Best In Rare Earth Class And Undervalued: Tasman Metals

Editor's notes: TAS is the best way to play the rare earths space, says The Critical Investor. Limited risk and big potential could mean 50% near-term upside and more in coming years.

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in TAS over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

1. Introduction

For a few months, I noticed increased attention for rare earth junior mining companies after a long period of relative silence. It must have been more than two years since I sold my own, highly speculative, rare earth plays Great Western Minerals and Stans Energy. My IB platform let them go just one day after they spiked on February 8, 2011 when these stocks fell through my trailing 20% stop-loss, which I like to use in a run up for this kind of speculative stocks. Looking back, this day could have been the end of the rare earth elements (REE) hype at that very moment, and the start of a formidable retraction of all mining stocks, as the most speculative stocks usually go down first when confidence starts to seep out of the markets.

(click to enlarge)

TSX Venture, 5-year period

Back then, it didn't matter which rare earth stock was picked, everything that barely mentioned "rare earths" went up 500-1000% within the previous 6 months. This was often based on nothing but some drill results, an inferred resource estimate or some vague promises by companies, driven by expected implications by the Chinese restricting REE exports at that time, sending REE prices through the roof. Very complex issues like metallurgy or cash costs weren't known or regarded at all. It was a time when some overly enthusiastic analyst reports came out, among others estimating targets like $160 for Molycorp (MCP) (back then trading at $50, now at $7.40). These days are long gone now, REE prices have come down 80-90% as China normalized exports, and most REE companies lost 80-95% of their value as a consequence. Since 2011, a distinction slowly arose between light and heavy rare earth minerals as the heavy REEs (HREEs) appeared to be really rare, compared to light REEs (LREEs) which were found in large deposits globally. The LREEs are produced in abundance in China (and later on also by Molycorp and Lynas), and therefore always have been relatively very low priced, compared to the HREEs. Just a few companies outside of China managed to build a solid business case based on heavy REEs since 2011, cases that actually could result in a producing rare earth mine.

The company which came out on top during my research to find the best REE explorer of the moment is Tasman Metals (TAS), whose flagship project Norra Karr contains one of the highest percentage of heavy REEs at 51.8%, and recently produced a Preliminary Economic Assessment (PEA) with one of the highest Internal Rates of Return (IRRs) of all junior REE miners with substantial deposits. Very important as well is Tasman Metals' initial capex, which is much lower than those of most of its peers, as it is very difficult nowadays (or anytime soon) to raise the necessary funds. An extensive comparison on much more parameters will be made in this article between Tasman Metals and its peers to show why this company could be considered best in class. A target share price for 2017 (when the company expects to reach the commercial production phase) will be estimated as well, and I will also provide a current target share price as I am convinced the company is undervalued at the moment.

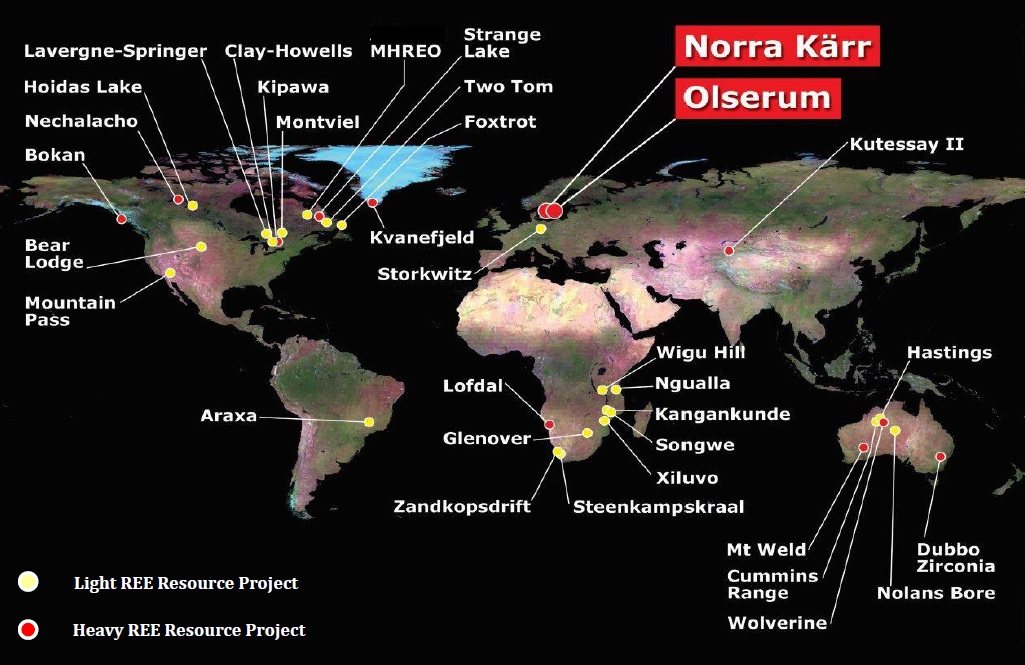

(click to enlarge)

REE projects worldwide

2. Executive summary

Tasman Metals (TAS, or on the Canadian main board: TSM.V) is a Canadian based and Scandinavian focused mineral exploration company with extensive claim holdings in Sweden, Finland and Norway that are prospective for strategic metals, including rare earth elements, iron ore and very recently also tungsten. Its flagship project Norra Karr contains one of the highest ratios of heavy REEs at 51.8% and the company recently announced a very positive Preliminary Economic Assessment (PEA) on July 9 of this year. The PEA reveals a high after tax NPV@8% of $1,464M, one of the highest after tax IRRs (45%), of all junior REE miners with substantial deposits in combination with a relatively very low initial capex of $266M (including a healthy 20% contingency).

As Tasman Metals has very good fundamentals, actually the best of all REE-juniors as far as I am concerned, it would likely be just a matter of fast-tracking towards production in 2017, as the project is already considerably derisked by the latest PEA and the already obtained test results on metallurgy.

First positive catalyst could be better than expected results of ongoing metallurgy testing at its pilot plant, to be expected in November/December 2013.

After this, Tasman is expected to finalize the conversion of Indicated resources into Measured resources by an updated NI43-101 resource estimate, in Q1 2014.

Next up is the release of a Pre-Feasibility Study (PFS), scheduled for Q2 2014. which will be very important as it could confirm or even improve the very good PEA results, and derisks and fine-tunes the project further. The release of a Feasibility Study (FS) is planned for Q1 2015. When the FS is positive, or even after a positive PFS, construction is expected to begin in Q3 2015, and production in Q1 2017.

One issue that can have a large, positive impact on the business case of Tasman Metals, is increasing of the prices of rare earth minerals. Prices have come down 80-95% since the absolute peak in 2011, stabilizing roughly at 100-300% above 2010 prices, and rising again lately.

There are also negative catalysts. As the rare earth industry is dominated by China (92-97% of global production), any interruption or increase of supply by this country could have serious ramifications for pricing levels globally, rendering the case of Tasman Metals less positive in case of supply increase. I already explained in another article why I don't consider China a very trustworthy party to deal with, this will remain a risk for some time to come. For now the situation seems to be under control, but as China has its own agenda things could change rapidly.

Other risks are of course negative results and outcomes on all scheduled estimates and reports. I don't expect the resource estimate and PFS to disappoint, as the deposit is very consistent and the PEA is already conservative in its fundamental metrics. In the longer term (2014-2015 onwards) some of the competitors could cause problems when they manage to commence commercial production before Tasman Metals does, as they are more likely to provide enough supply first and win the HREE production race in this case. Despite a lot of rosy schedules of these competitors, this isn't very likely to happen as already further advanced companies have serious disadvantages in raising funds for construction, being able to compete on HREE territory, or obtaining mining permits.

To determine the value of the company, a combination of a derisking factor based on extensive peer comparison, this year's price action of its peers and a discounted NPV/market cap ratio is used. Taking into account a current share price of $0.72 (10/11/2013), based on 60.85M shares we get a target share price of $1.08, for an estimated profit of 50% at this moment. For investors with more patience, in 2017 when Norra Karr should be in commercial production, the target share price is estimated with a very conservative 50% discount on NPV@8% at $5.94 for an estimated profit of 725%.

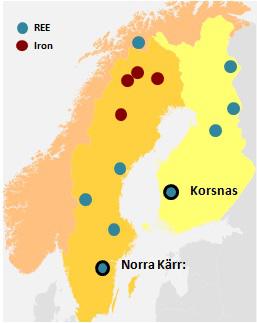

Tasman Metals, geographical distribution of projects

3. Rare Earth Elements

Before describing the company, I would like to provide some background information on rare earth elements itself. Rare earth elements are used in many alternative energy, lifestyle, and defense applications. Alternative energy systems such as wind power generation, fuel cells, hydrogen storage, rechargeable batteries, and the permanent magnets used in electric and hybrid-electric vehicles all rely on rare earths. REEs are used as phosphors in many consumer displays and lighting systems, and are used in fluid cracking catalysts and catalytic converters in the oil and automotive industries. REEs are also vital for many defense technologies, including precision guided munitions, targeting lasers, communications systems, airframes and aerospace engines, radar systems, optical equipment, sonar, and electronic countermeasures.

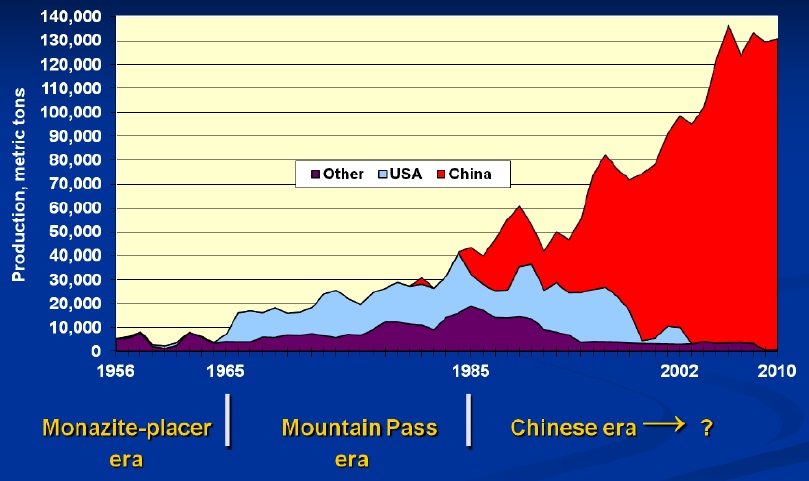

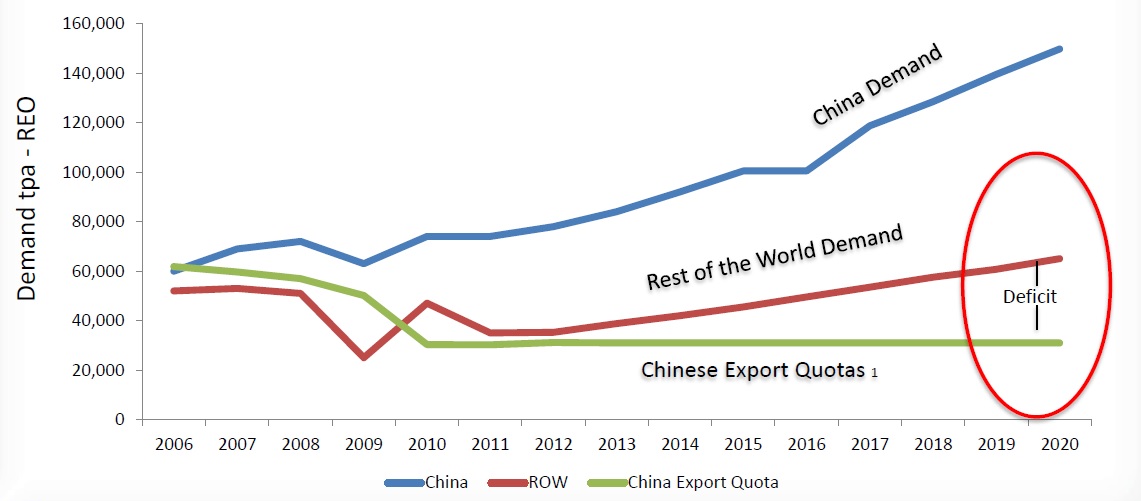

The supply of rare earths is dominated by China, which provides 92-97% of the world's production. However, China only has 48% of the world's known reserves of rare earths, according to the USGS Mineral Commodity Summaries. Due to growing internal demand, industry consolidation and stricter internal environmental regulations, China has imposed export quotas on rare earths. This creates two separate rare earth markets, one internal Chinese market and one for the Rest of the World (ROW). The Chinese export quota amount therefore defines the majority of REE supply for the ROW, and therefore its pricing.

(click to enlarge)

Industry experts are trying to forecast the REE supply and demand figures, but this is not easy, as each rare earth element has different end uses and applications, and is produced in different quantities. This means that certain rare earths, including Neodymium, Europium, Terbium, Dysprosium, and Erbium are and will be in a supply deficit, while more abundant rare earths such as Lanthanum and Cerium will be in surplus.

(click to enlarge)

Combined REE supply and demand

Personally I think this chart is too positive, as China and the world economy as a whole are slowing down. However, China turning into a more consumer driven economy (as is the intention of national government at least) could mostly neutralize this slowdown regarding REEs.

Western LREE production isn't on schedule and progressing as planned. Furthermore China is regulating its production at the moment as it adjusts or closes illegal REE mining operations. Therefore, my personal assumption is a more moderate growth in demand, and a moderate growth in supply as well.

Nevertheless, the dominance of China in the sector is overwhelming, and this already caused supply problems in the recent past for the rest of the world. This dependence is further reinforced by the current lack of rare earth production infrastructure and processing knowledge in the rest of the world. Also, because each rare earth deposit is unique and contains the various REEs in different proportions, individual elements are produced in different quantities. Besides this, end users require tailor-made rare earth oxides and other related products, therefore limiting flexibility for producers to stockpile or sell to random off takers.

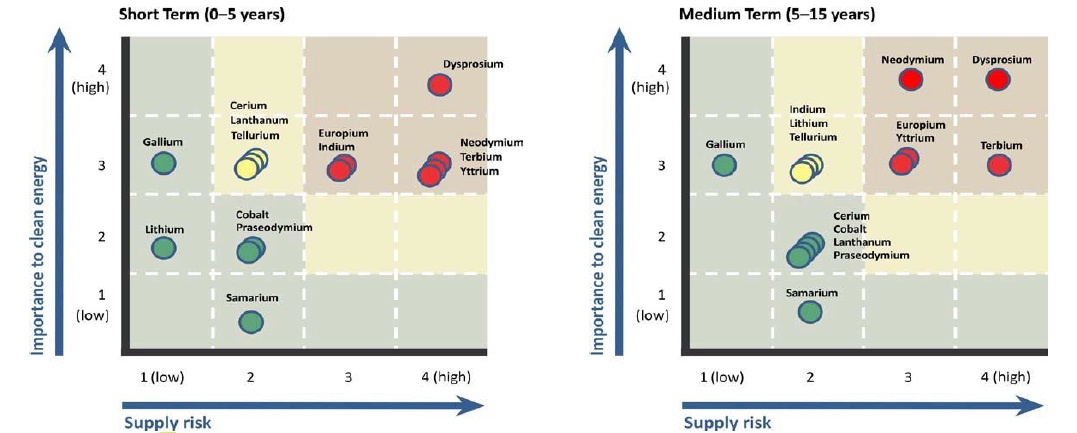

Some rare earths are likely to stay in short supply even though the total supply is forecast to exceed total demand by 2015. The US Department of Energy has identified 5 critical elements that are at a serious supply risk over the next 15 years: Dysprosium (DY), Terbium (Tb), Neodymium (Nd), Europium (EU) and Yttrium (Y)

(click to enlarge)

Most of these critical elements are part of the so-called "heavy rare earth elements" or HREEs as they have a bigger mass:

(click to enlarge)

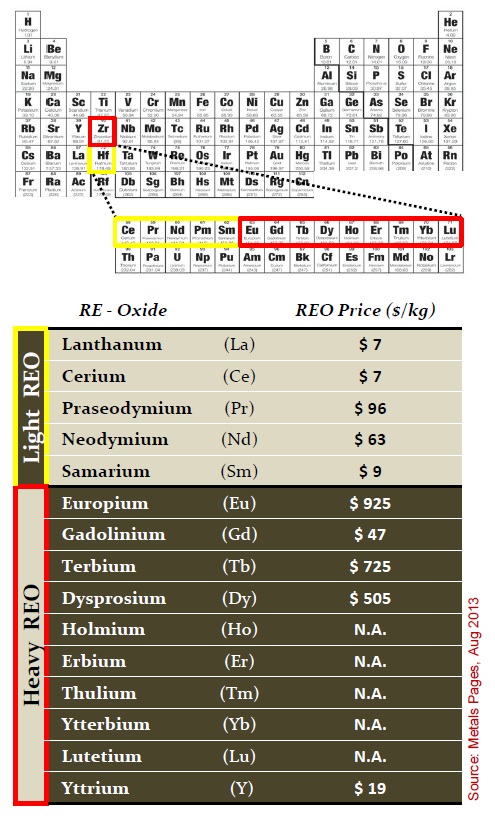

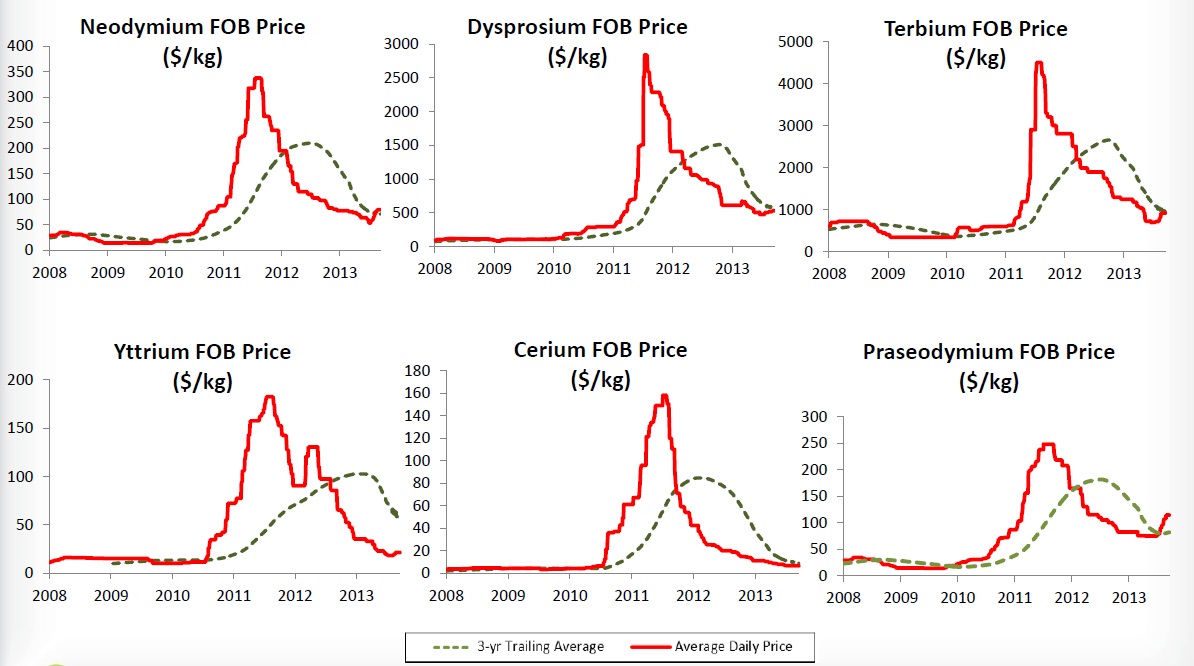

As clearly can be concluded by seeing these prices, the heavy or critical elements are far more rare than the light rare elements. A recent increase in heavy rare element prices is caused by the Chinese government's action to cut domestic rare earths' production, especially by targeting illegal miners, in conjunction with a perception of higher demand, especially in key markets such as Japan.

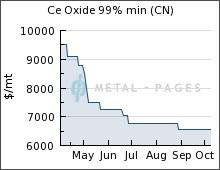

Typical development in HREE prices looks like this:

Dysprosium:

Yttrium:

In LREEs the prices don't pick up as there is more than enough supply:

Lanthanum:

Cerium:

This marks the first time prices are increasing since the spike in 2011:

(click to enlarge)

After the Chinese export limitations in 2009 caused an escalation in REE prices never seen before as is seen in the last charts, which lasted into 2011, global concern rose since then about the sustaining availability of certain REEs, important to the Western Hemisphere. Two of these critical metals are Dysprosium and Terbium, both heavy REEs.

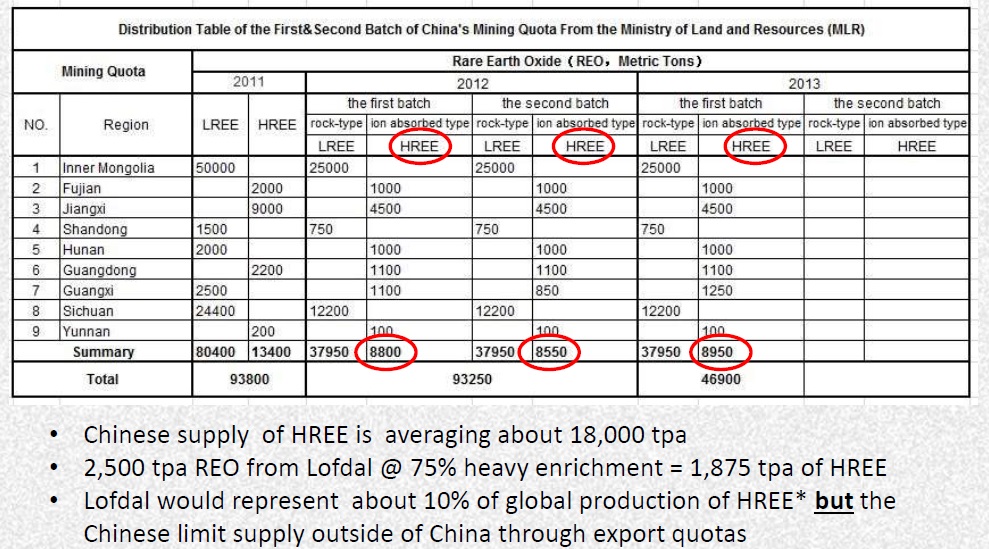

To get an idea of current production figures of China, have a look at this table:

(click to enlarge)

China produced 37,950 tonnes of LREE in H1 2013 and 8,950 tonnes of HREE in the same period. Only 3,874 tonnes of HREE were allowed for export to the rest of the world (ROW) in 2012. As China has an abundant resource base of LREEs but a relatively limited resource base of HREEs (it has only one very high percentage HREE mine, the Jangxi mine at 95% HREE), it is expected HREE output could be approaching its production limits, and China could become a net importer (here and here) from 2016 onwards.

There are doubts whether this is true, but I thought it was rather surprising to find out that the latest funding of Northland Minerals, one of the resulting top companies in my research, is financed for a considerable part by a Chinese conglomerate named Conglin. The chairman of this conglomerate, Conglin Yue, is also director and largest shareholder (37.15%) of Northern Minerals. The conglomerate is directly linked to one of the biggest state owned miners of rare earths. Another researched company, Greenland Resources, also received a lot of Chinese interest on its REE project lately. China wouldn't be doing this if internal supply wasn't any problem at all in my opinion. If they would be doing this just to maintain a stranglehold over the REE industry, they have to buy out all HREE projects globally.

I don't see this happening with several much larger and profitable North American and European initiatives whose governments would certainly block this as considerable irritation about the Chinese way of handling their REE industry and exports already developed. Over a year ago, China started stockpiling strategic reserves of REEs, this could very well be strategic for internal use, but also to halt a further drop in prices, one never knows what this country is up to. Very recently, China released other purchase plans in connection to this. Bottom line is, LREE prices are stabilized now, and HREE prices have seen a slight increase since July 2013.

A lot of countries aren't too pleased with the whole situation, for example the Defense Department of the USA is already considering starting to stockpile some critical metals, including a number of HREEs. Domestic production in the Western Hemisphere is also encouraged and followed with a lot of interest, on all levels. There are only a few companies who have very good and profitable projects at the moment, and because China could become a net importer of HREEs in a few years from now, and HREE demand in the rest of the world will be relatively limited it will be a race against time to become part of a select group of new HREE producers. One of the companies who could very well win this race for first commercial production is Tasman Metals.

4. Company

Tasman Metals is a Canadian based and Scandinavian focused mineral exploration company with extensive claim holdings in Sweden, Finland and Norway that are prospective for strategic metals, including rare earth elements and iron ore. The region is rightly regarded as the "home of REE" as many REEs were first discovered in Sweden, including cerium, erbium, holmium, lanthanum, scandium, terbium, thulium, ytterbium, and yttrium.

The Scandinavian region has a long and prosperous mining history, which has developed into a modern, highly mechanized and low cost region to explore and develop mines. The Fraser Institute in its 2012/2013 survey ranked Finland and Sweden 1st and 2nd respectively for mining friendly countries/places to explore and mine. The Scandinavian countries offer good infrastructure, a skilled workforce, modern mining legislation with low or no royalties and big areas of relatively unexplored ground.

(click to enlarge)

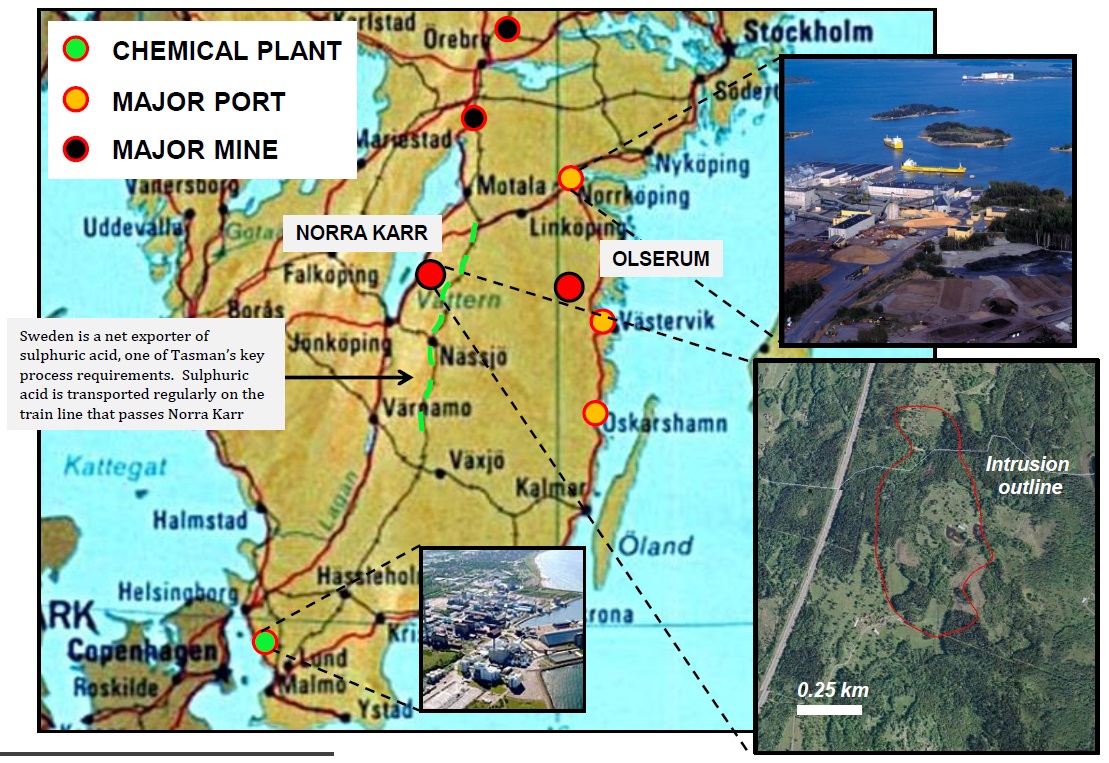

Tasman Metals, Norra Karr project, Olserum project

The management is very experienced, with senior management having 17-50 years experience in mining and/or financing. They also have an authority in the field of REEs on their advisory board, Dr. Eriksen who advises Tasman Metals on various REE processing- and separation opportunities.

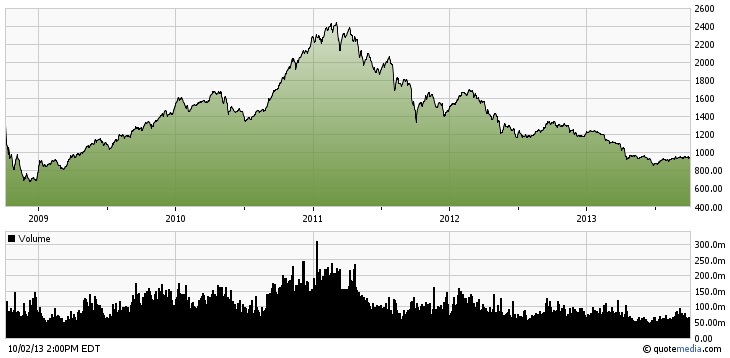

As of October 11, 2013, Tasman Metals has a share price of $0.72 and a market cap of $43.81M, with 60.85M shares outstanding. The company has $6.5M in cash and is debt free.

(click to enlarge)

Share price over 3-year period

5. Projects

A. The Norra Karr project

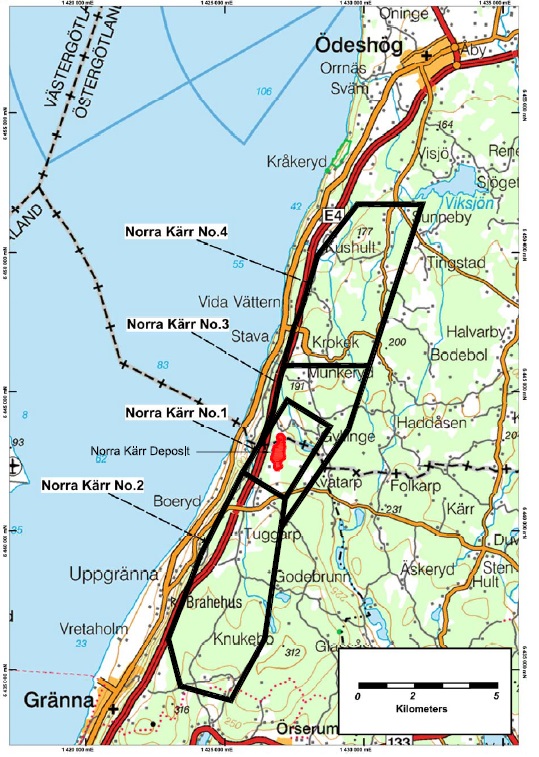

The Norra Karr project is located in southern Sweden, 300 kilometers south west of the capital Stockholm and lies in mixed farming and forestry land. The site is well serviced by power, roads and water allowing all year round access, minimizing the need for offsite infrastructure to be built by the Company. The claim area is much bigger than the deposit itself, and is supposed to have a lot of upside potential:

Tasman Metals, Norra Karr claims

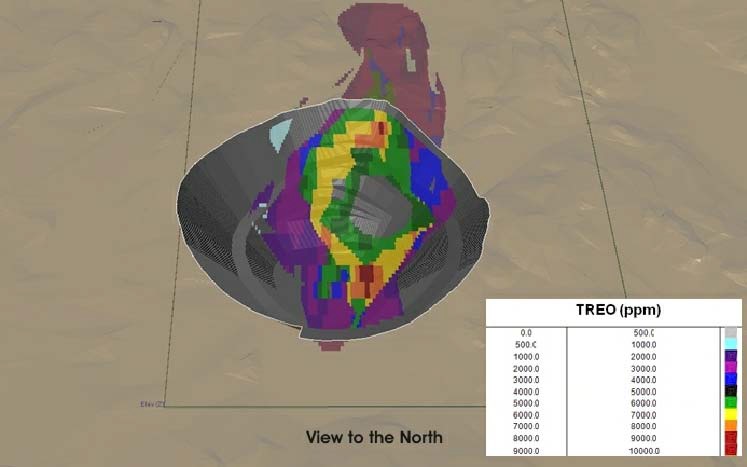

This project consists of a very near surface, rare earth deposit which is approximately 300m wide by 800m long at surface, and covered by an average of less than 1m of soil, which makes it a perfect candidate for open pit mining:

(click to enlarge)

Norra Karr, open pit visualization

Resource estimate

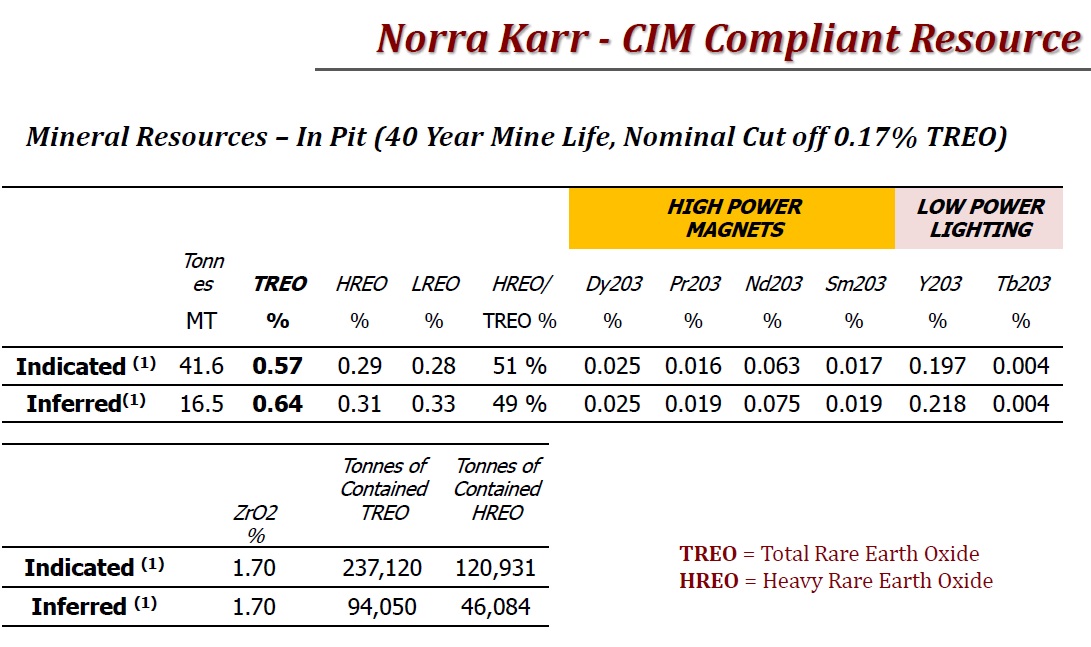

This is the resource estimate on the Norra Karr project:

(click to enlarge)

(click to enlarge)

Norra Karr project, major road within 0.5km

Tasman Metals completed a very positive Preliminary Economic Assessment (PEA) on the Norra Karr project on July 9, 2013, with key metrics a very low capex of $266M, a very high after tax IRR of 45%, a good after tax NPV of $1464M and this is all based on one of the highest percentages of HREEs globally, 51% HREEs of total rare earth oxides (TREO). The project also benefits from Zirconium oxide as by product, enhancing the business case.

B. The Olserum project

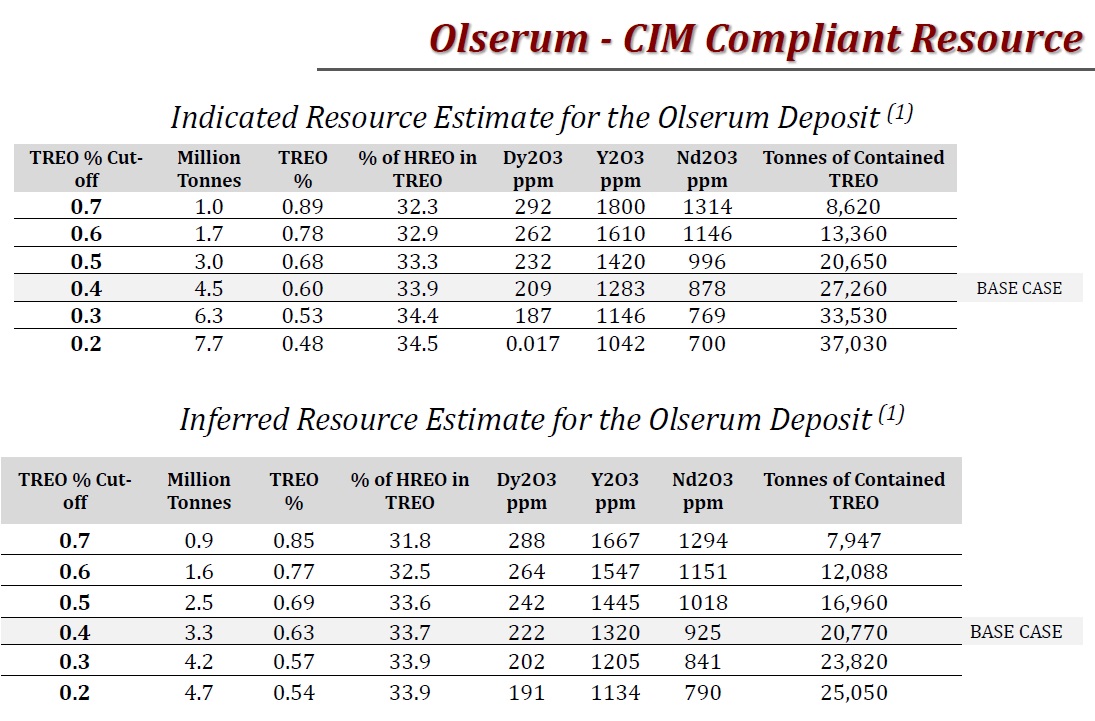

This is the other rare earth deposit of the company, although it is lower grade in HREE and has a smaller resource, it is still one of the better HREE resources in the world with 33.9% HREEs and 48,030 tonnes TREO and could easily be developed because of its small size.

Resource estimate

On June 12, 2012, Tasman Metals released an updated resource estimate for the Olserum project:

(click to enlarge)

C. Other projects

Tasman Metals also has a number of prospective iron ore claims in Sweden and Norway, and only very recently acquired 6 interesting tungsten projects which are secured by 7 exploration claims totaling 3,680.4 hectares in size. All projects, including a former tungsten producing mine, have extensive historic information including drilling, production and metallurgical data, and are supported by excellent road, rail and power infrastructure.

Tungsten is an essential industrial metal that faces the same resource security challenges to REEs, with a Chinese supply monopoly of 80%, and strongly growing demand.

Based on its economic importance and high risk of supply disruption, tungsten has been named a "critical" metal in recent British Geological Survey (BGS) and European Commission (EC) publications. Tungsten is an essential industrial element with hundreds of end-use applications. It has the highest melting point (3,410°C) and highest tensile strength of all pure metals, and is therefore highly sought after for drilling and cutting equipment, specialty steels and aerospace applications.

Since 2008, Chinese domestic demand has exceeded its own supply, resulting in a near doubling of price for tungsten concentrate over this period, and a gradual increase in total traded volume. Tungsten demand growth has consistently outperformed GDP growth, so Tasman Metals did a very interesting acquisition in my opinion with these projects, which contain on average 0.3% tungsten mineral (WO3) which is just above average. But for now all focus is directed towards the Norra Karr project.

6. Peer Comparison

Since I became curious what would be the best REE junior, I decided to perform an extensive peer comparison. As the company is a junior explorer, producers like Lynas (LYSCF.PK) and Molycorp (MCP) were left out. These two companies are currently ramping up production (or starting up production, determined by whoever is asked as much is unclear yet) of predominantly LREEs, therefore I expect them to reach full commercial production before the end of 2015. This practically rules out all other initiatives predominantly based on LREEs, as Lynas and Molycorp will produce enough to fulfill most demand on LREEs at this time for the rest of the world (ROW).

Molycorp, Phoenix project

Therefore, the only initiatives economically viable are projects predominantly based on HREEs, and the companies I chose are exploring exactly this kind of projects. However, I decided to include one exception, and this is Rare Element Resources . This company has by far the best business case