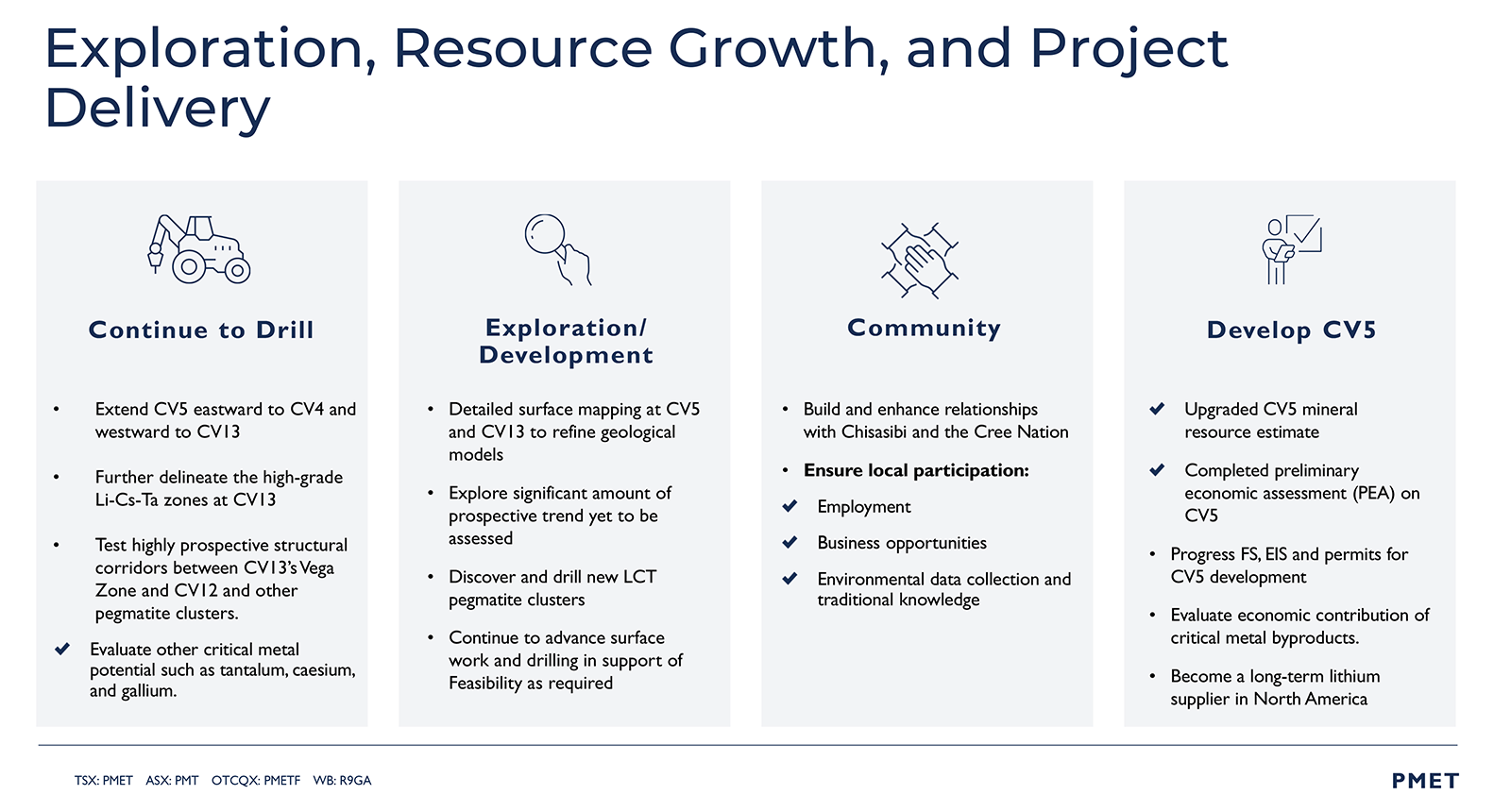

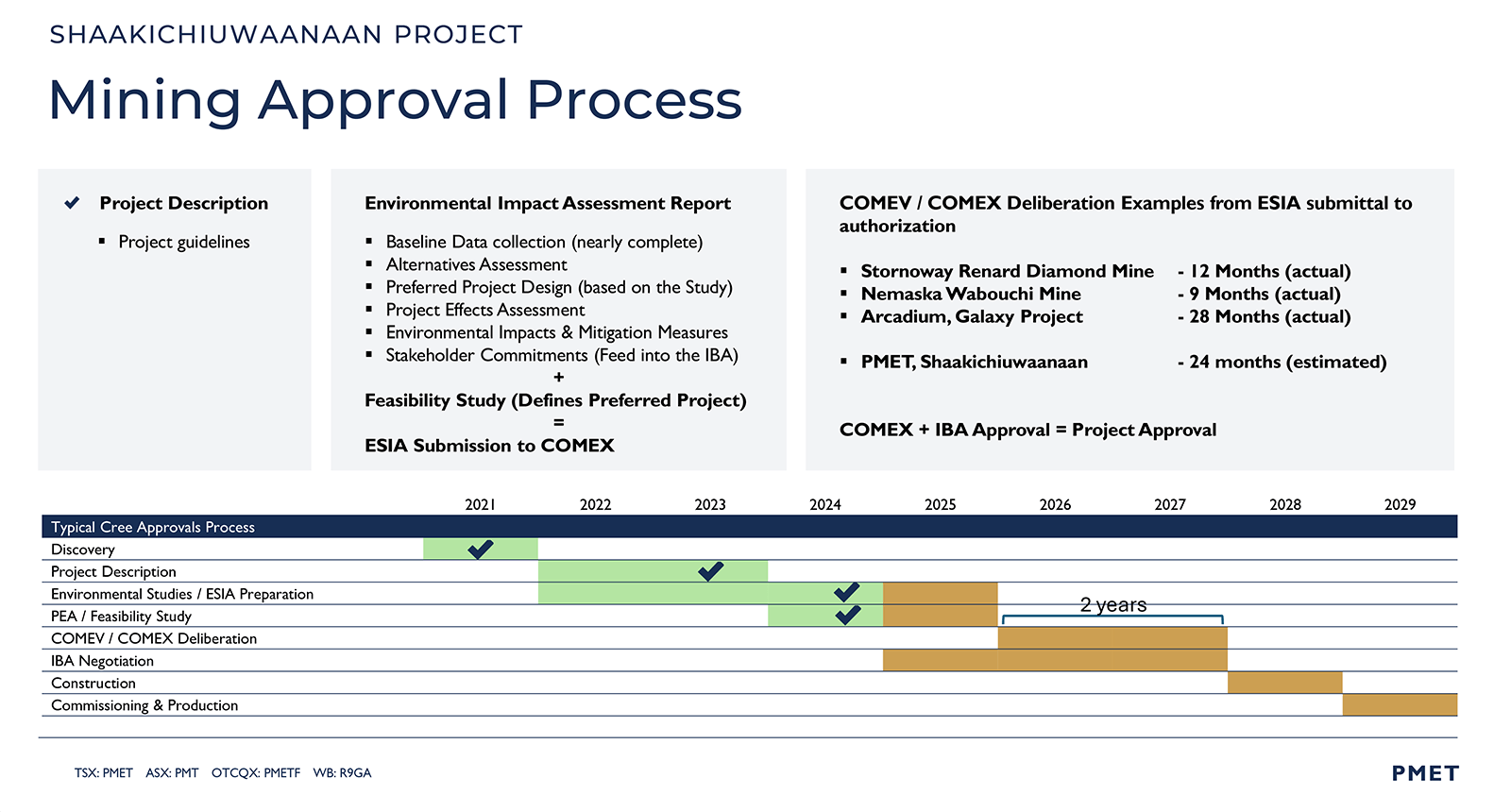

PMET’s current focus is on delivering a lithium-only Feasibility Study at CV5, expected in Q3 2025 — a major near-term milestone and catalyst that will underpin mine permitting, project financing, and the transition to construction.

Crucially, PMET is executing a highly intelligent staged development strategy at the flagship project.

Rather than delay advancement by incorporating satellite zones or byproduct flows into the initial mine plan, the company is prioritizing lithium first — accelerating approvals and sharpening its path to production.

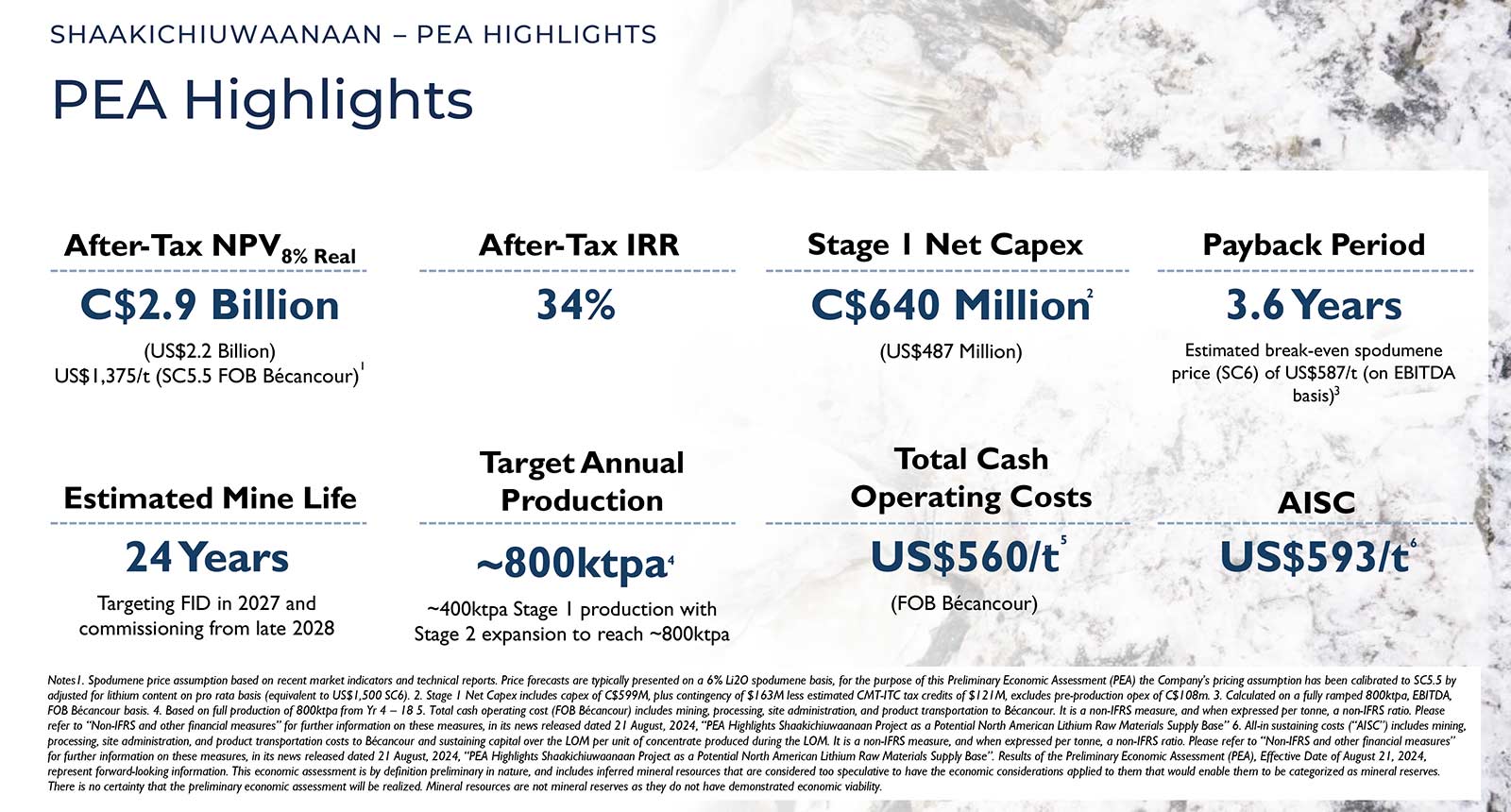

A 2024 Preliminary Economic Assessment (PEA) underscores the strong economics of a staged lithium-only development plan at CV5.

That disciplined focus sets PMET apart. And it matters even more in a world-class jurisdiction like Quebec.

James Bay remains one of the world’s most attractive Tier-1 mining districts, offering stable permitting, strong community partnerships, and exceptional infrastructure.

With established relationships across the Cree Nation, proximity to low-cost hydropower, year-round road access, and a permitting timeline measured in 12 to 24 months, Shaakichiuwaanaan is both strategically positioned and uniquely de-risked for near-term development.

As PMET CEO Ken Brinsden — featured in our exclusive interview just ahead — recently said:

“We’re advancing a large, strategic, high-quality lithium asset in a Tier-1 location — and we’re doing it with speed, clarity, and purpose.”

The lithium is here. The path to build is clear. And PMET Resources is executing with the kind of technical rigor and commercial foresight that continues to draw major players — including Volkswagen — to the table.

Game-Changing Cesium Discovery

A High-Value Critical Mineral with Global Supply Chain Impact

While lithium remains the centerpiece of PMET’s development plan, newly defined cesium zones at CV13 are quickly emerging as a strategic value-add metal with the potential to enhance future project economics and unlock new market opportunities.

The aforementioned Rigel and Vega zones within the CV13 pegmatite now host what is recognized as the largest pollucite-hosted cesium resource in the world — both in grade and scale.

The zones have now been incorporated into an updated Mineral Resource Estimate (MRE) for CV13, further underscoring the scale and multi-metal upside of the system.

CV13 Cesium MRE:

- 693,000 tonnes Indicated at 4.4% Cs2O

- 1,698,000 tonnes Inferred at 2.4% Cs2O

- Contained Cs2O: 71,300 tonnes total Indicated + Inferred

The zone footprints are substantial: ~800m x 250m (Vega) and ~200m x 100m (Rigel) as compared to historical cesium discoveries typically measuring just 40 to 50 meters in length and width.

The cesium mineralization is hosted in pollucite, the ideal carrier for cesium — much like spodumene is for lithium.

Globally, cesium supply is both constrained and vulnerable. Legacy sources like Sinclair (Australia) and Bikita (Zimbabwe) are now depleted, and Canada’s Tanco mine is nearing end-of-life.

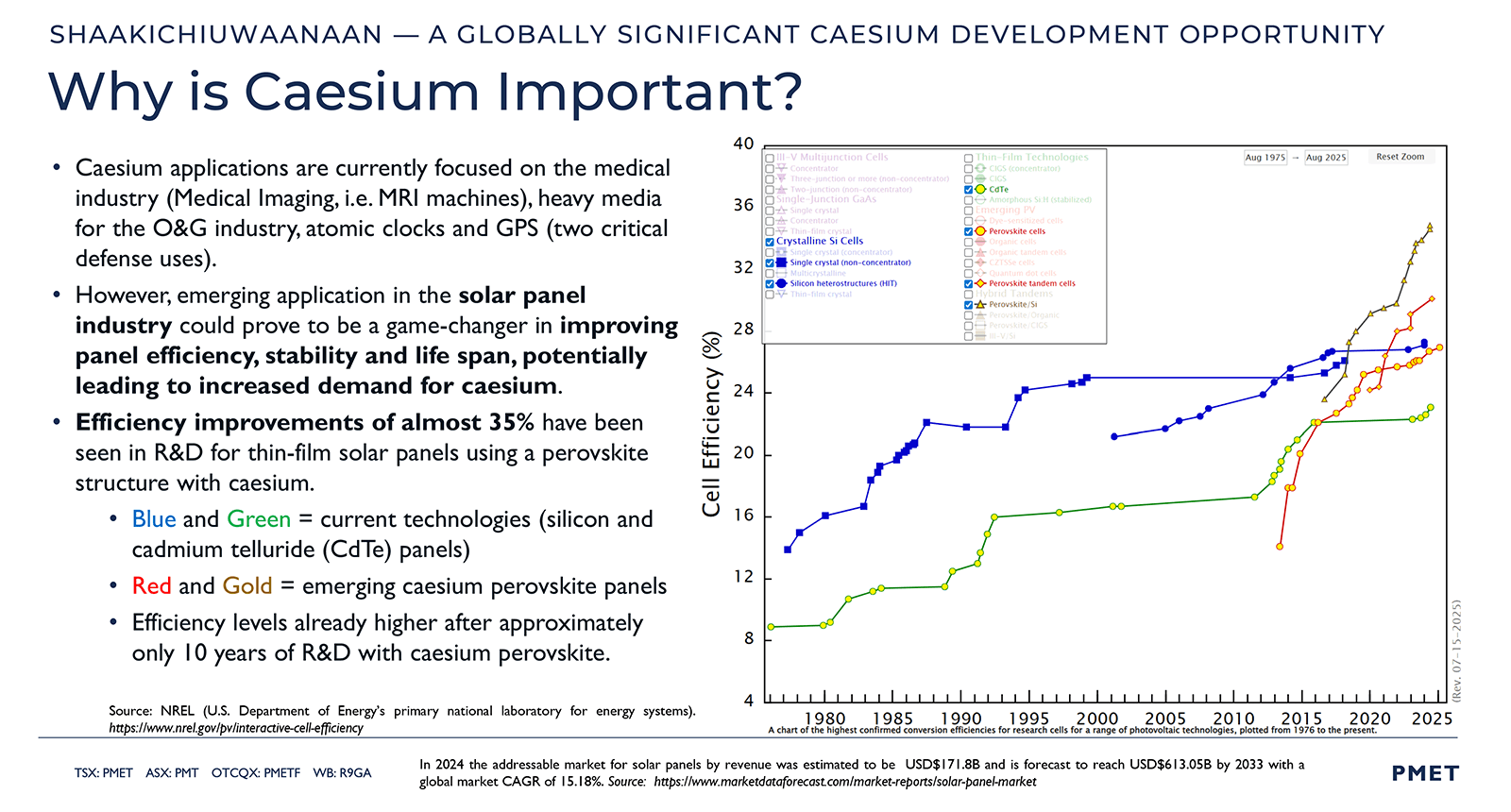

At the same time, cesium demand is rising across next-gen solar cell efficiency, medical imaging, and advanced oil & gas drilling applications.

As a rare and high-security critical mineral, cesium commands premium pricing:

- Cesium carbonate: ~US$120,000 per tonne

- Cesium metal: ~US$2,540 per ounce

What sets PMET even further apart is that the CV13 pegmatite’s cesium mineralization is fully embedded within high-grade lithium and tantalum zones — allowing this deeply mineralized zone to benefit from permitting and infrastructure work already underway for the broader lithium development.

That combination of grade, scale, and co-location within an already advancing development makes the discovery uniquely valuable.

As CEO Ken Brinsden puts it:

“The cesium discovery is remarkable for its incredible scale and grade. In fact, it’s almost unprecedented in the world of cesium.”

Metallurgical testwork using ore sorting techniques is underway with follow-up drilling and stakeholder engagement progressing in parallel.

An expanded cesium resource is under evaluation for Q3 2025 with PMET already fielding inbound interest from downstream industry groups seeking to diversify away from China-dominated supply chains.

Rather than a detour from PMET’s lithium-first strategy, the cesium mineralization represents a clear second-layer value opportunity and one that could play a pivotal role in future offtake discussions and project economics, including with key partners like Volkswagen — a point we’ll return to shortly.

For speculators focused on high-value critical minerals and North American supply independence, PMET’s world-leading cesium discovery adds a powerful new dimension… with plenty more to come.

Strategic Jurisdiction: The James Bay Advantage

In a global environment where permitting delays are worsening and geopolitical risks are rising, location matters more than ever with very few, if any, jurisdictions offering the level of stability, efficiency, and scalability of Quebec’s James Bay region.

PMET’s flagship, 100%-owned Shaakichiuwaanaan project is positioned in one of North America’s most advanced mining corridors, offering:

- Formalized First Nations partnerships and established community engagement

- Year-round access via road and regional airport infrastructure

- Abundant low-cost hydropower and proximity to processing hubs

- World-class tax incentives including flow-through shares and CMETC (Critical Mineral Exploration Tax Credit) eligibility

- Supportive permitting framework with clear federal and provincial alignment

That final point is particularly important. Last year, PMET formally entered Canada’s federal permitting stream — initiating the parallel review process required for large-scale mine development.

According to CEO Ken Brinsden, the response has been faster and more constructive than expected:

“At a federal level, we are seeing a very engaged and positive relationship in respect of the progress of project approvals… and all of that looks to have progressed much faster than would typically be the case.”

On the ground, PMET continues to build what Brinsden describes as a “deep, trusted relationship” with the Cree Nation of Chisasibi supported by employment initiatives, educational workshops, and long-term cultural engagement.

With both federal and provincial Environmental and Social Impact Assessments (ESIAs) expected to wrap by yearend, PMET is targeting mine authorization via COMEX within 12 to 24 months — placing Shaakichiuwaanaan well ahead of global peers navigating slower, riskier permitting regimes.

The advantage is simple yet powerful: resource scale without jurisdictional drag.

It’s the kind of foundational stability that major OEMs and institutional investors demand and a key reason why PMET Resources continues to attract world-class strategic interest.

Volkswagen’s Big Bet on PMET

C$69M Investment, 10-Year Offtake & Global Confidence

One of the most pivotal milestones in PMET’s growth trajectory came in mid-2023 when the company secured a C$69M strategic investment from Volkswagen Finance Luxemburg S.A., a wholly owned subsidiary of the Volkswagen Group.

The deal gives Volkswagen a 9.9% equity stake in PMET, marking one of the first times a global automotive OEM has taken direct equity in a development-stage lithium company.

More importantly, the deal includes a binding offtake agreement with PowerCo SE — Volkswagen’s battery subsidiary — for 100,000 tonnes per year of SC5.5 spodumene concentrate over 10 years contingent on the successful development of the Shaakichiuwaanaan project.

The partnership validates the scale, quality, and Tier-1 location of PMET’s lithium resource while signaling a direct commercial pathway from mine to battery supply chain at a time when Western OEMs are racing to secure critical raw materials.

It also lays the foundation for deeper collaboration with a broader MoU covering joint downstream processing and potential project financing tied to future offtake expansion.

Notably, Volkswagen’s investment came in at a 65% premium to PMET’s 30-day average trading price — a rare and resounding vote of confidence in a newly resurgent lithium market.

And with the majority of PMET’s future lithium production still uncommitted, the company has ample room to bring in additional strategic partners as the project advances toward feasibility, final permitting, and, ultimately, construction.

As CEO Ken Brinsden notes:

“It’s such a good project that you’re going to attract key partners to become part of its future.”

Volkswagen’s buy-in confirms that thesis, and with multiple value streams now in play, additional partnerships could be just around the corner.

Unlocking Major Shareholder Value

Through Upcoming Catalysts

Even after defining the largest lithium pegmatite resource in the Americas… confirming the world’s largest pollucite-hosted cesium deposit… and securing a 10-year offtake agreement with Volkswagen — PMET remains largely undiscovered with shares still trading around US$3.

That’s the opportunity… and it’s why this story remains in its early innings.

With lithium sentiment on the upswing, PMET is emerging as a de-risked, execution-stage developer on its way to becoming a cornerstone supplier of critical minerals in North America.

Here’s what’s coming next and why it matters:

- Lithium-Only Feasibility Study (CV5) - Q3 2025: A major milestone that will define scale, economics, and development strategy while serving as a springboard for final permitting, financing, and construction.

- Federal + Provincial ESIAs Submitted - Late 2025: With dual reviews underway and strong Cree Nation support, mine authorization via COMEX could come within 12 to 24 months.

- Cesium Testwork & Bulk Sampling Pathway: Ore sorting is underway and could unlock a high-value cesium revenue stream with downstream interest already emerging.

- More Strategic & Institutional Interest Likely: Volkswagen’s 9.9% stake and 10-year offtake validate the project’s scale, signaling potential for more partnerships, non-dilutive funding, and expanded offtake.

As noted earlier, these catalysts build on a 30% increase in Indicated lithium at CV5, a 306% jump at CV13, and the confirmation of significant tantalum and gallium credits — including what may prove to be one of the world’s largest hard-rock tantalum resources.

Yet, the stock still trades far below where a project of this scale, clarity, and jurisdictional strength would typically command.

There’s still limited recognition of the cesium discovery, no pricing of the tantalum or gallium upside, and little attention paid to how far PMET has advanced on the geology, permitting, and strategic fronts.

With over C$100M in the treasury, feasibility just months away, and mine permitting well underway… the stage is now set for a rapid rerate that could reward shareholders in PMET’s next phase of growth.

Importantly, PMET continues to explore, grow its resource base, and deliver key development milestones in parallel — executing a multi-pronged strategy few peers can match.

This unique ability to advance exploration and development simultaneously — while remaining fully funded — positions PMET for significant value creation going forward.

How PMET Stacks Up

Scale, Jurisdiction & Multi-Critical Edge

PMET Resources hosts one of the largest lithium pegmatite resources on the planet, a globally significant cesium discovery, and a de-risked development path in Quebec’s Tier-1 James Bay region.

Yet the company still trades at a market cap of roughly US$450 million — well below many advanced-stage lithium peers and a fraction of some in-production names.

For context:

- Sigma Lithium (NASDAQ: SGML) trades at ~US$650M, producing in Brazil with a 270,000 tonne-per-year SC5.5 target at Grota do Cirilo — a scale PMET’s CV5 pegmatite alone could match with throughput studies ongoing.

- Albemarle (NYSE: ALB) trades at ~US$9B and, despite its global leadership, chose PMET for a C$106M strategic investment — a powerful endorsement of PMET’s scale, strategy, and Tier-1 jurisdiction.

- Pilbara Minerals (OTC: PILBF) trades at ~US$4.5B as a dominant Australian hard-rock lithium producer, yet holds no North American foothold — unlike PMET, which offers that exposure early and inexpensively.

None of these peer companies report a cesium byproduct — let alone a defined, pollucite-hosted resource with world-leading scale and grade.

And importantly, none benefit from PMET’s unique combination of:

- A Tier-1 jurisdiction with year-round access

- Dual-track permitting and strong government alignment

- A binding offtake agreement with a major global automaker

The takeaway is clear: PMET’s fundamentals — from scale and jurisdiction to critical mineral diversity and commercial traction — firmly position it among the top tier of North American developers.

A Future Cornerstone for North American Lithium Supply

Today, over 80% of global lithium refining — and more than half of total supply — is controlled by China.

That imbalance remains one of the biggest vulnerabilities in the global battery and EV supply chain.

Governments and automakers across North America are investing billions to localize production and reduce dependence. Yet only a handful of projects have the scale, jurisdiction, and maturity to contribute meaningfully.

PMET isn’t just in the mix — it’s among the few ready to deliver real supply-chain impact.

With a large-scale lithium pegmatite resource defined, a lithium-only Feasibility Study due in Q3 2025, permitting underway, and a 10-year offtake agreement with Volkswagen’s PowerCo, PMET is uniquely positioned to help anchor a secure North American lithium supply chain.

Its location in Quebec adds further strategic weight, combining fast-track permitting and strong Cree Nation partnerships with direct access to emerging battery hubs in Ontario, Michigan, and the Northeastern United States.

Meanwhile, lithium prices have rebounded sharply off 2024 lows with lithium carbonate now trading above US$11,400 per tonne.

Adding fuel to the fire, a major Chinese lithium mine supplying about 6% of global output has halted production after its permit expired — a disruption that could further accelerate the current lithium price surge.

Global EV adoption is also on the rise — surpassing 17 million vehicles sold in 2024 — while demand from stationary energy storage continues to grow rapidly with battery installations ramping up worldwide.

That surging demand backdrop strengthens the case for stable, secure North American supply with PMET now entering its next phase of growth with the critical elements already in place:

- A large-scale, high-grade lithium resource with defined cesium upside

- Over C$100 million in the treasury

- Strong Cree Nation relationships

- Binding commercial alignment with a major OEM

As CEO Ken Brinsden notes, lithium demand is outperforming expectations with critical minerals like cesium and tantalum drawing increased interest from downstream players looking to diversify away from China.

To that end, PMET is advancing one of the few North American assets with the scale, maturity, and multi-metal upside to meet this moment and fuel the next wave of demand.

Exclusive Interview with PMET Resources

CEO Mr. Ken Brinsden

As promised, our own Gerardo Del Real of Resource Stock Digest and Junior Resource Monthly sat down with PMET Resources CEO Ken Brinsden for a firsthand look at the company’s evolving strategy and the key milestones shaping its next phase of development.

Behind every world-class mineral discovery is a world-class team… and in PMET’s case, it starts at the top.

At the helm is Ken Brinsden, a globally respected lithium executive best known for leading Pilbara Minerals from junior explorer to ASX-100 lithium powerhouse.

Now, as president & CEO of PMET, he’s applying that same discipline, scale-driven thinking, and executional focus to the Shaakichiuwaanaan project with results that are turning heads across the critical minerals supply chain.

In this exclusive conversation, we delve into Ken’s vision for PMET, the catalysts ahead, and how he sees lithium and cesium reshaping Western supply dynamics over the next decade.

Supporting Brinsden is a highly capable technical team with deep experience in lithium exploration and mine development.

That leadership includes industry professionals like Darren L. Smith, a leading expert in hard-rock lithium pegmatites who played a key role in defining both the CV5 and CV13 systems now anchoring PMET’s development strategy.

Working alongside him is Frédéric Mercier-Langevin, a proven operator and former COO of Wesdome Gold Mines who brings hands-on expertise in building and scaling advanced-stage projects in Quebec’s Tier-1 James Bay region.

Rounding out the technical team is newly appointed director Ms. Aline Côté who brings global operational experience — including senior roles at Glencore — as PMET transitions from discovery to development.

Together, this team is not only unlocking one of the most strategically important lithium-cesium systems in the world… they’re doing it with the credibility, partnerships, and jurisdictional advantages most peers can only hope to replicate.

So let’s dive in as Brinsden lays out what’s next for PMET from the upcoming Feasibility Study to Volkswagen’s involvement and the potential for new strategic partnerships and why the most significant value creation may still lie ahead.

Gerardo Del Real: This is Gerardo Del Real with Resource Stock Digest. Joining me today for a long-overdue catch-up is the quarterback and CEO of PMET Resources — Mr. Ken Brinsden. Ken, it’s great to have you on, sir. How are you today?

Ken Brinsden: Fantastic to be with you, Gerardo. I really appreciate the opportunity.

Gerardo Del Real: Listen, as a long-term supportive shareholder, it puts a smile on my face that despite your incredible past success — and the incredible success you’re having now with PMET — you’re still working hard. We appreciate that.

Let’s get right into it. We have a situation in the lithium space that’s changing in terms of the overall landscape. It’s been a frustrating couple of years for anyone who’s been in this space. We had a phenomenal period where it felt like investing in lithium stocks and miners was easy. You just put your money in, wait, and one day you wake up with more money.

What we’ve seen in the last 18 to 24 months is a pretty expected but more severe consolidation than many had anticipated. Expected in the sense that we all knew it had to pull back. It wasn’t sustainable at that pace. Now, I look at the landscape, and I look at your background and think: okay, deep, severe consolidation — and in the meantime, Ken and the team have added phenomenal value.

You now have not just one world-class discovery but potentially several world-class discoveries on a single project. And oh, by the way, you’ve brought in people who, to me as a shareholder, signal: ‘We’ll take this to production if we absolutely have to — no problem. We’ve done it before.’ You’ve obviously done it before.

I want to get your take on all of that. Let’s start with how you view the changing landscape because I’m starting to see a lot of green shoots in the lithium space, and the demand side of the picture is doing exactly what I thought it would.

Ken Brinsden: Gerardo, you’re right that it has shifted from being a supply-side debate over the past couple of years where China had a big influence on the market. And I honestly believe we’re now through the trough and coming out the other side. I think demand is going to outstrip expectations.

But it’s the same old story, Gerardo. It’s still very much about what China’s up to — and they really are changing the game. Lower-cost cells are translating into a heap more EVs, globally, because China is a major player in a lot of export markets. And it’s those low-cost cells that are making their way into new applications where the tech can be deployed economically.

One standout is the stationary energy storage sector, which is really a phenomenon, Gerardo. That one’s probably being grossly underestimated in terms of how fast it’s growing.

Just to give you some perspective: this year, growth in stationary energy storage is up over 50% — almost double the rate of EVs, which are in the 27-28% range. And that sector is going to be a big one in the coming years. It’s a really important driver of demand growth that’s being largely underestimated.

So yes, there’s plenty of reason to be optimistic about lithium raw material demand.

Gerardo Del Real: Let’s get specific with PMET Resources. You have an emerging — and for you, a bit of déjà vu — world-class discovery. And I think this one is going to be significant not just for Canada, not just for PMET, but for all of North America.

I believe deposits of global significance, especially in North America, are going to command a substantial premium in the coming years. And you don’t just have lithium; you potentially have three or even four different metals in high demand.

I want to start with the flagship, the lithium, because I know the cesium has recently and rightfully attracted a lot of attention. And we’ll definitely get to that.

But let’s begin with lithium. That’s what initially attracted Volkswagen to partner with you. It’s why Albemarle came in at a significant premium and wrote a check. And oh, by the way, having C$100 million in the treasury and continuing to add this kind of value during a broader consolidation has been brilliant execution despite what the share price may suggest.

Where are you currently with the lithium resource… and what’s next, especially with the Feasibility Study, which I think will highlight a lot of key factors and give us a clearer window into the potential economics moving forward?

Ken Brinsden: Yes, it’s a phenomenal piece of geology, Gerardo. When you’re in the hard rock world, you’re looking for these classic LCT resources: lithium, cesium, tantalum. That’s what the geos will refer to. But it’s very rare that you get the confluence of all three — and some additive minerals — in one piece of geology.

Yet that’s exactly what we have at Shaakichiuwaanaan.

World-class lithium in terms of both scale and grade... cesium now proven at scale and grade in the maiden resource... and a tantalite resource that many would be jealous of if tantalum was your only focus. So yes, it’s really an incredible piece of geology — and it’s for all of those reasons that we’re excited about the project’s potential.

Onto the Feasibility Study — spot on, mate. We’re only a month or two away from presenting the updated economics around a lithium-only CV5 development.

If I take you back to ground zero: we have the CV5 resource — lots of lithium there — and more lithium, cesium, and tantalum at CV13. And just to be clear, the Feasibility Study is focused on lithium only at CV5. That’s what we’re delivering, and that’s what ultimately gets us through the next phase of mine authorization — the presentation of the Feasibility Study and the environmental approvals documentation.

The value-add we expect from the other co-products — particularly cesium and tantalum — will be captured in the detailed engineering phase, which will happen as we go through that first round of mine authorization.

So just to be clear again: lithium only at CV5 for the Feasibility Study. Still a fantastic project. The economic upside from the cesium and tantalum will come in in the next step beyond the feasibility. We’re looking forward to demonstrating what’s possible there because those co-products are also material to the overall project.

Gerardo Del Real: For the generalist out there… and let me be clear, I consider myself a generalist, I’m not a geologist… when we look at the cesium, the tantalum, and the lithium, I have to imagine you’re having conversations with chemical companies, auto companies, etc.

Are you having separate discussions about each or are there conversations happening around all three? Because there are applications for all three metals where, hypothetically, you could send 25%, 50% of each to a single client in exchange for an offtake, right?

Or are those completely separate discussions at this point? I see the smile. I don’t know if you’re going to answer it.

Ken Brinsden: [laughs] No, no… I reckon you’ve raised a really interesting point there.

Actually, what it highlights is the issue of concentration. The way the industry thinks about this stuff is that they worry about the concentration risk going downstream through China. And if you were to say, ‘Could you send all of them in one direction?’ it would probably be toward China.

But of course, most people in the industry, especially those focused on North America and Europe, are thinking about diversifying their supply chains and moving away from that concentration risk in China.

What that has flushed out — and what I’m really pleased to report — is that as we’ve made these discoveries, we’ve been getting genuine inbound interest from counterparties who are motivated to talk about the potential in the resource.

Cesium is the most recent example. We made the discovery announcement even before the resource was out, and we were already getting inquiries as to what could be done with that product, especially from groups looking to diversify supply chains beyond China.

Cesium is interesting because, like a lot of critical minerals, it’s almost entirely controlled by China. So people are very interested in what the alternatives might be. And for those reasons, we’re happy to engage with them.

That doesn’t mean you don’t ultimately have the opportunity to sell to China. It just means there are parties actively looking for alternatives. And again, we’re happy to have those conversations

Gerardo Del Real: Excellent. Let’s get into that maiden resource on the cesium front.

Ken Brinsden: Yes, it’s really exciting because it’s pretty much unprecedented in its scale. The grade, in certain subsets of the resource, is kind of off the charts. So yes, we’re really happy with the outcome there, Gerardo.

It’s a fantastic resource — in total, about 2.3 million tonnes. I know that sounds incredible in the cesium world because the next biggest resource, we believe, is the Tanco mine, and that’s around 150,000 tonnes. So this has incredible scale, amazing grade, and we’re really keen to demonstrate what’s possible with that resource over the coming months and years.

Gerardo Del Real: I had the pleasure of speaking with Mr. Jody Dahrouge — who I know you’re familiar with — a few weeks back. He and I were just kind of shooting back-of-the-napkin notes, and we were speculating that there could be a couple billion dollars just in cesium here. And the resource estimate didn’t do anything to disappoint that hypothesis, right?

Thoughts on the potential value there? Do you want to get into that at all?

Ken Brinsden: Yes, so the mineral pollucite is similar to what spodumene is to lithium. In the case of cesium, it’s the pollucite concentrate that delivers it. You’re essentially following a similar path to lithium; it’s just typically done on a smaller scale.

Yet the core idea is that the pollucite concentrate gets chemically treated and produces really high-value mineral species used in very specific and, in some cases, incredibly high-value applications. Things like medical imaging, deep oil and gas drilling, and optoelectrical uses are where cesium comes in.

And now, with newer technologies, we’re seeing developments that improve the efficiency of solar panels. That’s where we see the next wave of tech — improvements in solar efficiency — and they’re probably going to rely on inputs of cesium.

Gerardo Del Real: Right.

Ken Brinsden: The industry has been a bit fearful about whether cesium could become a real growth opportunity. And they’ve been worried about where supply would come from.

So a discovery like ours at significant scale creates more abundance of cesium, and that starts to open doors. The market begins to grow. That’s really what we’re focused on, Gerardo: the idea that new technology pathways are going to grow the market for cesium.

And if you’ve clearly got the world’s biggest cesium resource… well, you’re going to be a target for more and more discussions on how to make that a reality.

Gerardo Del Real: Yes, North America; again, the world’s largest resource. Champagne problems on that front, right?

Ken Brinsden: Yep, you don’t need to go to Greenland or Ukraine for your critical minerals.

You’re right across the border in Canada in Quebec. It’s fantastic!

Gerardo Del Real: I spoke earlier about the share price performance… and sure, we’re up some 120% over the last month or so. But for those of us who started way back at 16 cents Canadian, rode it to C$17, and are now back around C$4.20 — it’s definitely been a roller coaster ride.

The end game, in my opinion, has never really been in doubt. It’s just all of the in-between noise. And I get the frustration from some shareholders.

But one thing I’ve always preached to subscribers, shareholders, friends, and family — and our group still owns a substantial amount of shares — is the value that has been added during the consolidation.

What I try to explain is that you have to look at the forest, not just the trees. If the end game was always to let Ken and the team take this to production — or sell it at a significant premium well above today’s prices — then all of the in-between stuff… sure, I’d rather see the price higher than lower but it’s just noise.

The emphasis I’ve really tried to drive home is the amount of value added over the last couple of years. And it’s not just value in the ground. With new metals discoveries and the expansion of these zones, which are still wide open… I think that part is underappreciated. But also the team — the human value. The expertise you’ve added. People who’ve been through this rodeo before. People who’ve taken it all the way with you in the past and actually put projects into production.

Can you speak to some of those additions to the board and to the team because I think that also doesn’t get enough attention when we talk about the next stage here of potentially involving several world-class metals discoveries of global significance.

Ken Brinsden: Yes, I’m really pleased and proud to be working with what I consider to be a fantastic team. When I think back to the development of Pilbara Minerals — fighting your way through those tougher periods — it really takes a great team to remain focused to realize the potential in what you know is an amazing project.

And I’m certain we have those characteristics at Shaakichiuwaanaan and within PMET: a combination of unbelievable geology and a really strong project and the right expertise to continue delivering. That means de-risking the project so you ultimately reach production and create excellent outcomes with great customers and key partners involved.

We’ve made some really strong additions to the team in Montreal, and I’m so pleased to be working with them. Each one is capable in their own right. And you don’t attract the likes of Volkswagen making what is really their first-ever mining investment without having those key characteristics in place: a great project and great people who are ultimately going to contribute to its success.

I’m really pleased with the progress there too, Gerardo, and we’re looking forward to continuing to demonstrate what’s possible with the project.

Gerardo Del Real: You touched on Volkswagen, and we touched on the North American premium that I think should accompany every metals project — whether it’s lithium, uranium, or copper — that has significant scale.

We’ve seen it in the uranium space: AI and tech companies coming in looking for energy to power their ambitions for the next several decades; even the Department of Defense here in the US taking direct stakes in companies.

Do you see the potential or have you heard of any potential discussions where that kind of activity could spill over into the lithium space, especially as we head further into this situation with China? It used to be what I called a quiet Cold War but it’s not so quiet anymore, particularly when it comes to resource independence.

Do you think that dynamic could spill into the lithium space?

Ken Brinsden: Yes, I’m certain that process is already underway, Gerardo. We now think about Shaakichiuwaanaan as a critical minerals story. It’s not just a lithium story anymore.

The combination of cesium and tantalum, and potentially other key elements down the track — like gallium and rubidium, which we’re also focused on — means people are paying attention to projects that can genuinely add value to the North American critical minerals narrative.

Why are they so focused on it? Well, it all comes down to the concentration risk that now exists through China.

China got well ahead of the game in the critical minerals space over the past 15 years, and now it’s the West’s time to play catch-up. And part of that means getting invested and underwriting project development so that these alternative supply chains can actually make it to market.

The danger is that if the West doesn’t start responding now — and I think the US is especially sensitive to this — then there’s a real risk that we fall further and further behind to the point where you simply can’t catch up.

Gerardo Del Real: Sure.

Ken Brinsden: A kind of microcosm of what I’m trying to describe is actually what’s happening in the car industry. The Western car industry is under real threat right now because of the rise of Chinese national brands. And it’s not some overnight success story — it’s the result of about 15 years of building capability, quality, and lower costs.

A lot of that centers around batteries. And honestly, it’s getting to the point where the West’s car industry is in serious trouble. One of the reasons we chose to work with Volkswagen was because of their intense focus on solving these challenges for Western automakers, particularly within the brands under the VW Group.

And their response is real. They’re making mining investments, and they’re investing in cathodes, batteries, and new car plants. They’re embracing hybridization to help address US range anxiety. All of these things are core to their strategy, and they’re investing like there’s no tomorrow.

Billions of dollars are going into the North American market to establish a real and growing presence at the same time that their business is getting hammered in China.

I focus on Volkswagen because they’re a relatively rare breed now, Gerardo. A lot of car companies are asleep at the wheel and not seeing what’s happening with the rise of Chinese national brands.

In the US, maybe you don’t see it quite as much yet. But in Australia, I can tell you, BYDs are everywhere. They’re dominating the streets. There’s a particular truck — the BYD Shark — that just blows me away on how many of them I see driving around Perth.

It’s really taking off. And it’s a sign that we need to be doing better in the West. And that’s why investment — like what you described — is a natural and necessary step to ensure the survival of key industries.

Gerardo Del Real: Well listen, no doubt PMET is going to play an important part there. You have approximately C$100 million in the treasury. How does that get allocated over the next six to twelve months, and what can we as shareholders expect to see from PMET Resources?

Ken Brinsden: Yes, spot on, Gerardo. We are doing a little bit more drilling. It’s more targeted now and not quite the same scale of programs we ran over the past couple of years because we’ve already broken the back of the resource base to support the Feasibility Study. But there’s still exploration intent, and we want to make sure we’re continuing to uncover new opportunities.

I mean, look at what has arisen with the cesium component — and there’s still plenty of lithium exploration potential as well. So that’s part of it.

We’re also completing the Feasibility Study and the environmental approvals documentation, which gets us through the last hurdle for mine authorization. Once we submit the feasibility and environmental documents later this year, you’re looking at about 12 to 24 months for that authorization process.

So yes, those are our key focuses.

We’re also going to progress the economic opportunity in cesium and tantalum. As I mentioned earlier, those really start to come into play once we’re through the feasibility phase and into detailed engineering. I’m excited about that as they represent real value-add beyond lithium.

It’s a fantastic credit to the project that you genuinely have all three… the L, the C, and the T: Lithium, Cesium, Tantalum.

Gerardo Del Real: I think a lot of people are underestimating the next six to twelve months. I don’t want to say material catalyst because you have several of those but you know how the general investor and speculator is: they want to see drilling, they want to see blockbuster results.

But once you get into feasibility studies and the real work that allows you to go from developer to producer — that’s the stuff that has to happen, and it’s starting now.

I think people are underestimating the potential for Volkswagen — or maybe another group, a chemicals company or vehicle company — to come in and say, ‘This is really unique. We want more of it, and we’re willing to work together in a number of ways.’

I think it’s going to be a fun six to twelve months watching you continue to deliver, and I’m really looking forward to the upside surprises on that front. I know you’re coy and like to play it close to the vest but I think it’s going to be a great, great run.

Before I let you go, Ken, any thoughts on the lithium spot price? I know the futures had a bit of a pullback. That’s going to happen. But we’ve had a relatively robust last three weeks or so, and it seems like we’re starting to see some cracks in China’s ability to keep flooding the market with cheap material.

Where do you think we go over the next few quarters?

Ken Brinsden: Yes, the sector is due for some upgrades as the brokers and analysts are a bit behind when it comes to the demand equation.

That’s the key now: demand has been outperforming expectations year-to-date. Lithium raw material demand is up around 30-35% so far this year, whereas most analysts and brokers are still sitting at around 20%. So there’s a gap emerging and it’s real. That’s one of the reasons you’re starting to see prices respond.

The bigger picture is that China is moving the market faster than most in the West have given them credit for. They’ve overbuilt cell-making capacity, and now they can switch that on with lower-cost cells being contracted globally.

One area that really stands out — and I’ve said it before — is stationary energy storage. That’s a key phenomenon. Another is trucks and buses within China itself. There’s a lot happening, and it’s all moving faster than most would’ve assumed.

So, with all of that, I think the sector as a whole is due for upgrades. And I think we can safely say we’ve now seen the bottom. As uncomfortable as it’s been, we’re probably through it. Now, it’s all about engagement with industry.

You mentioned, Gerardo, that our project is good enough that we can continue building the consortium that’s going to take it through to production. There are more deals to be done, and they’re going to be important for the progress of our project. We’re really looking forward to showing what that looks like.

Gerardo Del Real: Ken, it has been an absolute pleasure, and I’m excited for what comes next. Thank you so much for your time.

Ken Brinsden: My pleasure, Gerardo. Great to be with you. Thank you.

The PMET Resources Opportunity

PMET Resources Inc. (TSX: PMET)(OTCQX: PMETF)(ASX: PMT) stands at a pivotal moment — backed by a world-class resource in a Tier-1 jurisdiction and a globally significant cesium co-product now confirmed by a maiden Mineral Resource Estimate.

The flagship Shaakichiuwaanaan Project (formerly “Corvette”) in Quebec’s James Bay region is advancing rapidly on multiple fronts.

A lithium-only Feasibility Study for the CV5 pegmatite is expected in Q3 2025 with both federal and provincial permitting processes already underway and supported by strong Cree Nation engagement.

A strategic partnership with Volkswagen’s PowerCo — anchored by a C$69M equity investment and 10-year spodumene offtake agreement — puts PMET in rare company among global lithium developers.

You heard directly from CEO Ken Brinsden who says:

“It’s such a good project that you’re going to attract key partners to become part of its future… There are more deals to be done, and they’re going to be important for the progress of our project.”

With lithium carbonate prices rebounding sharply off 2024 lows — now trading above US$11,400 per tonne — the macro backdrop is once again aligning in favor of well-positioned developers like PMET.

Add to that the accelerating buildout of EVs and storable energy infrastructure and PMET emerges as one of the few near-term contributors to the West’s critical mineral supply chain.

With key catalysts now in motion, PMET’s development path from feasibility to production is clearly laid out.

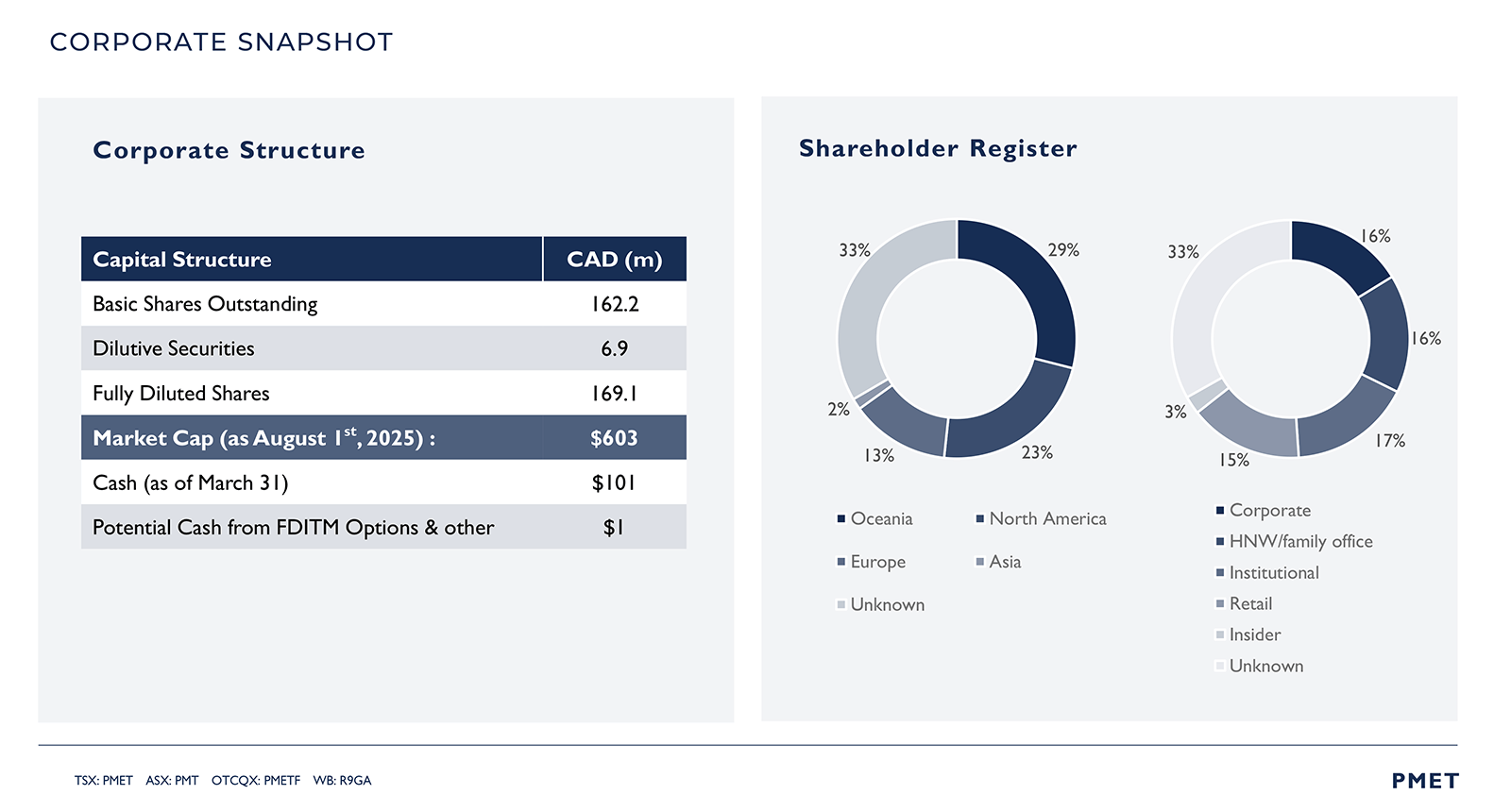

Financially and structurally, PMET is exceptionally well positioned with over C$100M in the treasury, a tight share structure, and listings across North America and Australia. The company’s share structure and capital exposure are summarized below.

Yet shares still trade around US$3 — a substantial discount to peers with less scale, weaker jurisdictional footing, limited permitting progress, and no exposure to high-value critical minerals beyond lithium, including cesium, tantalum, and gallium.

That’s where PMET truly stands apart.

In addition to lithium, the Shaakichiuwaanaan project hosts the largest pollucite-hosted cesium resource in the world, confirmed tantalum and gallium credits, and significant expansion potential across additional pegmatite clusters.

Add in Ken Brinsden’s proven success at Pilbara, and it’s clear this is a team that knows how to scale and attract high-level strategic interest.

And remember, this is no longer just a lithium story: It’s a fast-moving, multi-critical mineral play advancing toward a key role in the North American supply chain.

With a key Feasibility Study underway, permitting advancing, and strategic interest accelerating, now is a prime moment for speculators to take a close look at PMET Resources — a timely, high-upside opportunity with multiple catalysts on deck.

A great place to start is PMET’s corporate website where you can explore the properties, meet the team, and sign up for direct updates from the IR department.

View the most recent Corporate Presentation here.

Also, click here for more of our ongoing coverage of PMET Resources, including additional late-breaking interviews with upper management as developments arise.

PMET Resources Inc. trades on the TSX under the symbol PMET, on the US OTCQX under the symbol PMETF, and on the ASX under the symbol PMT.

— Resource Stock Digest Research

Click here to see more from PMET ResourcesIMPORTANT DISCLAIMER & DISCLOSURES

Resource Stock Digest, as a publisher, is not a broker, investment advisor, or financial advisor in any jurisdiction.

Please do not rely on the information presented by Resource Stock Digest as personal investment advice.

If you need personal investment advice, kindly reach out to a qualified and registered broker, investment advisor, or financial advisor.

The communications from Resource Stock Digest should not form the basis of your investment decisions. Examples we provide regarding share price increases related to specific companies are based on randomly selected time periods and should not be taken as an indicator or predictor of future stock prices for those companies.

PMET Resources has sponsored this report.

The information in this newsletter does not constitute an offer to sell or a solicitation of an offer to buy any securities of a corporation or entity, including U.S. Traded Securities or U.S. Quoted Securities, in the United States or to U.S. Persons. Securities may not be offered or sold in the United States except in compliance with the registration requirements of the Securities Act and applicable U.S. state securities laws or pursuant to an exemption therefrom.

Any public offering of securities in the United States may only be made by means of a prospectus containing detailed information about the corporation or entity and its management as well as financial statements. No securities regulatory authority in the United States has either approved or disapproved of the contents of any newsletter. Neither Resource Stock Digest nor any employee of Resource Stock Digest is registered with the United States Securities and Exchange Commission (the “SEC”): as a “broker-dealer” under the Exchange Act, as an “investment adviser” under the Investment Advisers Act of 1940, or in any other capacity. Resource Stock Digest, its owners, directors, and employees are also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

HIGHLY BIASED:

In our role, we aim to highlight specific companies for your further investigation; however, these are not stock recommendations, nor do they constitute an offer or sale of the referenced securities. Resource Stock Digest has received cash compensation from PMET Resources and is thus extremely biased. It is crucial that you conduct your own research prior to investing. This includes reading the companies' SEDAR and SEC filings, press releases, and risk disclosures. The information contained in our profiles is based on data provided by the companies, extracted from SEDAR and SEC filings, company websites, and other publicly available sources.

Resource Stock Digest, and its owners, directors, employees, and members of their households may own shares of PMET Resources. Therefore, Resource Stock Digest is extremely biased. Measures are in place such that no shares will be sold during the active awareness campaign.

HIGH RISK:

The securities issued by the companies we feature should be seen as high risk; if you choose to invest, despite these warnings, you may lose your entire investment. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures.

NOT PROFESSIONAL ADVICE:

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Resource Stock Digest, and all partners, members, and affiliates harmless in any event or claim. While Resource Stock Digest strives to provide accurate and reliable information sourced from believed-to-be trustworthy sources, we cannot guarantee the accuracy or reliability of the information. The information provided reflects conditions as they are at the moment of writing and not at any future date. Resource Stock Digest is not obligated to update, correct, or revise the information post-publication.

FORWARD-LOOKING STATEMENTS:

Certain information presented may contain or be considered forward-looking statements. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results or events to differ materially from those anticipated in these statements. There can be no assurance that any such statements will prove to be accurate, and readers should not place undue reliance on such information. Resource Stock Digest does not undertake any obligations to update the information presented or to ensure that such information remains current and accurate.